Q2 2025 US TGA Funding and Liquidity Outlook

Analyzing the US Treasury TGA balance — one of the core system-liquidity gauges — and a medium-term liquidity outlook through the lens of the debt-ceiling negotiation.

1. Where Things Stand

On Jan 21, 2025 the US Treasury entered a Debt Issuance Suspension Period. Issuance had neared the $36.104T ceiling, so from then it secures headroom via extraordinary measures. Given the TGA ran $500B–$600B in Feb–Mar 2025, the Treasury is inferred to hold ~$1.1T–$1.2T of capacity through two extraordinary measures.

The Treasury currently cannot do net issuance (gross issuance − maturities − central-bank purchases) and the TGA is draining. Net issuance absorbs system liquidity into the TGA, so the current TGA situation is, at least short-term, a positive for financial-market liquidity.

2. Probable Timing of a Deal

Measured against the X-date — when the TGA balance (including extraordinary-measure funds) hits zero — two outlooks exist. On balance, the probable window for a debt-ceiling deal is sometime between April and August 2025.

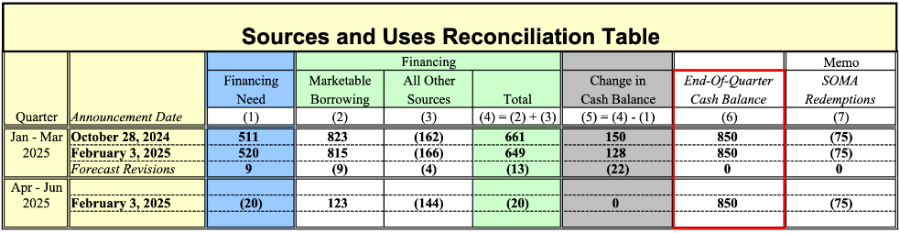

3. The TGA-Refill Liquidity Source

After the 2023 debt-ceiling deal, refilling the TGA occurred with a substantial $2.25T RRP balance present. The cost of the Treasury's issuance could thus be cushioned by draining RRP, softening the system-liquidity absorption shock — the correction stayed around −10% on the S&P 500.

(purple) the TGA refilling after the '23 debt-ceiling deal / (green) effective reverse-repo balance excluding foreign-official deposits / (candles) S&P 500 over the period → −10% correction

Now it is different.

The Treasury's Q2 2025 QRA shows a TGA target of $850B through Q2.

Both the Fed and the Trump administration are aware of this. Since a liquidity source to fill the TGA must be arranged, the key is to shift the buyer of Treasury issuance from MMF money parked in RRP toward commercial banks.

4. Preventing Inflation Reignition, and What to Watch

For this plan to run smoothly, inflation reignition must be prevented. The point to keep monitoring is whether the RRP balance declines. If cash that flows out of the TGA goes to RRP rather than commercial-bank reserves, it provides no increase to system liquidity at all.