On the Bessent-Warsh Regime Pt. 1 | Introduction and Inflation Prerequisite

At the start of 2026, the US fiscal financing architecture has hardened into a single coherent regime rather than a sequence of discrete policy decisions — three institutional choices have moved into lock-step.

- Treasury's bill-share metric switch, the Fed's RMP autopilot, and the Bessent–Warsh political layer all operate as one coherent system.

- This series covers (a) how the regime was institutionalized and (b) what could go wrong. Part 1 lays out the regime itself and the inflation prerequisite its operation hinges on.

Conclusion

- The core of the Bessent–Warsh regime is a framework in which "issuance mix is the primary lever on long-end yields, with the Fed policy rate as the secondary lever."

- Treasury justifies a path of raising bill issuance and cutting coupon issuance under the new metric, and

- the Fed absorbs that bill supply through RMP as a standing operation, so that net bill supply to the market converges to near zero.

- The regime is self-reinforcing — but only as long as inflation does not reignite. If the Fed is forced to prioritize its mandate over the absorption role, the RMP rationale weakens and the entire regime comes under stress.

- Assessing the inflation path requires looking at the spread across three measures simultaneously — core CPI, core PCE, and ex-tariff core PCE — not any single number. Where you place your prior across the roughly 100 bp spread is what splits the hawk and dove camps' framing.

- The regime's prerequisite is not "the ex-tariff reading is correct" but rather "Fed staff are actually using the ex-tariff reading in their internal assessment, and the market is pricing that fact in." The spread narrows toward disinflation — and the prerequisite holds — only when two conditions are met simultaneously: no Tariff Round 2, and no activation of oil-lag channel 4 (the channel through which sustained oil price increases manifest as household concerns about inflation persistence over the next 6–12 months).

Core Summary

1) What it means that the regime has been institutionalized

Three policy signals don't sit independently — they interlock as one coherent regime.

- Treasury switched its operative bill-share metric from "bills / total outstanding" to "bills / privately-held outstanding."

- The denominator nets out the Fed's SOMA holdings.

- For the same issuance plan, measuring under the new metric makes bill share appear to stay within the target band.

- On that metric-based justification, Treasury chose a 2026 path of raising bill issuance by +$461B and cutting coupon issuance by −$461B.

- The Fed restored Reserve Management Purchases (RMP) as a standing operation via the December 10, 2025 FOMC directive.

- RMP absorbs ~$360B/year, MBS paydown reinvestment absorbs ~$180B/year — together, about $540B/year of bills end up in SOMA.

- This framework operates separately from the FOMC's policy rate decisions, framed as a plumbing operation to "maintain ample reserves."

- Treasury Secretary Scott Bessent said in a February 2025 interview, "We're focused on the 10-year, not the Fed funds rate," framing issuance mix as the primary lever on long-end yields. The political layer was then completed on April 29, 2026, when the Senate Banking Committee advanced Kevin Warsh's Fed Chair nomination on a 13–11 party-line vote — a full Senate vote is imminent ahead of Powell's chair term expiring May 15.

When these three layers operate together, Treasury's bill issuance is netted out by the Fed's absorption, the bill supply reaching the market is essentially zero, and the reduction in coupon supply eases upward pressure on the 10Y / 20Y / 30Y. Treasury's interest cost stays controlled, and the bill-heavy tilt sustains itself. It is self-reinforcing — as long as inflation does not reignite.

2) The regime's single point of failure

Inflation.

- If the Fed is forced to prioritize its mandate (price stability) over absorption (bill absorption through RMP),

- the "ample reserves" framing around RMP weakens and the bill-absorption autopilot stops.

- At that point Treasury's issuance-mix lever stops working mid-air, term premium reprices, and upward pressure builds on long-end yields.

1. The Regime Plan ⎯ What Got Institutionalized

(1) Treasury's bill-share metric switch ⎯ reframing onto a private-basis

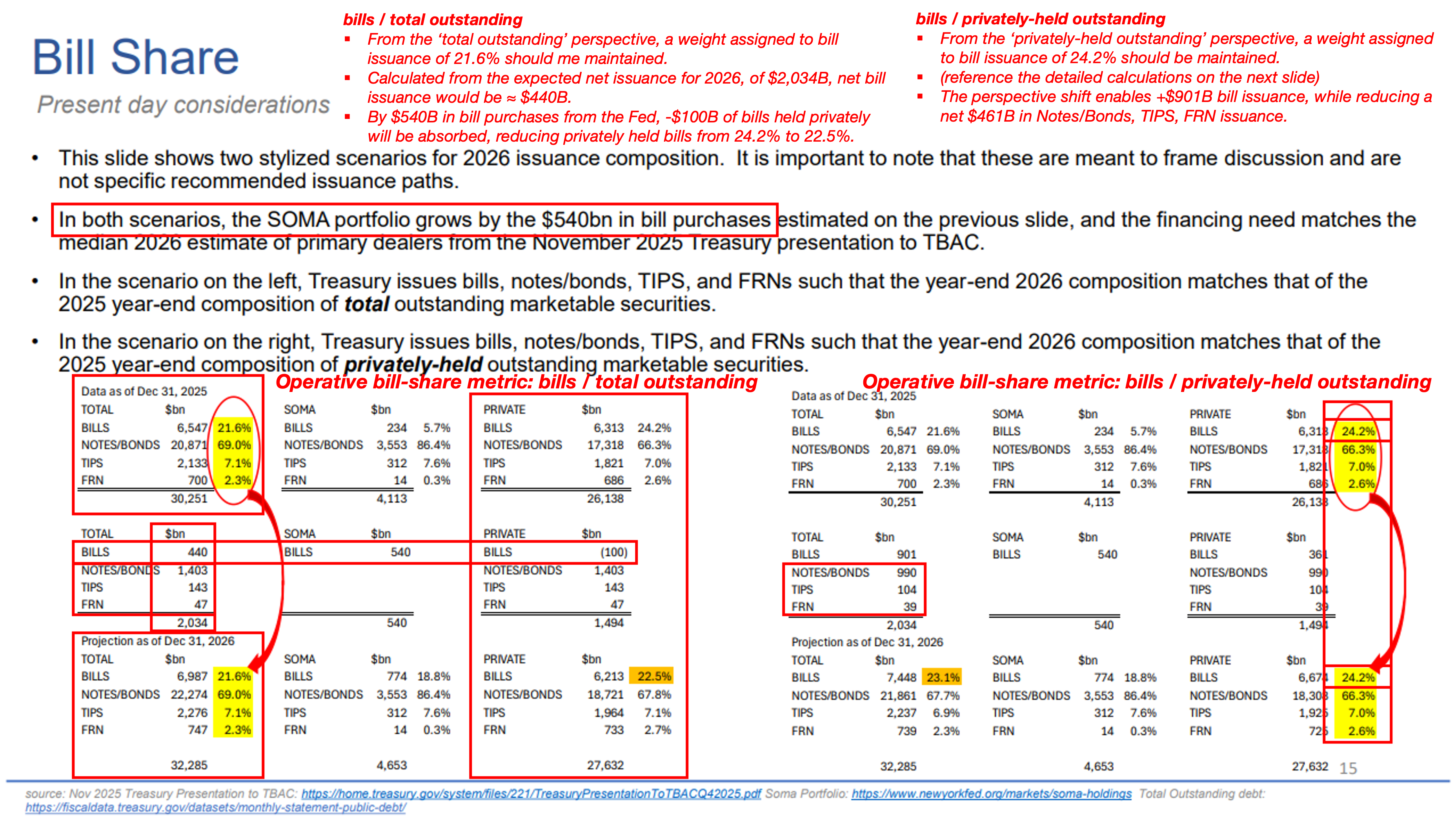

In the February 2026 Quarterly Refunding Statement (QRA) and the accompanying TBAC materials, Treasury's operative bill-share metric switched from "bills / total outstanding" to "bills / privately-held outstanding."

Privately-held = total marketable debt − Fed SOMA holdings.

1) The difference between the two metrics

| Metric | Denominator | Policy implication |

|---|---|---|

| Bills / Total outstanding | All marketable Treasury debt | Includes bills absorbed into SOMA. The "headline" ratio. |

| Bills / Privately-held outstanding | Private holdings, excluding Fed SOMA | The bill share the market actually has to absorb. The reference for Treasury issuance mix. |

When Treasury issues debt and the Fed's SOMA buys it, that issuance never reaches private investors. Viewed as one consolidated federal entity, debt issued by Treasury and held by another arm of the same government (the Fed) is effectively an internal transaction. What matters for the market, on this logic, is the composition of debt actually held by private investors — not the gross issuance figure.

Holding the same "low-20%" bill-share target, measuring on a private basis lets Treasury raise nominal bill issuance more aggressively. The path of cutting coupon (notes / bonds / TIPS / FRN) issuance and adding to bill issuance is justified under the new metric.

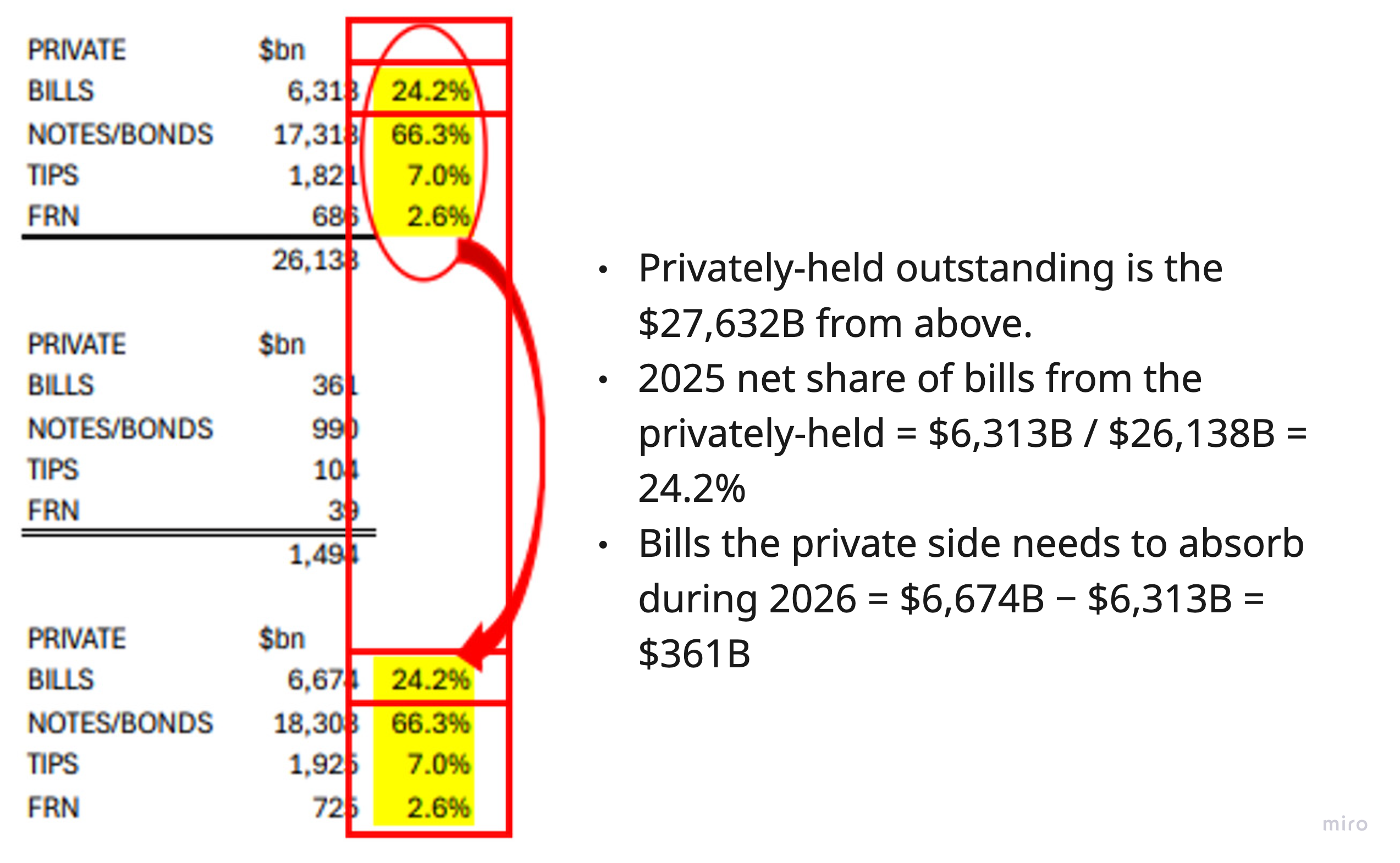

2) Calculation ⎯ 2026 projection (based on TBAC presentation, February 2026)

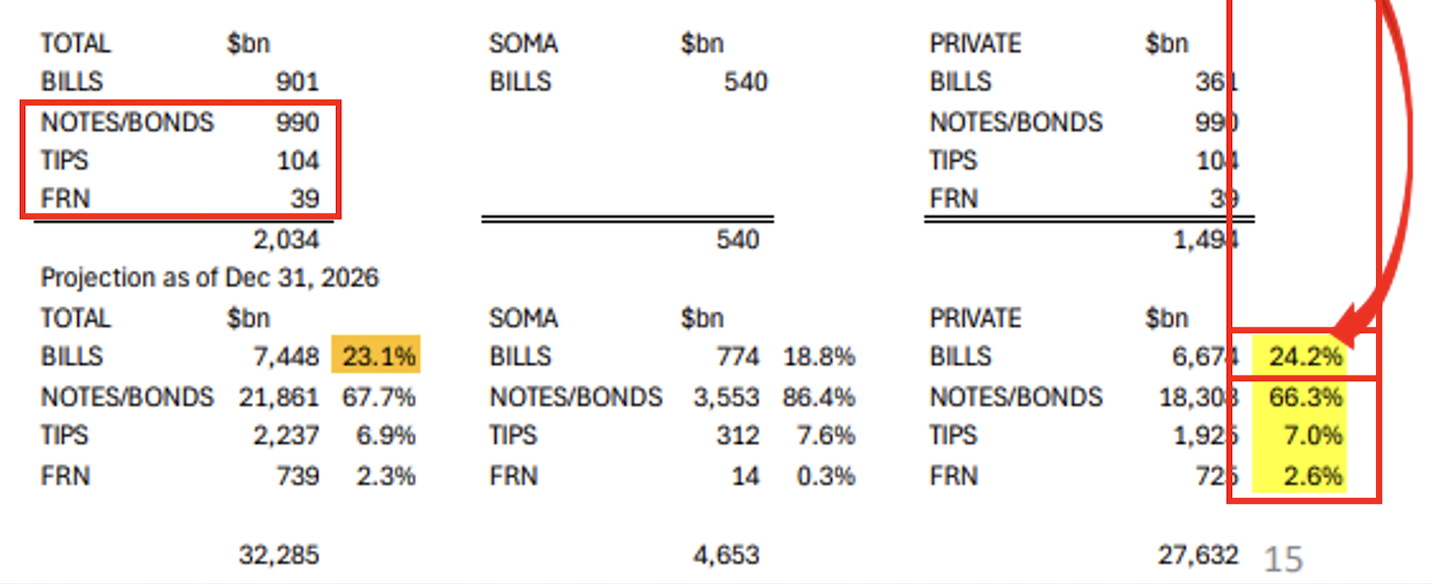

Under the bills / total outstanding metric (old)

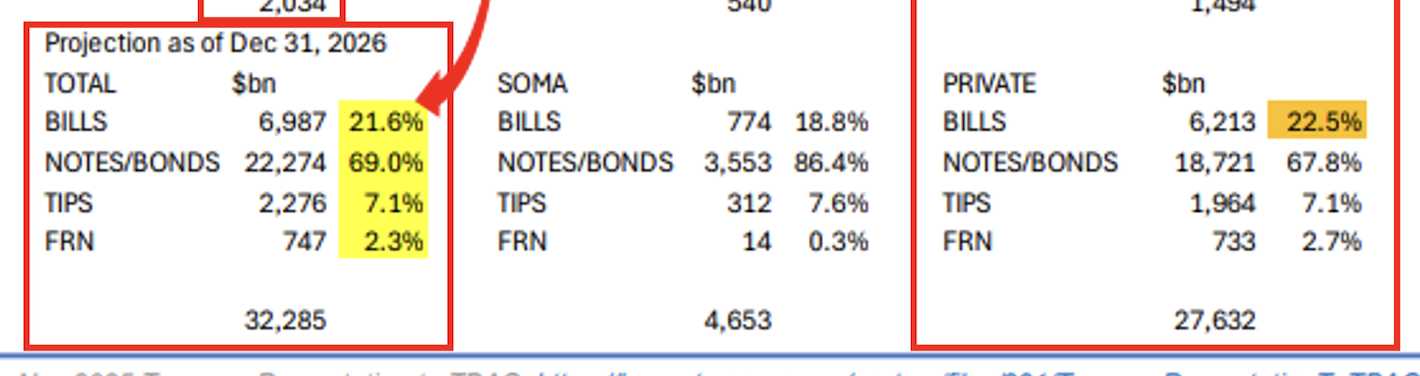

- Total marketable Treasury debt outstanding (Dec 31, 2025) = $32,285B

- The Fed's SOMA absorbs $540B in 2026, putting end-of-year SOMA balance at $4,653B

- The difference is privately-held outstanding = $32,285B − $4,653B = $27,632B

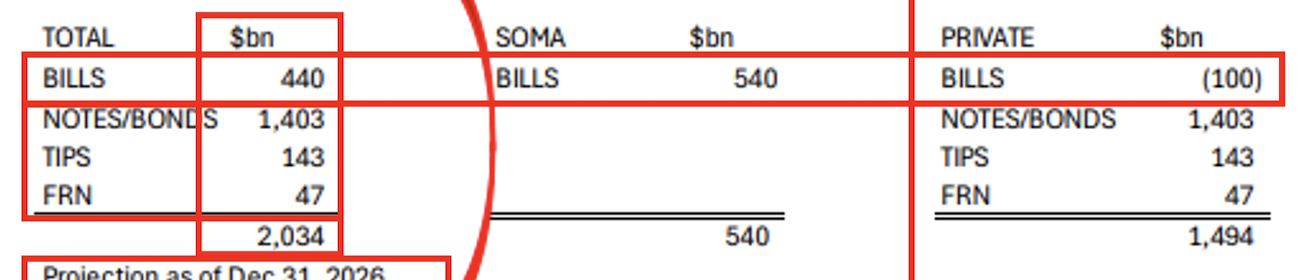

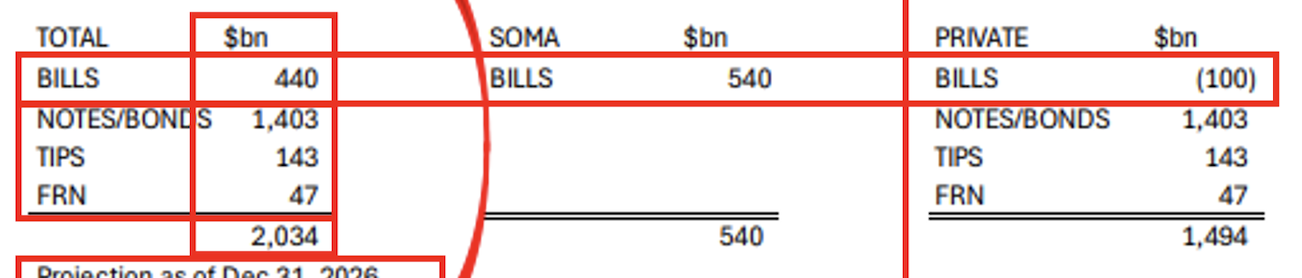

- $440B in bills get issued in total.

- After subtracting $540B that Fed SOMA absorbs, the privately-held basis sees −$100B in bills — bill liquidity available to the private market actually shrinks.

Under the bills / privately-held outstanding metric (new)

TOTAL, SOMA, PRIVATE securities distribution under the bills / privately-held outstanding metric

TOTAL, SOMA, PRIVATE securities distribution under the bills / total outstanding metric

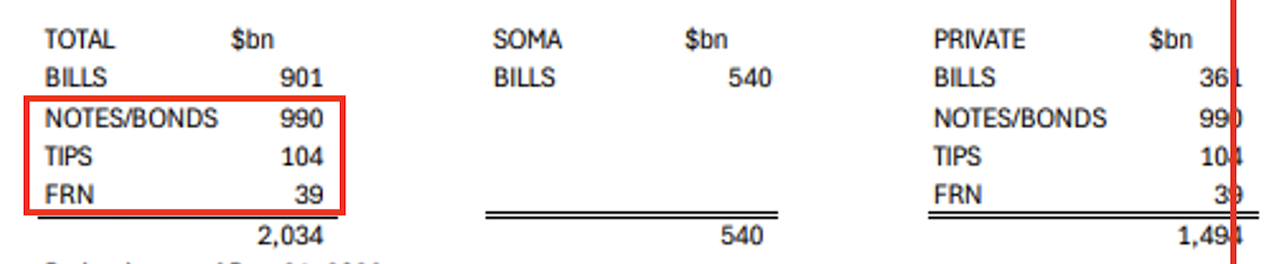

- Total bills issued = $361B + $540B = $901B

- Total securities issuance stays at $2,034B, so the +$461B in bill issuance is offset by an equal-sized reduction across notes / bonds, TIPS, and FRN.

| Category | Pre-shift (2026 plan) | Post-shift (2026 plan) | Difference |

|---|---|---|---|

| Bills | $440B | $901B | +$461B |

| Notes/Bonds | $1,403B | $990B | −$413B |

| TIPS | $143B | $104B | −$39B |

| FRN | $47B | $39B | −$8B |

| Total coupon difference | ≈−$461B (≈+$461B substituted into bills) |

- Bills held by the private side at year-end 2026 = $27,632B × 0.242 = $6,674B

- Bills held by Fed SOMA at year-end 2026 = $234B + $540B = $774B

- Total bills outstanding at year-end 2026 = $6,674B + $774B = $7,448B

- 2026 net share of bills = $7,448B / $32,285B = 23.1%

- Under the total-outstanding metric, the bill share rises 21.6% → 23.1%; under the privately-held metric, it stays at 24.2%.

3) Two narratives, depending on which metric you pick

| View | Implication |

|---|---|

| Total-outstanding view (old metric) | Bill share looks like it's rising 21.6% → 23.1% YoY. Triggers "bill-heavy" concern. |

| Private-holdings view (new metric) | Bill share stays at 24.2%. Treasury can argue it remains "within the target band." |

The same issuance plan produces different narratives depending on the metric you choose. From Treasury's standpoint, this lets the constraint on long-end issuance be reframed not as "politically motivated issuance gerrymandering" but as "sound debt management measured on a private-holdings basis."

(2) The Fed's bill-absorption autopilot ⎯ RMP + MBS reinvestment

- At the October 2025 FOMC, the Fed confirmed it would end QT as of December 1. The signs of liquidity stress that had emerged across MMFs were the core backdrop.

- At the December 10, 2025 FOMC, the Fed formalized the resumption of Reserve Management Purchases (RMPs) to manage reserve levels, directing the NY Fed Open Market Trading Desk to grow SOMA holdings.

- Alongside RMP, MBS paydowns are reinvested into bills. Combined, the Fed absorbs around $540B in bills per year.

4) The definition of RMP

- Reserve Management Purchase is the operation through which the Fed buys Treasury bills in the secondary market to maintain ample reserves.

- It is framed as operating policy and executed separately from the FOMC's policy rate decisions — a plumbing operation that maintains ample reserves regardless of the policy stance.

- First implementation: December 12, 2025 (initial schedule of $40B in T-bills).

5) MBS paydown reinvestment

- Previously, MBS paydowns within SOMA were automatically rolled off up to a runoff cap.

- From Q4 2025, the Fed shifted those paydown proceeds into bill reinvestment.

- The pace is ~$13–16B per month, or roughly $180B annualized.

6) Combined absorption

| Operation | Monthly | Annualized |

|---|---|---|

| Reserve Management Purchases (bills) | ~$30–40B (variable) | ~$360B/yr |

| MBS paydown → bill reinvestment | ~$13–16B | ~$180B/yr |

| Total | ~$540B/yr |

That $540B is the SOMA-absorption assumption baked into the TBAC private-basis framework.

7) RMP's two funding sources and the inflation sensitivity of its framing

- The $540B in annual SOMA absorption looks like one mechanism, but the monetary implications of its two components diverge.

- RMP (~$360B/yr) is an operation in which the Fed buys bills in the secondary market with newly created reserves — a net expansion of the Fed's balance sheet, effectively quasi-QE.

- MBS paydown reinvestment (~$180B/yr) is a portfolio rotation: proceeds from MBS paydowns within existing SOMA holdings get rolled into bills. The total balance sheet doesn't change; only the asset mix shifts from MBS to bills.

- So out of the $540B, roughly two-thirds is net new balance-sheet expansion and roughly one-third is portfolio rotation.

- This distinction is why the "ample reserves" framing around RMP is sensitive to the inflation environment (which gets worked out concretely below).

- Rotation has essentially no impact on the monetary stance, but

- new reserve creation is, in substance, balance-sheet expansion — and that becomes directly contested under an inflation-fighting credibility lens.

- In a low-inflation environment, markets and the political establishment accept RMP as plumbing.

- Once inflation starts to reignite, every Fed action gets re-evaluated against a single criterion: "Is the Fed demonstrating inflation-fighting commitment?" Under that lens, balance-sheet expansion is hard to defend.

- And because the quantitative threshold for "ample" isn't fixed, the argument "reserves are already ample enough — no need to buy more" becomes defensible too.

- The Fed ends up choosing between maintaining RMP (absorbing the fiscal-dominance narrative) and pulling back on RMP (defending mandate credibility) — and in an unfavorable inflation environment, the latter becomes plausible.

8) Operational schedule (December 2025 ⎯ May 2026)

| Operation period | Reinvestment | RMP | Notes |

|---|---|---|---|

| Dec 12, 2025 ⎯ Jan 14, 2026 | ~$14.4B | ~$40B | Initial schedule |

| Jan 15 ⎯ Feb 12, 2026 | ~$15.4B | ~$40B | |

| Feb 13 ⎯ Mar 12, 2026 | ~$13.4B | ~$40B | |

| Mar 13 ⎯ Apr 13, 2026 | ~$13.8B | ~$40B | |

| Apr 14 ⎯ May 13, 2026 | ~$15.5B | ~$25B | First RMP step-down ⎯ seasonal variation |

- RMP is announced monthly and its scale adjusts to seasonal fluctuations in reserve demand.

- The $25B step-down in the April–May window is empirical evidence that "RMP is a plumbing operation calibrated to maintain ample reserves" — monthly intervention size is variable, not fixed.

9) Why this counts as "autopilot"

- RMP is not an instrument that gets reviewed every FOMC cycle alongside the policy rate decision.

- The December 10, 2025 directive made it a standing operation; the monthly announcement is closer to an operational task that updates the schedule than a policy decision.

- In other words, as long as reserves-side plumbing is being maintained, the Fed keeps absorbing bills regardless of the inflation backdrop.

- That said, two escape clauses are baked into the very phrase "to maintain ample reserves":

- If reserves are judged to be no longer scarce, the rationale for RMP disappears and the operation can be paused.

- If inflation pressure starts to conflict with the Fed's mandate (price stability), the Fed can rethink RMP itself.

10) What it means for Treasury

Run alongside the TBAC private-basis framework,

- Treasury can issue additional bills on the assumption that SOMA will absorb $540B,

- which lets it cut the relatively expensive funding cost on intermediate and long-dated debt by substituting bills.

- The cascade: reduced coupon issuance → less long-end supply pressure → easing of upward pressure on 10Y / 20Y / 30Y yields.

(3) The political layer ⎯ Bessent's 10Y posture and Warsh's Chair nomination

1) Bessent's stated posture

In a February 2025 Bloomberg interview, Treasury Secretary Scott Bessent stated: "He [Trump] and I are focused on the 10-year Treasury... He is not calling for the Fed to lower rates."

The crux is the framing that the lever for pulling borrowing costs down is not the Fed funds rate but the 10Y Treasury yield. Three policy implications follow:

- Treasury attempts to directly control long-end supply through its issuance mix (bills ↑ / coupons ↓), with the TBAC private-basis framework providing the justification.

- By not pressuring the Fed for rate cuts, Bessent avoids antagonizing the inflation-hawk camp — preserving political room.

- At the same time, deficit financing cost is shifted from the long end to the short end (where the Fed absorbs it).

2) Warsh nomination timeline

| Date | Event |

|---|---|

| 2026-04-21 | Senate Banking Committee confirmation hearing |

| 2026-04-29 | Banking Committee advances nomination on a 13–11 party-line vote ⎯ the committee's first fully partisan vote on a Fed chair |

| 2026-05-04 | Warsh's remarks on Fed independence trigger "confusion + concern" in the market (CNBC reporting) |

| 2026-05-15 | Powell's chair term expires ⎯ full Senate vote likely before then |

- How it cleared the committee

- Sen. Thom Tillis (R-NC) had placed a hold on the nomination. A Senate "hold" is an informal procedural objection to the majority leader, signaling "don't bring this to the floor"; unless released, scheduling typically gets deferred.

- Once the hold was released, the Banking Committee was able to advance the nomination.

- The direct trigger was the DOJ dropping its criminal investigation into Powell — which removed the motivation behind Tillis's objection.

- Camp positions

- Democrats (Warren and others) raised concerns about Fed independence, calling Warsh a "sock puppet of Trump."

- Warsh himself emphasized institutional independence, arguing the Fed "should stay in its lane." Some market participants, though, read those very remarks as a signal of policy autonomy weakening (CNBC May 4 reporting).

- Confirmation outlook

- With a Republican Senate majority and Tillis's hold released — i.e., the procedural choke point gone and the majority party's arithmetic running through unimpeded — full Senate confirmation looks highly probable.

- By the time Warsh takes the chair, the RMP framework will already be entrenched as a standing operation.

- Forward risk under the new chair

- Whether the new chair re-interprets the RMP framing depends on the inflation path — if the "ample reserves" justification weakens or inflation reignites, RMP itself could become a political target.

3) How the two figures' axes lock in

| Layer | Bessent (Treasury) | Warsh (Fed Chair, post-confirmation) |

|---|---|---|

| Primary lever | Issuance mix (bill ↑ / coupon ↓) | RMP / SOMA balance composition |

| Stated objective | 10Y Treasury yield stability | Ample reserves + dual mandate |

| Implicit goal | Suppress coupon supply → ease upward pressure on long-end yields | Absorb bills → justify Treasury's issuance mix |

| Political cover | "We're not asking for rate cuts" | "Fed stays in its lane" ⎯ preserving the independence framing |

The two levers align not through explicit coordination but at the framework level — producing the same outcome without looking like fiscal dominance.

(4) Pulling it together

Treasury ↑bill / ↓coupon → Fed absorbs through RMP (autopilot) → Net bill supply to market is essentially zero → Short end stays stable + coupon supply contracts → Eased upward pressure on 10Y / 20Y / 30Y → Treasury interest cost stays controlled → The bill-heavy tilt sustains itself

Unless inflation reignites, this is a self-reinforcing dynamic — for the full 2026 horizon, at least.

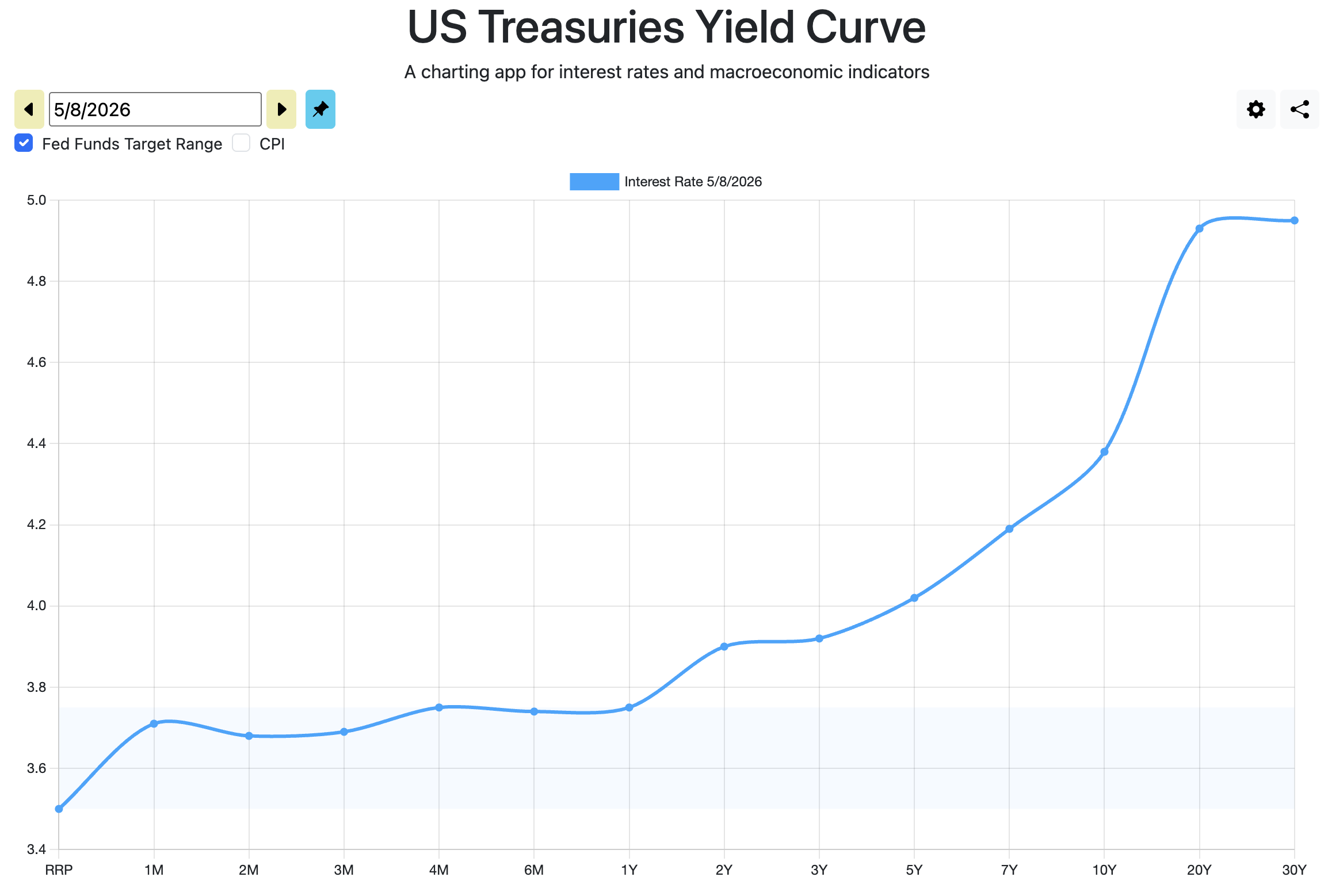

2. The Inflation Prerequisite

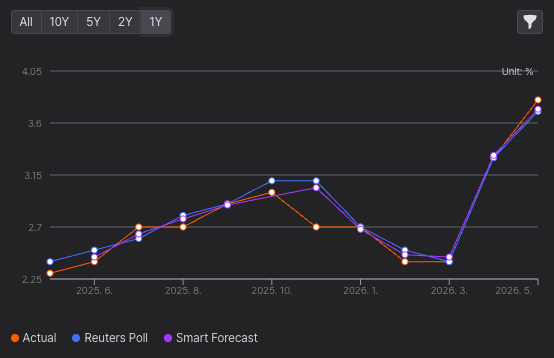

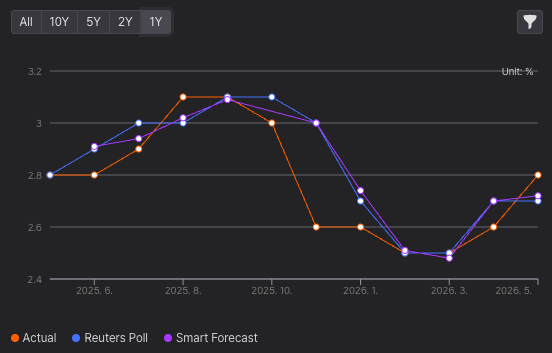

As emphasized above, the regime's single point of failure is inflation. Evaluating the Bessent–Warsh regime's operation requires looking at three measures simultaneously rather than any single number — the core CPI the market watches, the core PCE the Fed targets, and the underlying core PCE that backs out tariff effects.

(1) Three numbers (latest releases)

| Measure | Reading | Implication |

|---|---|---|

| Core CPI YoY (Apr 2026) | 2.8% | Market-facing tape ⎯ sticky but not accelerating |

| Core PCE YoY (Mar 2026) | 3.2% | The Fed's dashboard |

| Core PCE ex-tariff (Fed staff implied) | ~2.4% | The underlying signal ⎯ inside the 2% target band |

The spread across these three readings sets the framing for the entire stage. (April Core PCE is scheduled for BEA release on May 30; the table holds March as the reference point for now.)

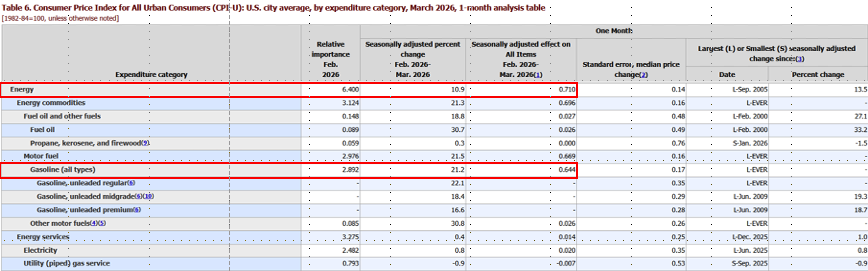

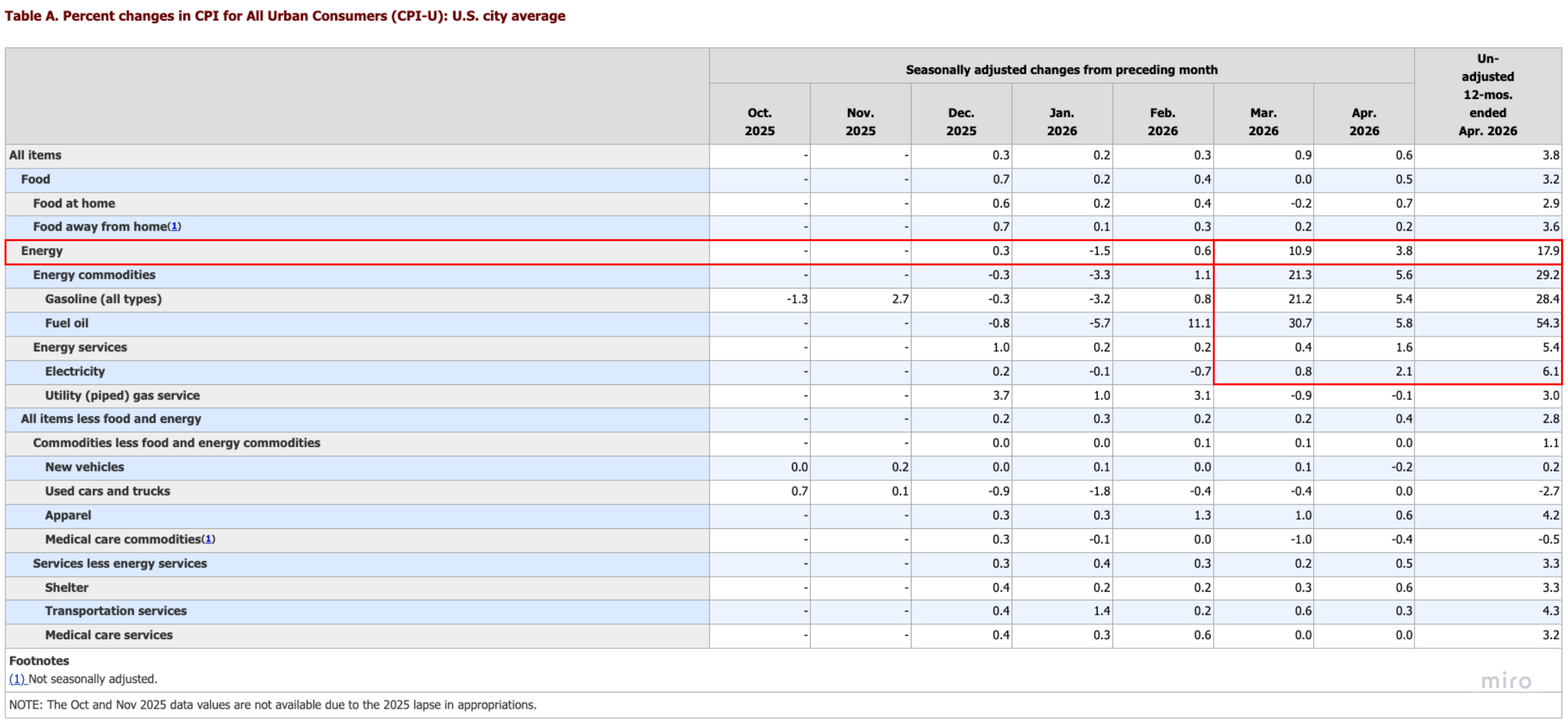

(2) March 2026 CPI

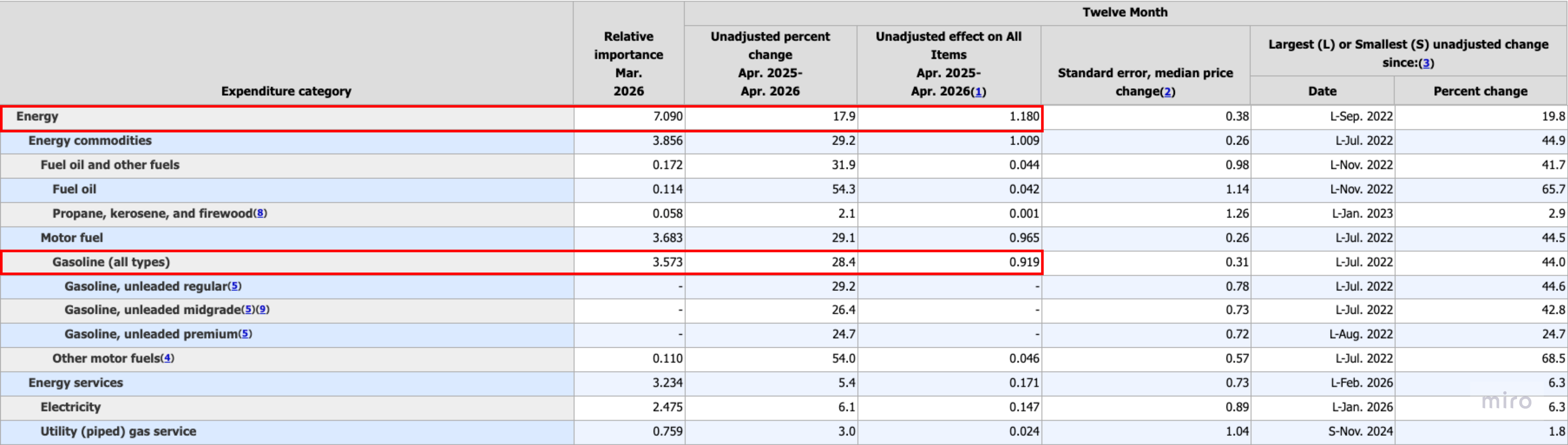

- Headline CPI: +0.9% MoM, +3.3% YoY

- Energy: +10.9% MoM, gasoline +21.2% MoM. Energy contributed +0.71pp to all-items (gasoline alone +0.64pp).

- Core CPI: +0.2% MoM, +2.6% YoY.

(3) April 2026 CPI

- Headline CPI: +0.6% MoM, +3.8% YoY.

- Energy: +3.8% MoM (decelerating from March's +10.9%), +17.9% YoY.

- Gasoline +5.4% MoM, +28.4% YoY.

- Fuel oil +5.8% MoM, +54.3% YoY.

- Core CPI: +0.4% MoM, +2.8% YoY (up modestly from March's 2.6%).

Key read:

- April energy MoM decelerated from +10.9% to +3.8%, but YoY accumulated to +17.9% — upward pressure persists at the run-rate.

- Gasoline +28.4% YoY confirms the refined-product → retail-energy passthrough is steadily showing through.

- Core CPI ticked up modestly from +2.6% to +2.8% YoY but stays within the sticky-but-stable range.

(4) March 2026 PCE

- Core PCE: 0.3% MoM, 3.2% YoY.

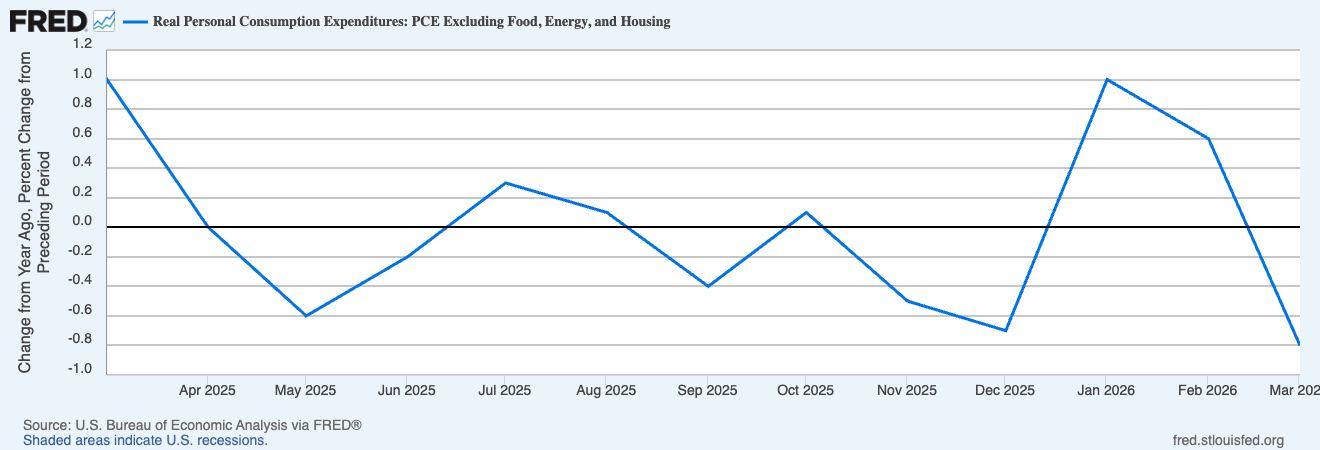

- Real PCE ex food, energy, and housing has been in a downtrend on a YoY basis through 2026.

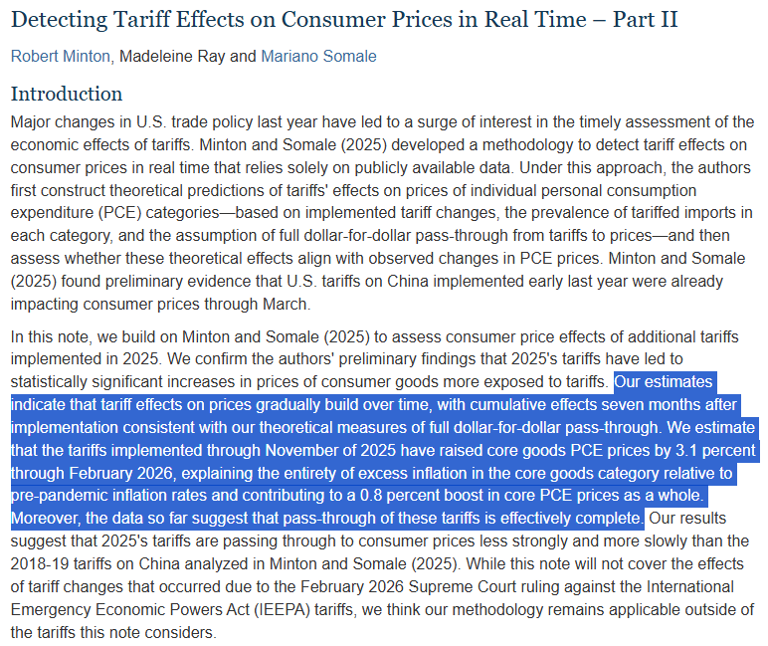

(5) The Fed's tariff study

- The reciprocal tariffs applied April 2, 2025 lifted core-goods PCE cumulatively by 3.1% through February 2026, according to the Fed staff analysis.

- The total contribution of tariffs to headline core PCE comes to 0.8pp.

- Pass-through window: gradual accumulation over roughly 7 months from implementation — meaning the 2025 tariff round's consumer-price passthrough is effectively at full completion around the 7-month mark.

→ Implied ex-tariff core PCE ≈ 3.2% − 0.8pp = 2.4%, putting the underlying reading effectively inside the Fed's 2% target band.

(6) Policy implications of the three numbers

What matters isn't that the three readings split cleanly into separate "policy stances" — it's that the spread between the three measures itself acts as a narrative lever.

- Core CPI 2.6% → 2.8% (Mar → Apr 2026 / sticky but within the prerequisite range),

- Core PCE 3.2% (100 bp from target),

- Ex-tariff core PCE ~2.4% (inside the target band) — where you place your prior across this ~100 bp spread is what splits the hawk and dove camps' framing.

The Bessent–Warsh regime's inflation prerequisite turns not on which side of the spread is "correct" but on whether Fed staff are actually using the ex-tariff reading in their internal assessment and whether the market is pricing that in.

- The Fed staff tariff study is closer to a reference point demonstrating that the internal reading skews ex-tariff — it isn't, on its own, an argument justifying a dovish narrative.

- The spread narrows toward disinflation, and the prerequisite holds, only when two conditions are met simultaneously: no Tariff Round 2, and oil price increases not spilling over into consumer-side inflation concerns.

If either condition breaks, the hawk camp's Core PCE 3.2% reading hardens into the base case — and the rationale for the Fed's RMP, the "ample reserves" framing, risks colliding directly with the inflation mandate.

The most visible variable testing this prerequisite — the lagged passthrough of the February 28, 2026 oil shock — is taken up in Part 2.