Q2 2025 QRA Update and the Risk of a Q3 Correction

The US Treasury's late-April QRA (Quarterly Refunding Announcement) is out. A short follow-up analysis.

1. The Q2 2025 QRA Update

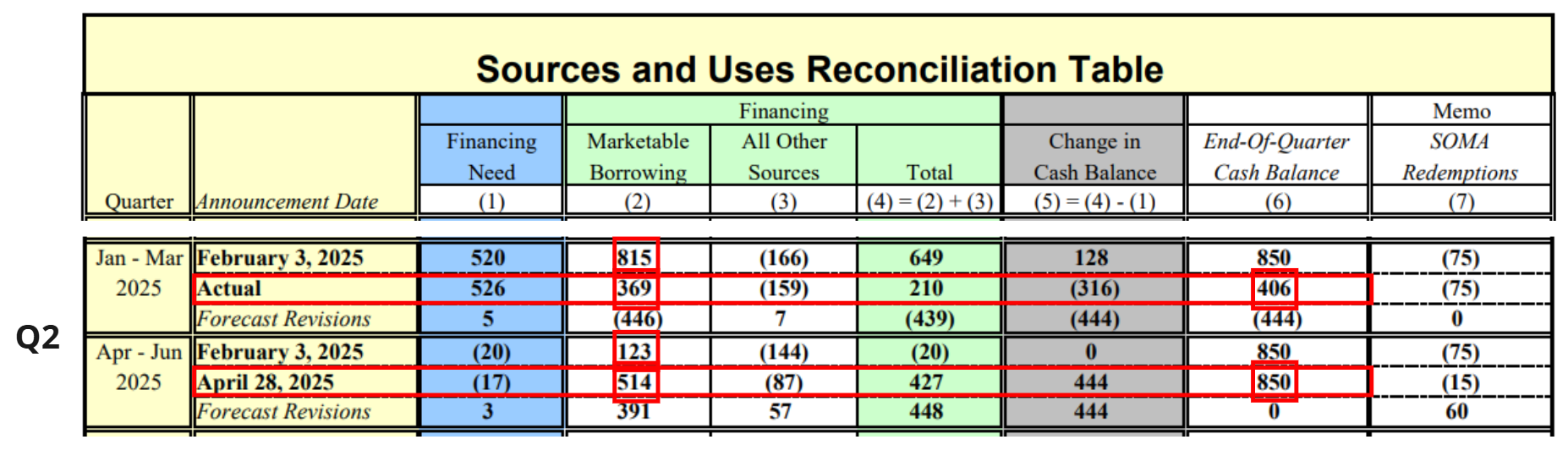

The Target Balance (End-of-Quarter Cash Balance) is set at $850B, same as Q1, but the following are worth noting:

- Q1 estimated vs actual borrowing gap: the estimate was announced at $815B but actual was $369B, and the end-of-quarter cash balance finished at $406B vs the $850B target.

- Raised Q2 borrowing estimate: from an initial $123B to $514B.

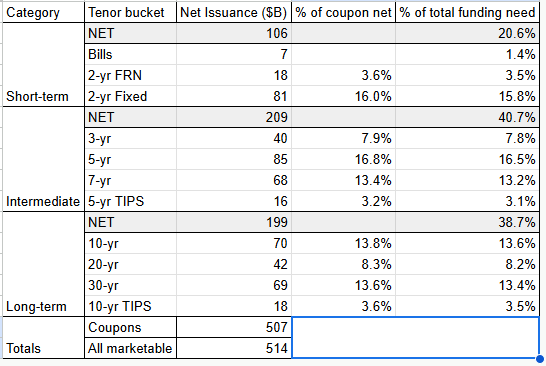

(1) Implied Bill Funding

Vs 2024, the bill issuance amount has fallen markedly, and the mix is gradually widening toward bonds.

2. Implication

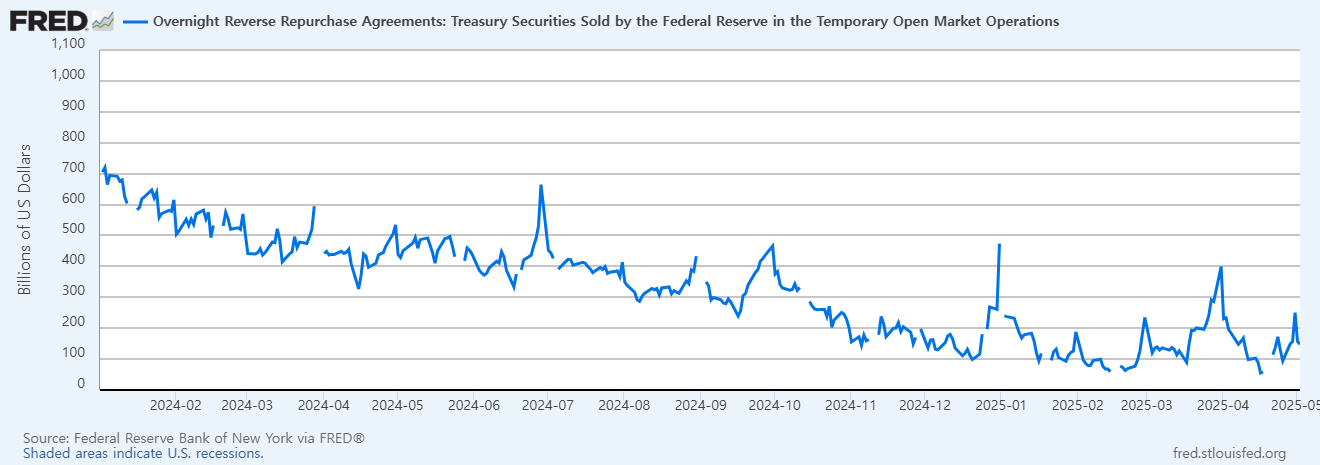

In the debt-ceiling liquidity note I described the post-2024 TGA funding environment and its risks. In short, the reverse-repo balance that had been 2024's TGA funding source is near depletion, and a clear means to absorb the $514B borrowing is currently uncertain.

That said, the $514B estimate is not an immediate concern. That borrowing plan is valid only on the assumption the government receives debt-ceiling approval within Q2 2025. Currently, additional issuance is constrained.

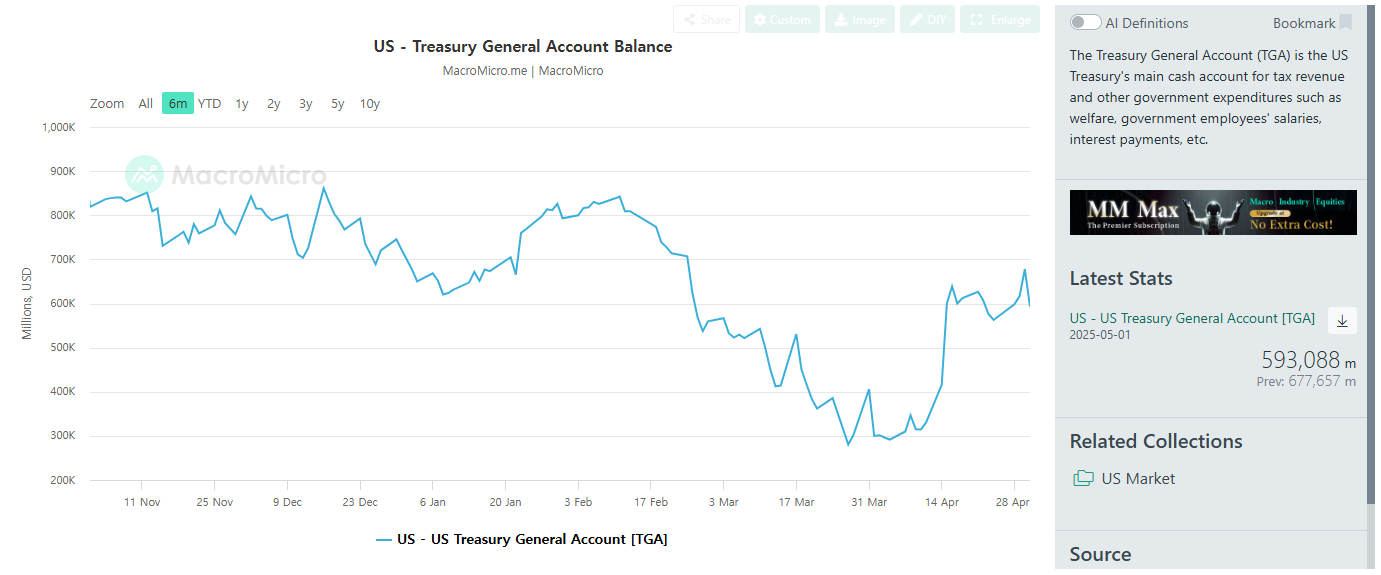

The short-term focus is how the current TGA balance of $593B reaches the $850B target. The funding scale shrinks by nearly half, to $257B. The key: until a debt-ceiling deal, this is not an immediate Q2 worry.

3. The Risk of a Q3 Correction

(1) The BOJ hike question and a possible short-term yen adjustment

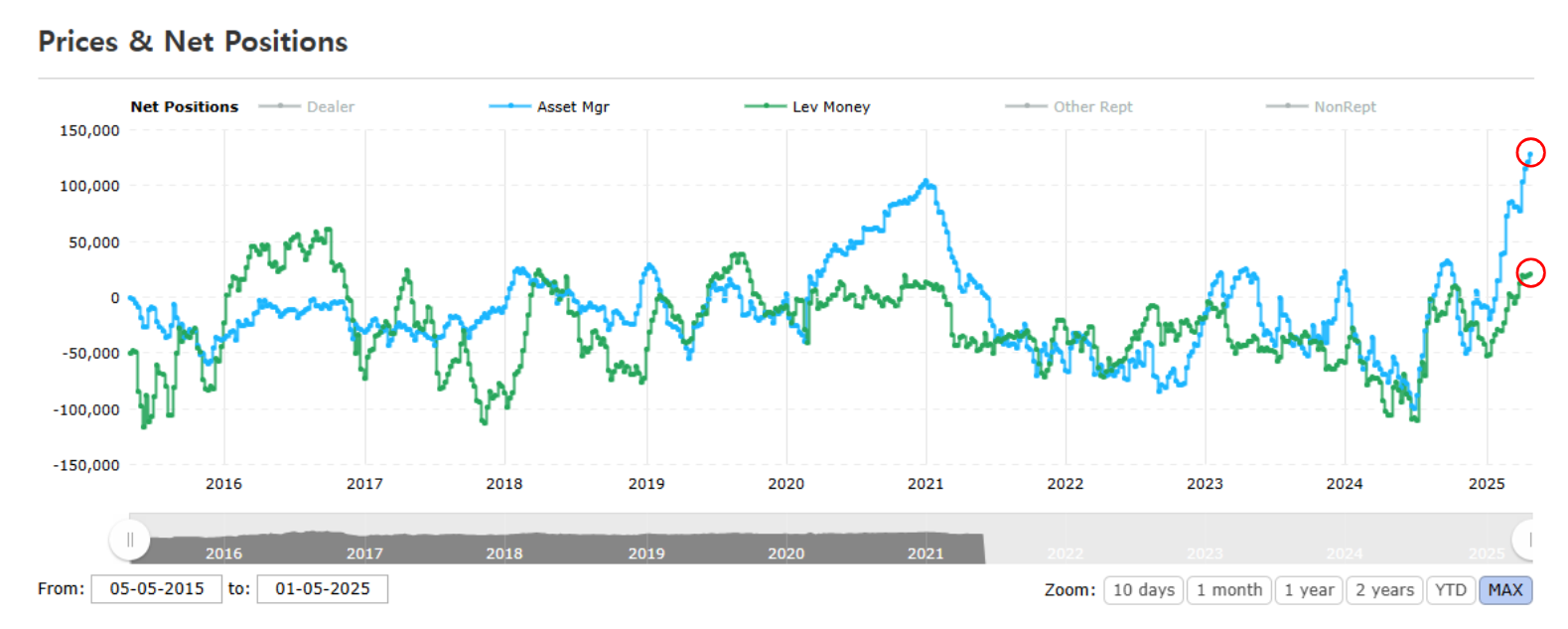

The COT (Commitment of Traders) report shows hedge-fund / institutional JPY-long bets in futures stacked at a record high.

With Trump tariff uncertainty weakening the dollar, the yen is turning somewhat stronger. USDJPY broke sharply out of the safe 150–160 range in early April.

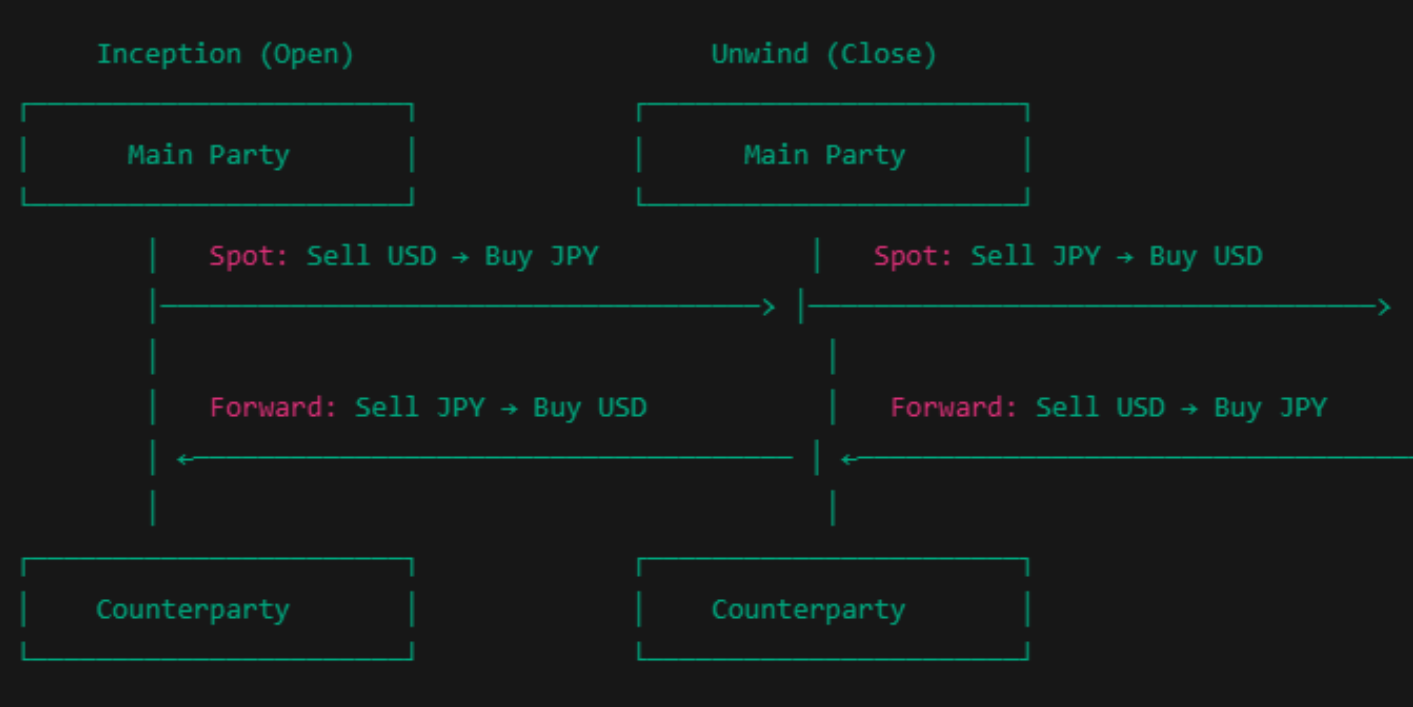

Given the structure of the FX-swap trade (sell USD to bet on yen strength), when the trade unwinds (sharply) the dollar in the forward contract is recalled; as the dollar supply circulating in the market shrinks, dollar funding cost spikes, and banks / MMFs become reluctant to lend dollars — a capacity overload.

The factor that would trigger this is the June 16 BOJ policy meeting. If the BOJ does not hike, a short-term yen adjustment is likely. With a record JPY-long position stacked in futures, a wave of selling can hit; once the selling begins, the yen can correct sharply and the FX-swap unwind plays out.

(2) TGA funding and the tariff shock

The hard data so far describes the pre-tariff economy. The tariff shock may therefore become visible from the June data. The TGA X-date is hard to pin precisely, but I place it between end-Q2 and early-to-mid Q3. From then, a TGA-funding correction must also be on the radar.

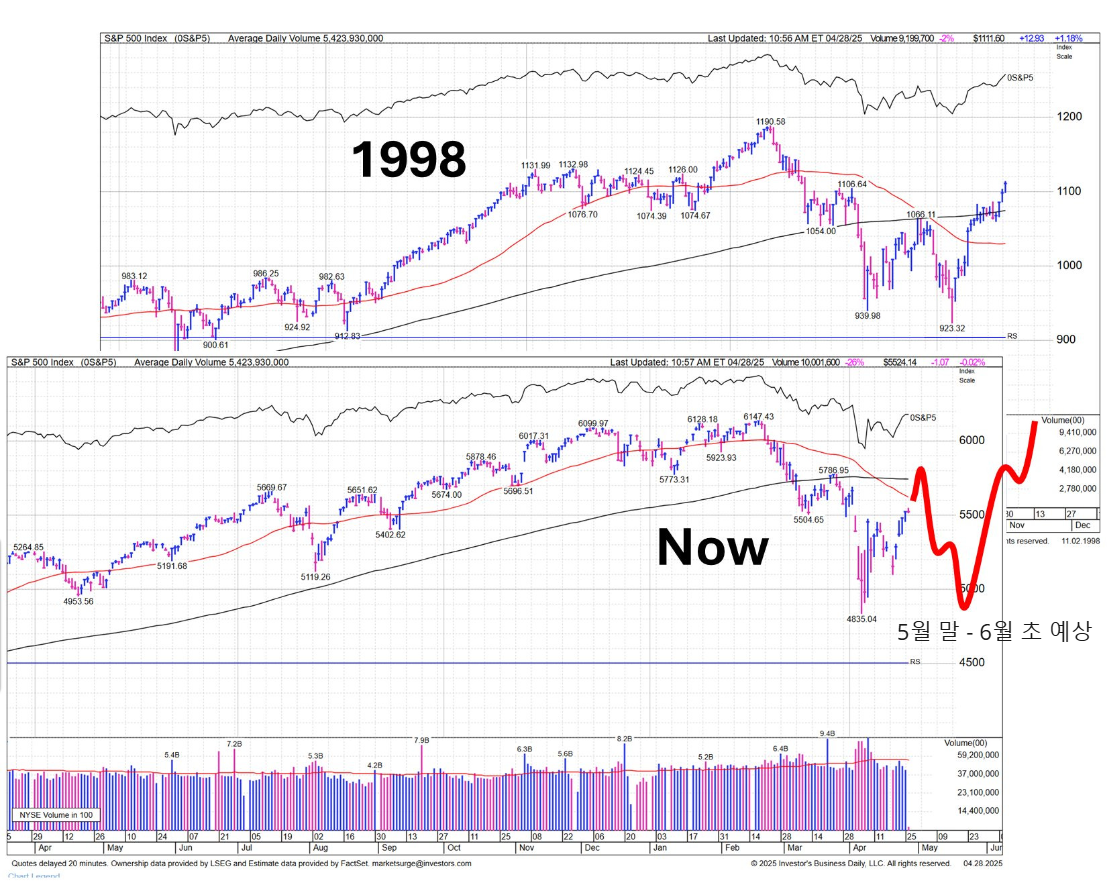

4. Summary

May is likely to remain a liquidity-driven tape amid doubt and unease, but I see a high probability that the downside resumes in June. I have the following scenario in mind.