Macro Check, Oct 21-25 2024

1. The Switch in the Liquidity Source

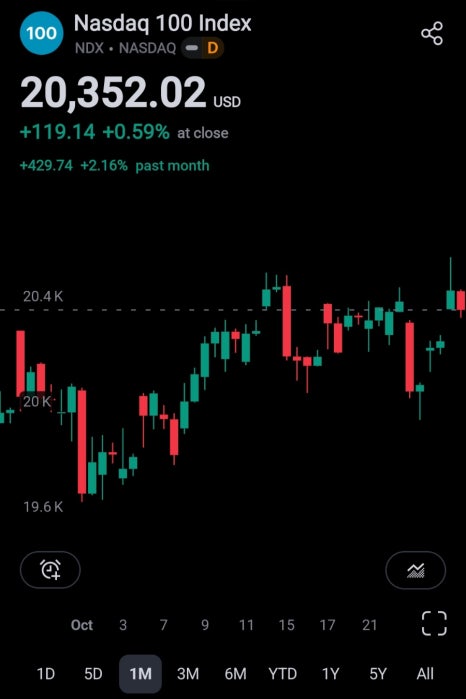

US equities are printing record highs day after day. The S&P 500 is at a new high in the 5,800s, the Nasdaq 100 at a new high in the 20,300s.

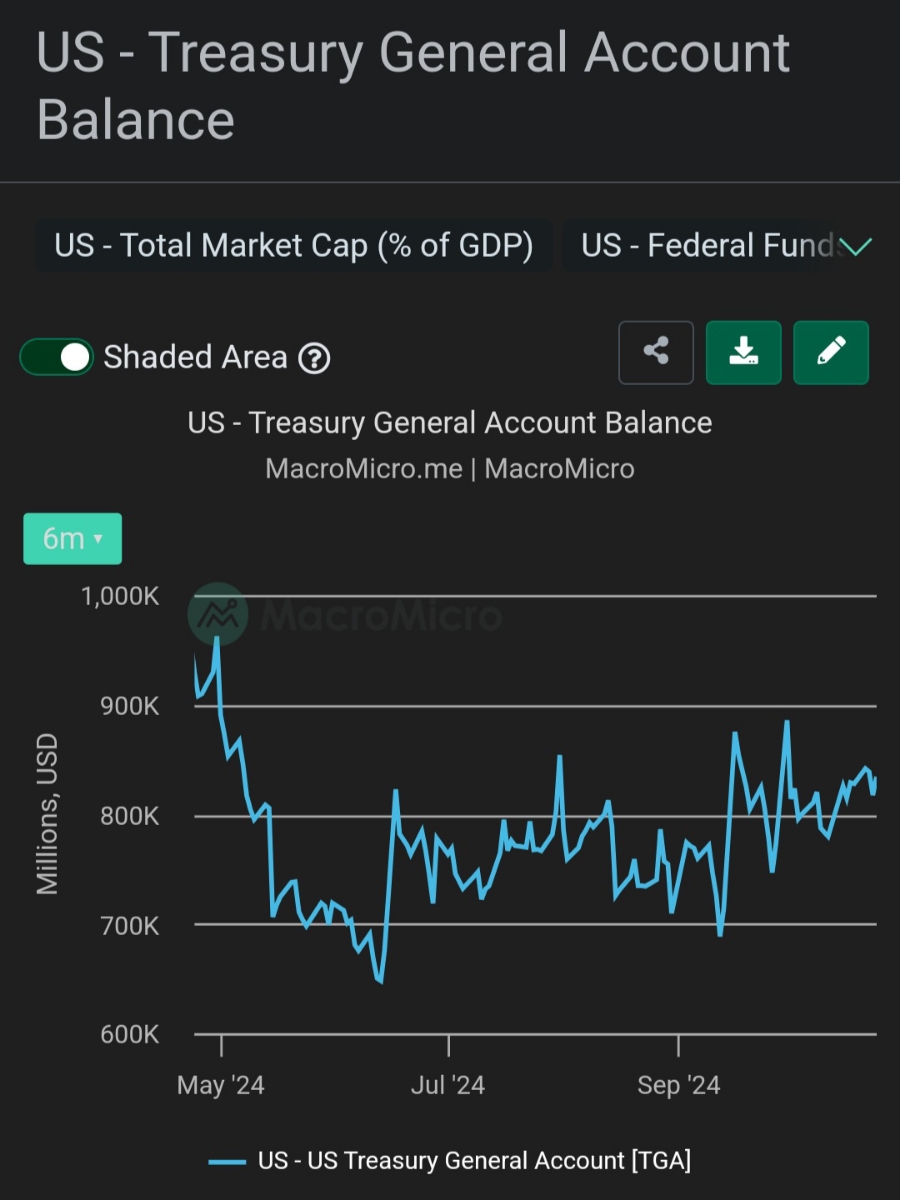

As stressed before, index gains are made by rising inflowing liquidity, so monitoring the liquidity source is important for portfolio-volatility management. The base scenario under the prior assumption was Yellen draining the Treasury TGA balance to prop equities for a Harris win. Is it materializing? Look at the TGA Account Balance.

As shown, the TGA balance is not falling — it has been refilling since September, contradicting the Treasury's previously announced Q4 2024 QRA spending plan. By plan it should have drained the TGA to supply liquidity (balance falling); reality is the opposite.

Recognizing Yellen's supply plan has been revised, consider her posture and the liquidity source now. With the market at record highs on solid earnings, there is no need for the Treasury to step in and release cash. Propping via TGA drawdown would, as the balance falls, raise inflation-reignition fears and pressure long-end yields up — ultimately a bigger problem of inflation and rising interest cost. Yellen's prop plan presumed Trump and Harris were close; the market is already trending to bet on a Trump win.

The key question: if not the Treasury TGA, where does the liquidity come from?

2. The US Domestic Liquidity Environment

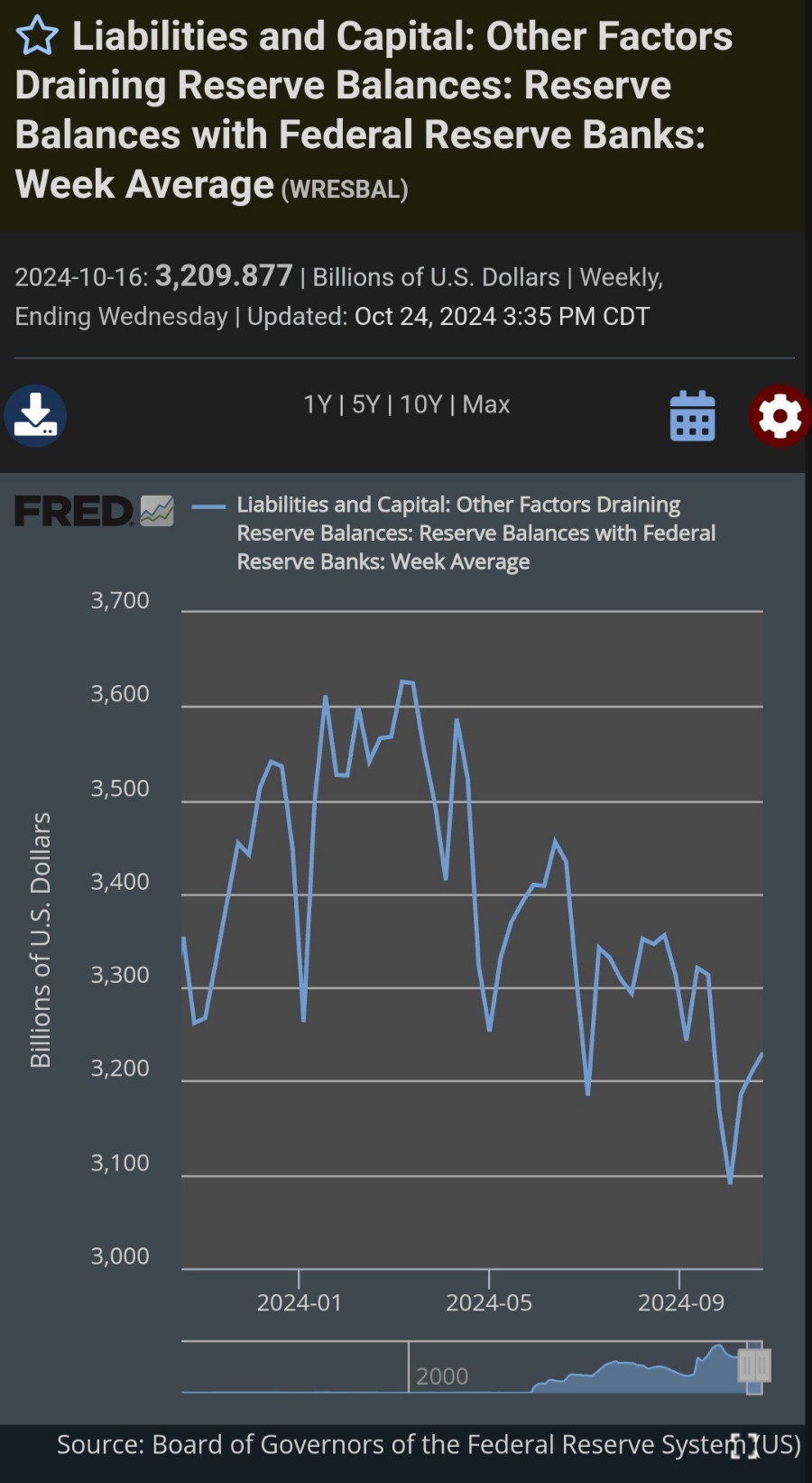

Bank reserves — highly correlated with market liquidity — have kept falling since 2024, while the Treasury TGA balance refills.

Either way the Fed continues tightening and the Treasury is absorbing liquidity — the US domestic situation is not cooperative with rising liquidity.

3. The Return of the Yen Carry Trade

Stepping out of the US lens into the yen lens. From September to now USDJPY has kept strengthening (continued yen weakness).

Hypothesis: on Sticky-Inflation concern, US Treasury yields kept rising over the past month despite the Fed's cut. A yield environment was created that encourages the re-emergence of the carry trade — borrow and sell funds in a low-rate country (typically Japan), convert to dollars, and invest in Treasuries / equities for a higher risk-free return. So despite the cut, an environment formed for yen-carry funds to return to the US. With a pillar now (at least temporarily) supporting equity liquidity, the Treasury gained a reason not to enter a prop that risks inflation reignition.

(1) The motive — rising Treasury yields

Despite the Fed's cut, yields kept rising over the past month.

Why? Bond-market participants worry inflation won't resolve as easily as expected, so the Fed cannot cut as fast as planned. This sentiment is reflected in the market: demand rises for bonds with high nominal rates to compensate inflation-eroded purchasing power; newly issued bonds offer higher rates, and existing bond rates adjust in the market.

(2) Hypothesis review

In the Aug 12–16 2024 note I noted the hypothesis that USDJPY, once at ¥140, would return to the ¥150–160 range. With downside risk cleared, US major indices / stocks / Treasuries were quite cheap in yen terms, so the fear zone could be a good entry zone for hedge funds. Further, despite a cut that would raise yen-carry-outflow risk, rising Treasury yields became a motive that instead encourages the carry.

The two big roots of 2024 equity liquidity are yen-carry-based funds and the US Treasury TGA balance (noted in the Aug 19–23 2024 note). By plan, yen-carry funds would shrink relatively while the TGA released, raising liquidity to lift H2 equities. Reality differs — the TGA keeps refilling, and returning yen-carry funds support the rise.

(3) Net: more uncertainty

Under the prior "TGA-drawdown supports the rise" assumption, one only had to monitor how long the TGA's residual cash could support equities. But now, with the TGA not draining and yen-carry funds doing the support, variables multiply: (i) the range of the US-yield rise, (ii) USDJPY, (iii) the Trump–Harris election probability. In an environment of falling reserves and a refilling TGA reducing liquidity, one must keep monitoring how long the yen carry persists and whether it can keep supporting the rally.

4. Conclusion

Despite the Fed's cut, inflation-persistence / reignition concern lifted Treasury yields and, coincidentally, brought yen-carry funds back to US equities — not a long-run move. Watch points:

- Solid earnings help the rise, but PER is broadly high. However good a company's earnings, a relatively high PER tends to revert to the historical average or below — time to trim the portfolio.

- The market shows inflation-reignition concern. Build appropriate scenarios; a Trump win raises the odds of higher government spending — negative for inflation and Treasury yields.

— Aside: note uploads have been sparse for ~a month. I enlisted in early September and, after seven weeks of army boot camp, am in follow-on training. Being cut off from the world forcibly avoided short-term noise. This is the first note post-enlistment; I'll be active as before going forward.