Macro Check, Aug 12-16 2024

The major earnings season is largely done. Summary:

- Strong demand for AI accelerators (hardware) and cloud (big-tech's aggressive investment commentary; visible in $TSM's results).

- In-house AI software, by contrast, is mostly still early-investment stage ($PLTR / $NOW excepted).

For big tech this season showed "rising customer gen-AI demand → higher productivity," but left the question of whether that demand converts to real net income — revenue grows yet CAPEX outflow is still heavy and "aggressive investment" was guided. Each company's Fundamental frame is roughly set post-earnings. This note looks at the macro risk the market is wary of, rather than Fundamentals / Valuation.

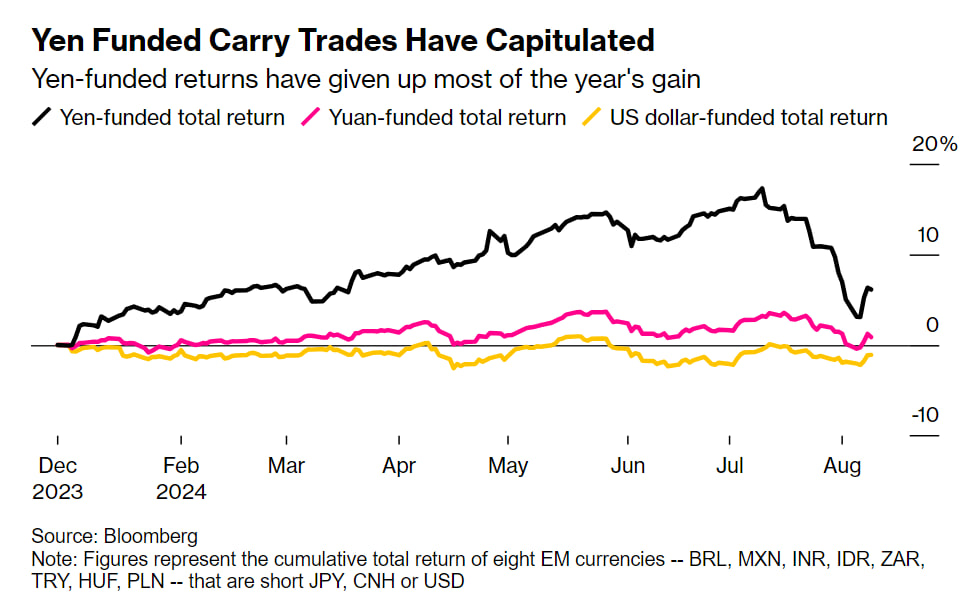

1. The Yen-Carry Unwind

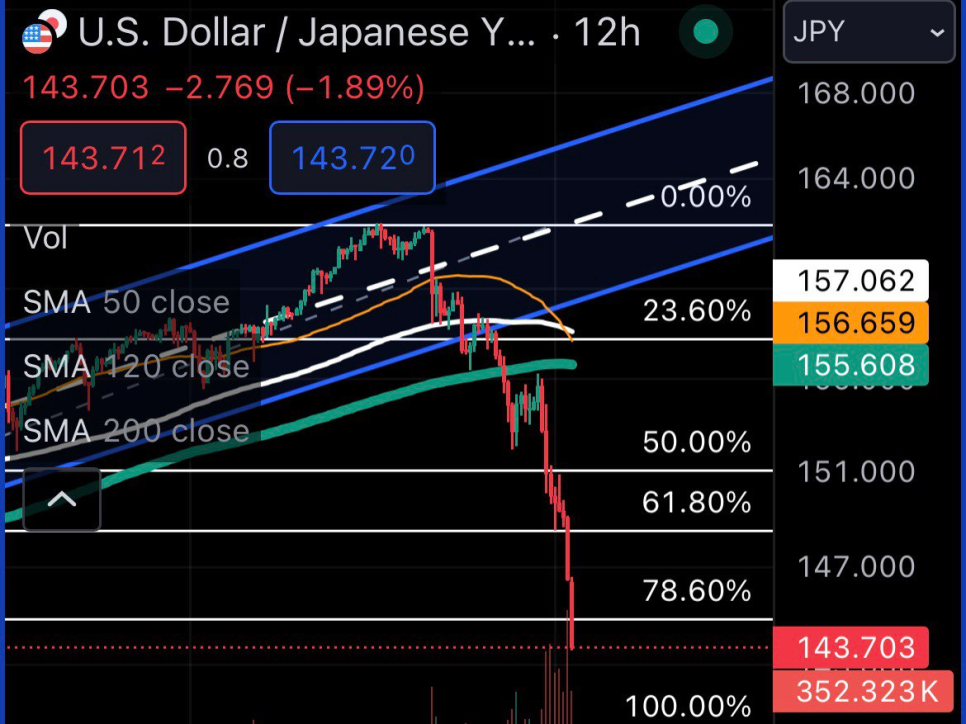

After the BOJ hiked from 0–0.1% to 0.25% on July 31, USDJPY — already falling from the mid-July high of ¥160/$ — fell further. From ¥160 → ¥150 (−6%) to ¥140 post-hike (−12%).

As the rate hit a threshold, it triggered a large unwind of the yen-carry trade — one of the funding sources driving US-equity liquidity. Yen carry: borrow low-rate yen, sell (short) it, buy (long) dollars, and invest in higher-yielding US Treasuries / corporates or high-expected-return US equities for the spread.

(For UST purchases) two profitability drivers:

- The gap between borrow rate (yen) and Treasury yield — lower borrow / higher Treasury → higher expected return. US 10Y ranges 4–5%; with Japan at −0.1% then, theoretical expected return 4.1–5.1%. After two hikes (Japan 0.25%) and US 10Y falling to 3.9–4.2% over the window, theoretical expected return dropped sharply to 3.65–3.95%.

- FX risk after converting yen→USD — USDJPY +1% → expected return +1%, −1% → −1%.

Net: lower yen rate / higher dollar rate motivates the carry more; while holding the dollar position, a rising USDJPY further raises expected return, a falling one lowers it. If USDJPY keeps falling (yen appreciates) entrants liquidate yen-based positions to avoid losses. That risk detonated decisively from the Aug 5 Asia session through the US session.

2. Three Institutions and the FX Band

If USDJPY exceeds ¥160/$, yen depreciation causes a domestic-demand recession in Japan, so the BOJ tried to defend ¥160. It succeeded, and the rate entered the stable ¥150–160 band. After the July 31 hike to 0.25% it fell to ¥140. After the carry-unwind-driven global crash, the BOJ said "further hikes look difficult" — the downside possibility faded (one risk off).

The institutions most directly tied to USDJPY, at the largest scale, are the BOJ, the US Treasury, and US hedge funds. The band all three agree on is ¥150–160 (minimizing each's losses, maximizing gains):

- BOJ: the last threshold to minimize a domestic-demand recession. Most cash is locked in USTs, and the only FX-defense option is sell USTs → sell USD → buy JPY (the hike card is spent).

- US Treasury: Japan is a major foreign UST holder; a large Japanese UST sale would ripple through the bond market. Yellen must protect equity / bond markets and stimulate growth into the election — maintaining this band shields the bond market from BOJ selling.

Top-5 foreign holders of US Treasuries

- US hedge funds: a band suitable for maintaining carry positions. Funds run via borrow JPY → sell JPY → buy USD → invest in US equities / Treasuries need this band held to minimize FX risk and earn stable returns.

USDJPY is now finding support at ¥140 and bouncing. On the hypothesis it soon returns to ¥150–160:

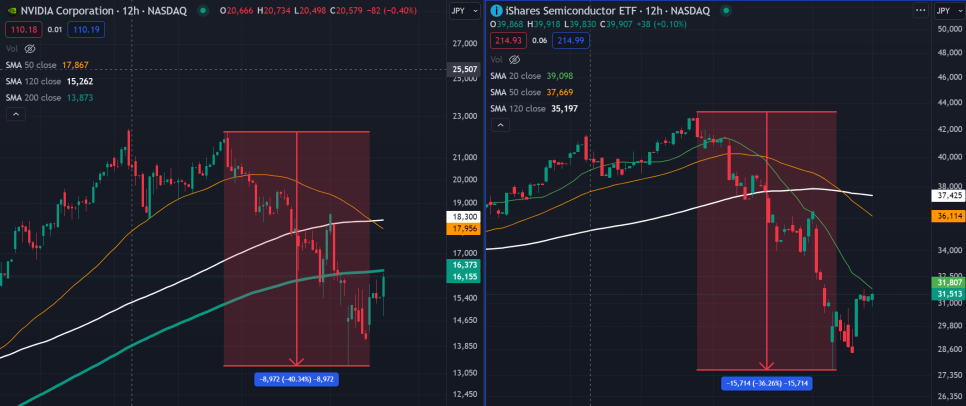

USDJPY downside risk has eased somewhat. Current major indices / stocks / US bonds are cheap on a yen basis — the Black-Monday drop plus FX drop means a substantial fall from the prior high.

In yen terms: S&P 500 ~−18% from the prior high, Nasdaq 100 ~−24%

The H1-2024 rally leaders NVIDIA and SOXX ETF, in yen terms, ~−40% / −36% from the high

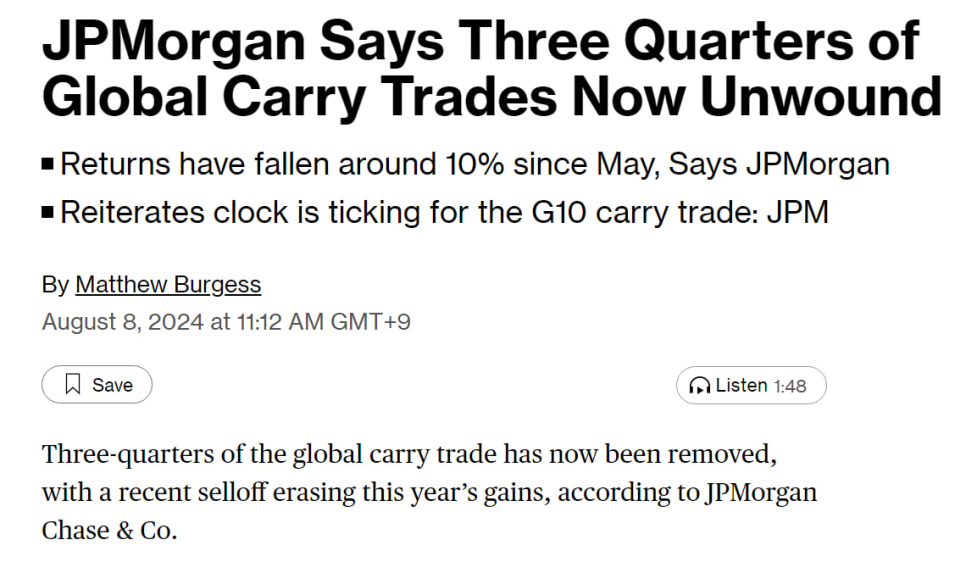

Per JPMorgan, ~3/4 of global carry-trade funds were unwound — this fear zone could instead be a good entry zone for hedge funds. At least short-term, funds rotate from yen into US equities / bonds, and continued yen selling returns USDJPY to ¥150–160. Thereafter USDJPY moves as a dependent variable of major indices like the S&P 500 — at the threshold USDJPY led the market; now the S&P 500 / Nasdaq 100 retake the lead.

3. Filtering the Residual Risks

(1) Yen carry / the Fed

USDJPY downside is less likely, but it is hiked to 0.25% regardless. The larger the September Fed cut, the lower yen-carry expected return — a big Fed dilemma → doubt that the prior yen-carry demand holds.

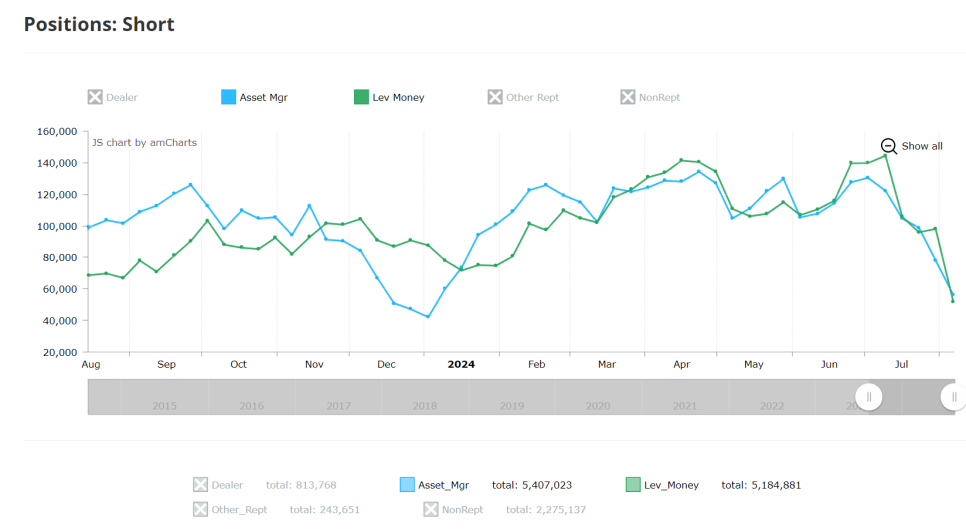

Per the CME yen-futures COT (Commitments of Traders) report, from mid-July to Aug 6 (latest) the yen-short positions of asset managers (Asset_Mgr) and hedge funds (Lev_Money) shrank sharply. Watch the Aug 16 yen-short data — a rebound signals funds rotating from yen back into US equities / bonds.

(2) Data / CPI

US data is stable so far, but Wednesday's July CPI may print softer than expected (consumer data is negative).

Current sentiment is "bad is bad" — a large CPI miss could act as short-term noise.

(3) Election uncertainty

Ultimately, who becomes president could reshape the market and economy. The market hates uncertainty most.

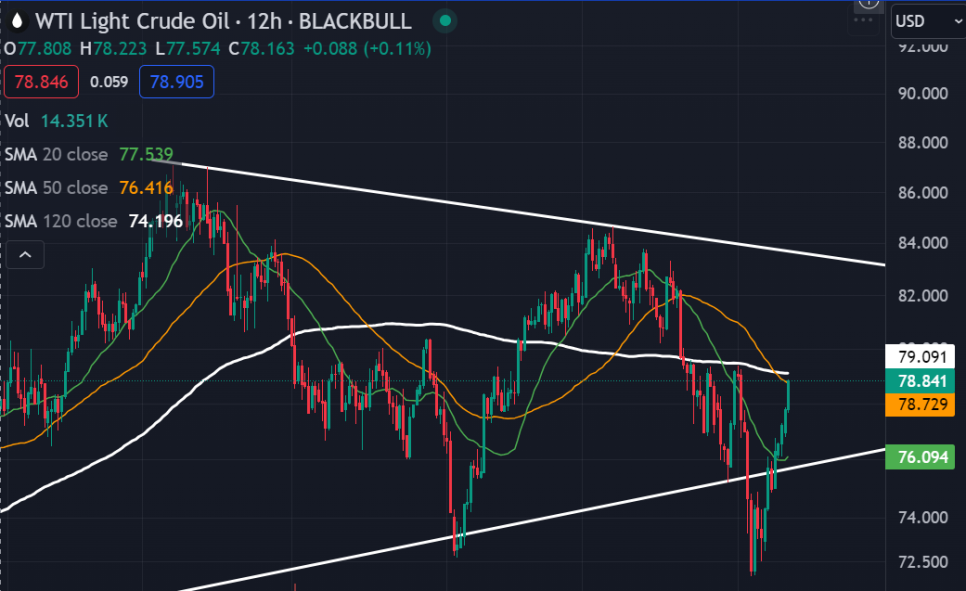

(4) Geopolitics — oil

A possible Middle East war is raised and affecting oil:

Higher oil means higher odds of inflation reignition. (The Russia–Ukraine war is also a residual risk.)