Q2 2025 Settlement

1. Net Trade P/L, Trade History & Evaluation

The Q2 Net Trade P/L accounting first.

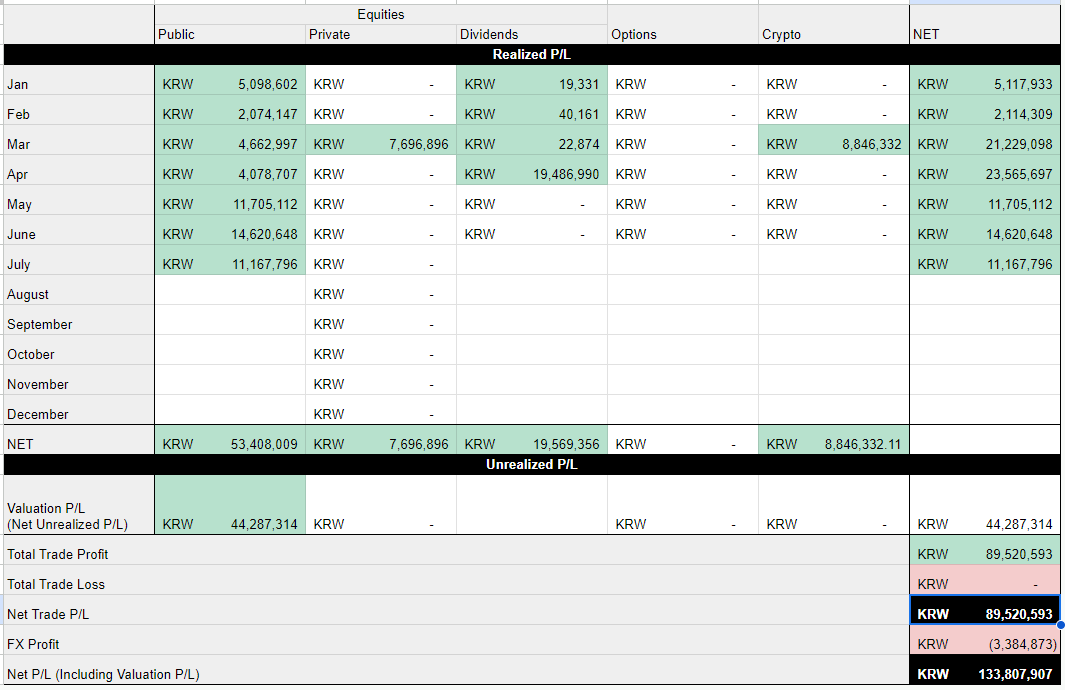

[Table 1] P/L Log through Q2 '25

- Total realized P&L YTD '25: KRW 89,520,593.

- Q2-only realized P&L: KRW 49,891,457

- Including unrealized KRW 44,287,314, total to date: KRW 133,807,907.

- July started with realized P&L KRW 11,167,796.

[Table 2] Public Equities trade record

- April: in a market rising slowly amid unease after macro volatility peaked, took profit for temporary cash. $PLTR was the sacrifice.

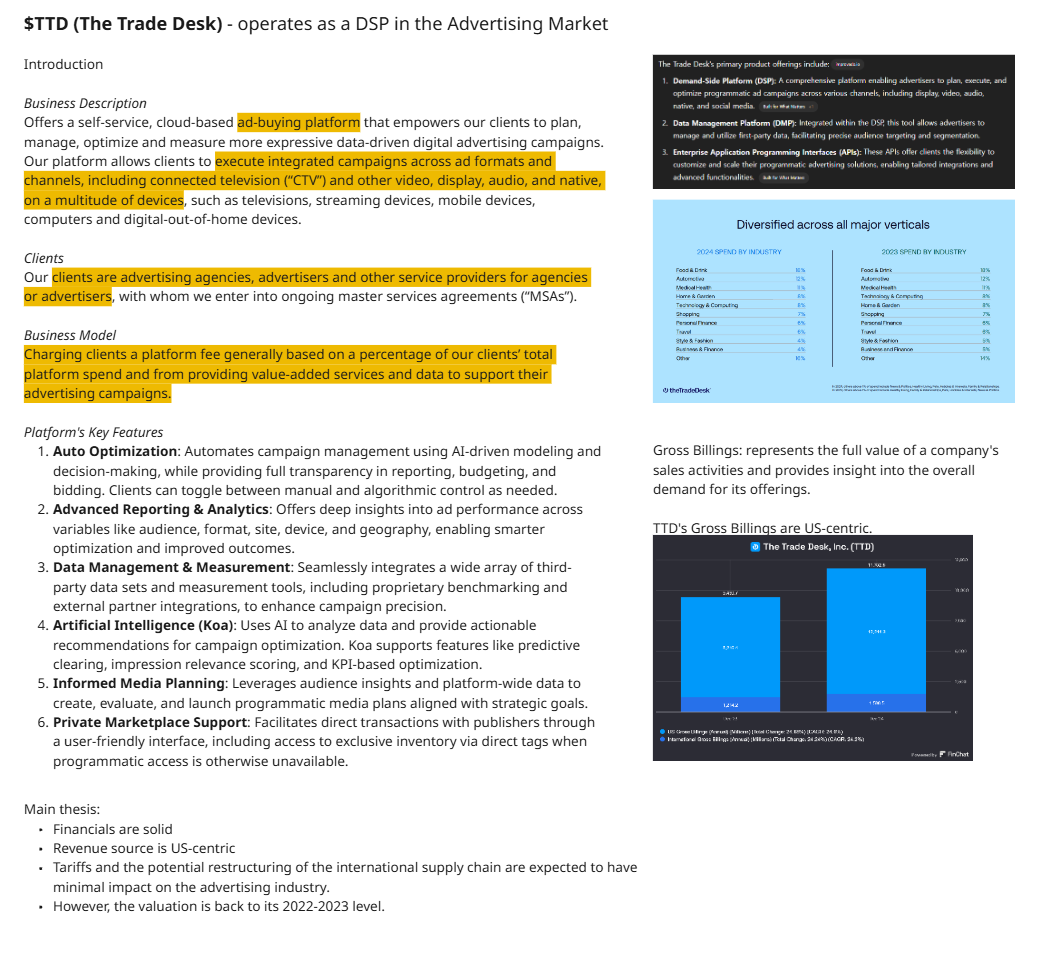

- May: one of the names held in the April correction for short-term volatility — the cloud-based ad-buying platform The Trade Desk ($TTD). Amid heavy reciprocal-tariff noise:

- (1) despite sound financials, the valuation had reverted to 2022–23 levels,

- (2) revenue is centered in the US,

- (3) regardless of reciprocal tariffs, the ad ecosystem is essential to maintaining/raising corporate revenue. For these reasons I (hurriedly) built a swing portfolio centered on ad-software main players.

A surface-anatomy doc written hurriedly within an hour.

[Chart 1] $TTD Trade Log

- In conclusion, a fairly satisfying trade within a month — avg cost $52.12, final take $74.63.

- June:

- On rising Iran–Israel geopolitical risk, expecting some downside, cashed out part of a near-0%-cash portfolio ($VRT·$VST·$ANET).

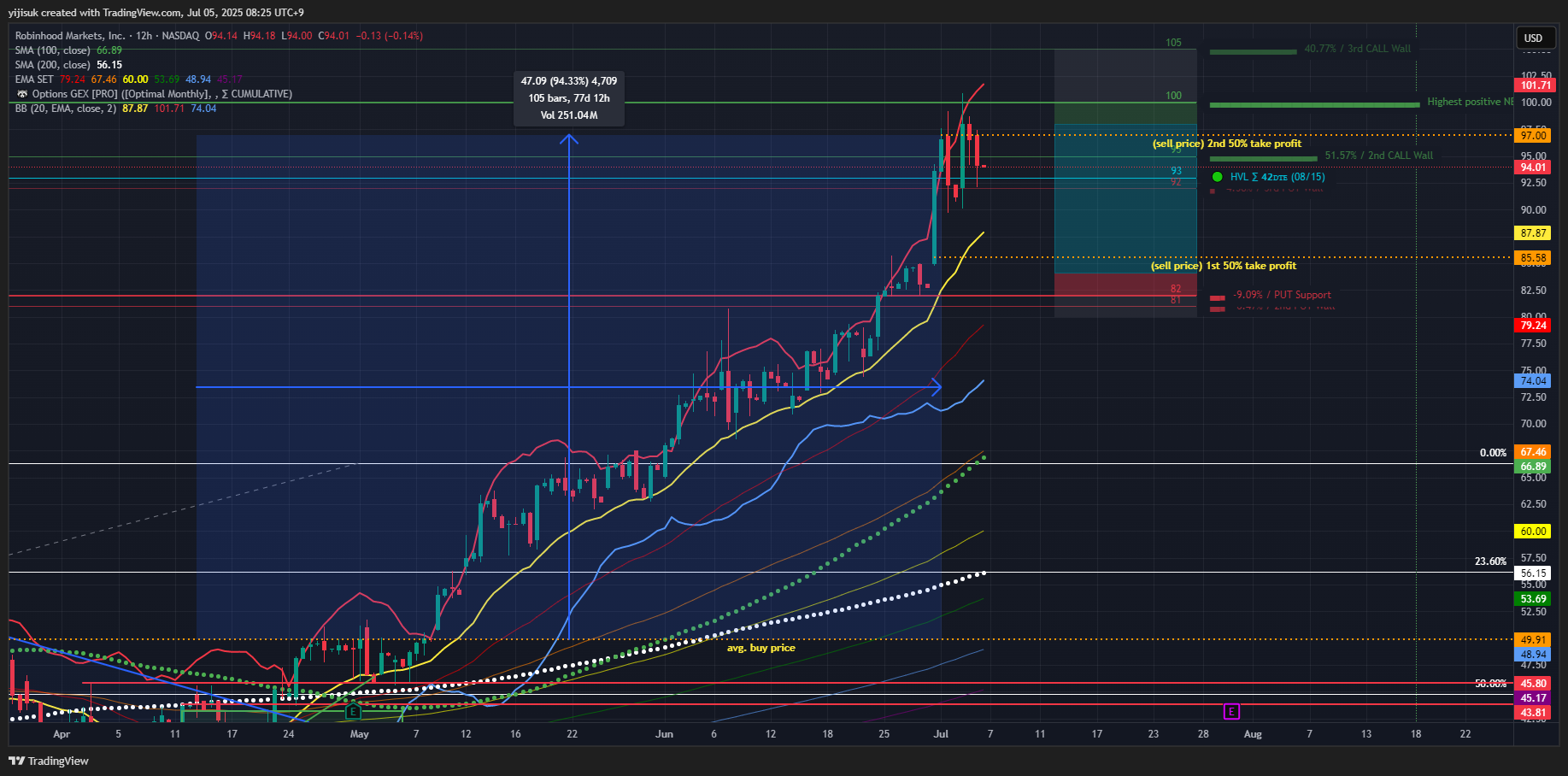

- $HOOD, judged near its target, half taken (split-sold across late June–early July).

2. Reflection — Q2 Market-Flow Overview

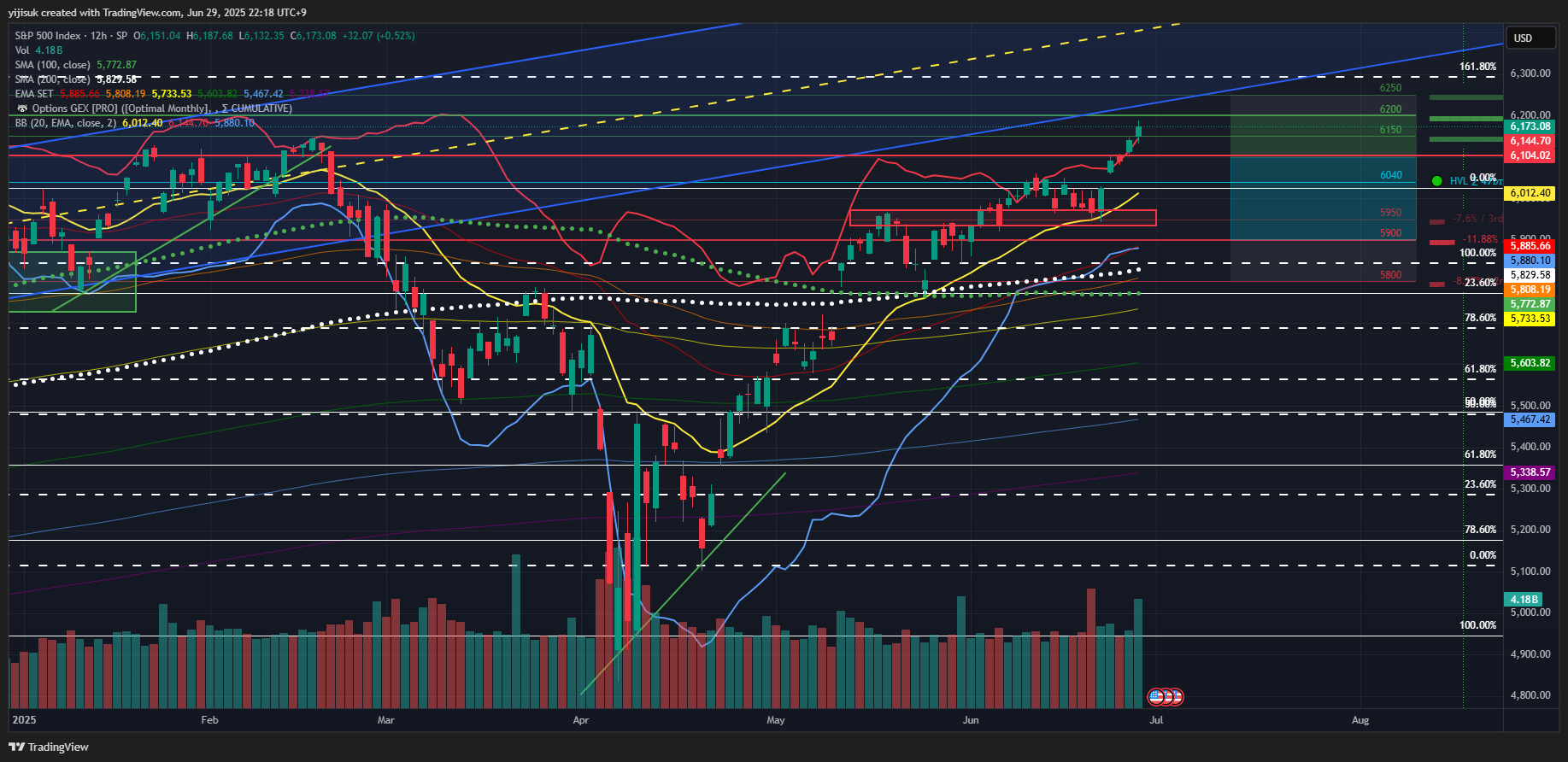

[Chart 3] S&P 500

[Chart 4] NASDAQ 100

Per the April '25 market-recap note: in April '25 the traditional correlation — equities down, long rates down — no longer held, since long rates rose even as equities fell.

- Before the reciprocal-tariff announcement, widening uncertainty had the market trim equity exposure and favor Treasuries / gold (a textbook move).

- After it, sudden dollar weakness (dollar outflow), centered on damaged trust in US exceptionalism, brought substantial volatility.

[Chart 5] US 10Y Treasury yield

[Chart 6] US 30Y Treasury yield

[Chart 7] DXY

The sharp yield rise raises not only future-issuance demand uncertainty but the government's interest-cost burden. Trump eventually capitulated with the 90-day reciprocal-tariff pause, revealing to all that the weak point is Treasury yields. Whether or not the economy enters recession this year, judging the possible uncertainties were already all disclosed, the market moved to pre-price.

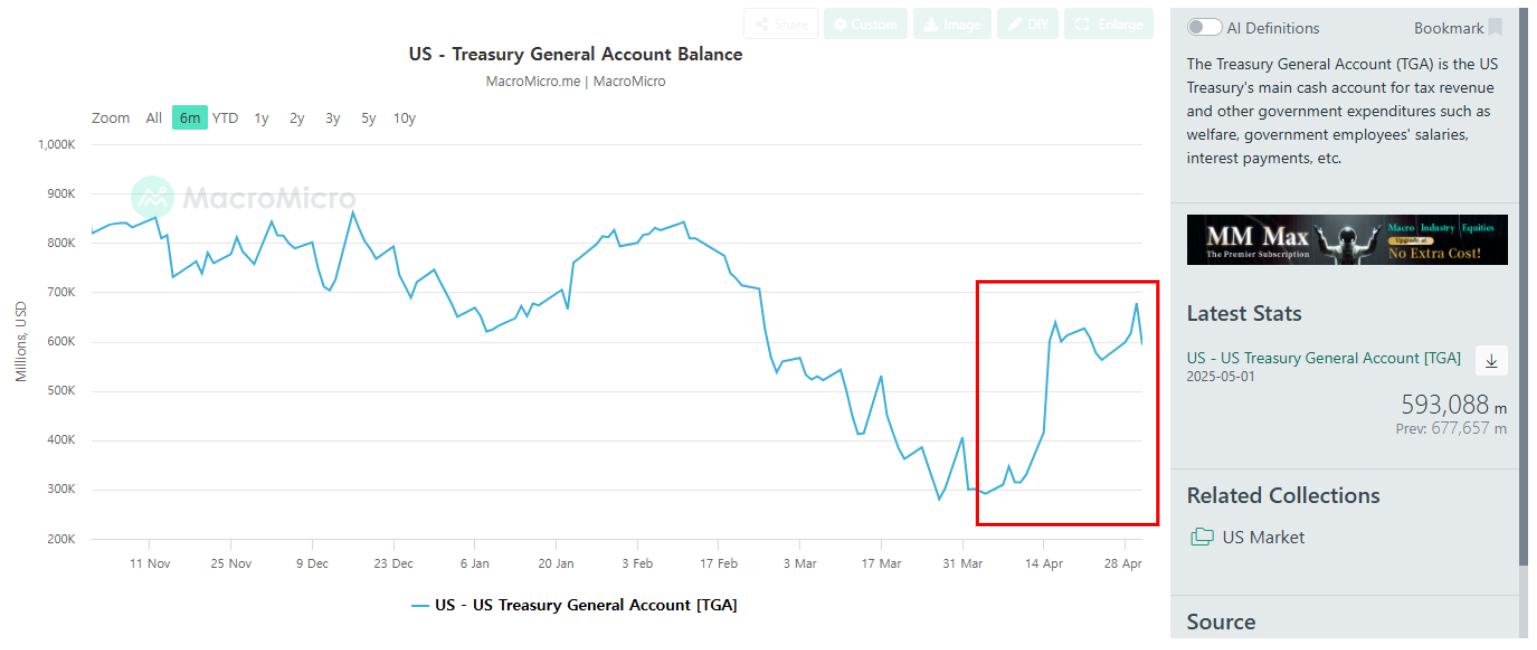

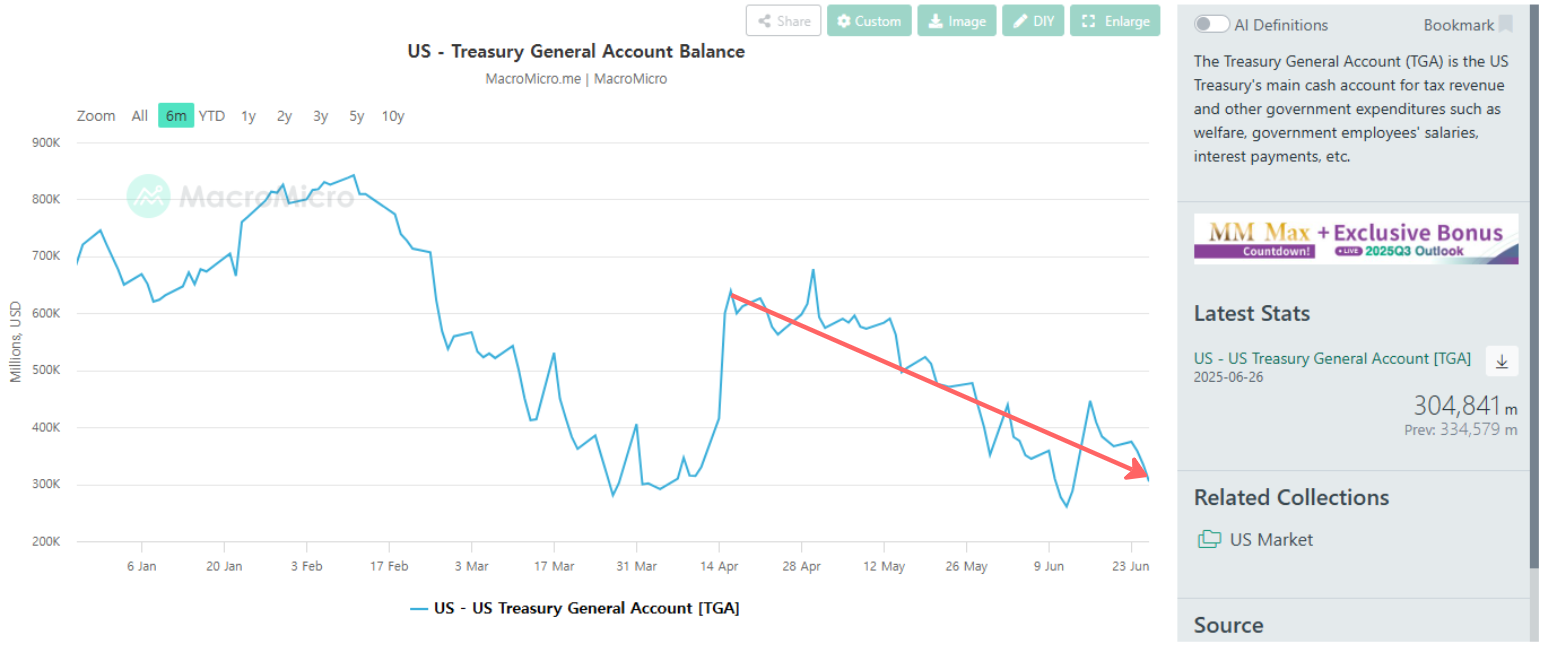

While the market focused on geopolitics and recession odds, the April tax season passed quietly and refilled the TGA. From late April to mid-May, corporate buybacks and earnings season began in earnest, and the market kept rising slowly amid doubt. The factors behind the rise:

(1) On the surface

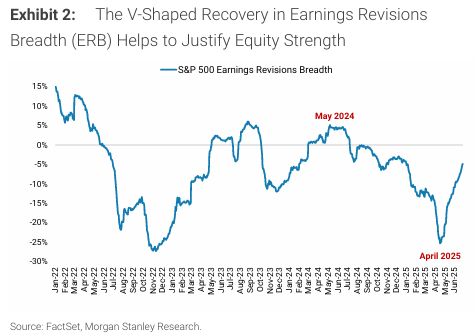

- AI demand's scale and persistence, proven by big-tech results — NVIDIA, MSFT, Google, Amazon posted results beating expectations; cloud AI revenue surged, clearly showing AI-infrastructure investment in earnest. They guided further AI CAPEX expansion with strong confidence in long-run growth — driving the whole AI value chain higher. Earnings Revision Breadth (ERB) bottomed in April and rebounded (coincidentally the equity bottom).

Earnings Revision Breadth (ERB)

- Trump's Middle East sales.

- Reciprocal-tariff negotiation progress with major economies.

(2) From an underlying-liquidity view

Liquidity-release trend

From mid-to-late April, after the TGA refilled, liquidity release persisted.

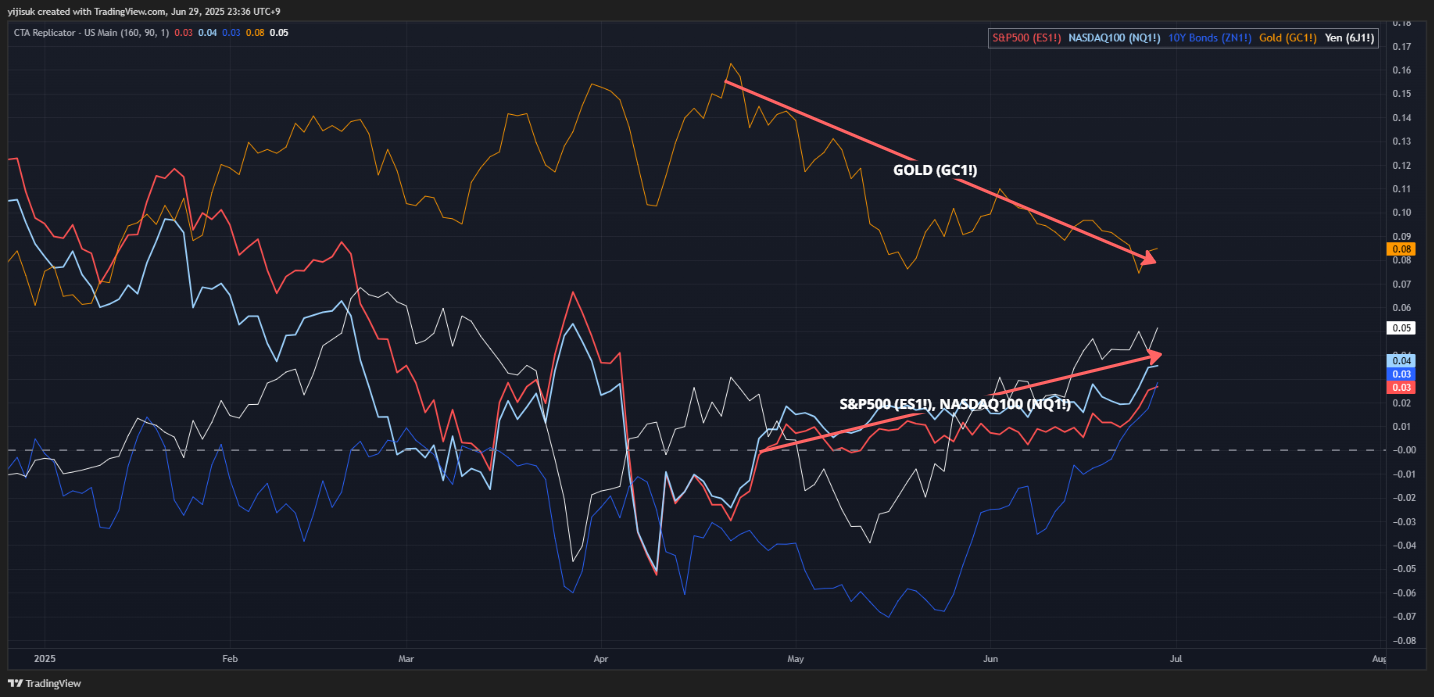

[Chart 8] CTA Replicator

From late April, CTA trend-following on the S&P 500 / NASDAQ 100 turned net-long and GOLD trend-following momentum declined.

[Chart 9] GOLD

Gold, after the sharp run-up through April, is range-bound.

3. Bird's Eye View — Entering Q3

comment: in the first week of July when writing this, Trump's One Big Beautiful Bill (OBBB) Act passed sooner than expected. Some in-progress content judged no longer valid was cut decisively, but some may still feel timeline-awkward. Added comments are italicized.

- Focus shift: with Iran–Israel risk easing, attention returns to Trump tariff policy.

- Key variables

- Surface: July 9 reciprocal-tariff pause expiry. How Trump adjusts the expiry under the tariff–real-economy–bond-market trilemma, midterms, geopolitical burden, and his stance-change potential.

- Deep: the change in system liquidity through a TGA lens, around the debt-ceiling negotiation.

- Macro data: inflation / employment prints before the July 30 FOMC are key variables in the rate-cut debate.

Key July schedule:

- Jul 4: OBBB (tax and spending package) expected passage (per Scott Bessent) → as of Jul 4, passed both chambers; only the signing remains.

- Jul 9: reciprocal-tariff pause expiry → with OBBB passage, 10–70% tariffs flagged from Aug 1.

- Jul 14–18: House crypto week; GENIUS Act (stablecoin codification) House passage and CLARITY to the Senate (per David Sacks).

- From Jul 15: Q2 earnings season.

- Jul 30: FOMC.

The key: the debt-ceiling deal must close within July.

- Jan 21, 2025: the Treasury entered the Debt Issuance Suspension Period (DISP).

- Currently financed via special accounting measures rather than additional issuance.

- Treasury Secretary Scott Bessent extended the measures' deadline to Jul 25, 2025.

comment: passed comprehensively with OBBB on Jul 4. Includes a $5T statutory debt-ceiling increase.

X-Date when?

- CBO (Congressional Budget Office): mid-August to end-September.

- JP Morgan and other major IBs: between August and October.

4. The Debt-Ceiling Lens, and TGA Liquidity Absorption

Trump insists his tax bill (OBBB Act) and the debt-ceiling increase must be linked — not the ceiling alone, but tax cuts + ceiling as one package passed by Jul 4. Two factors to note:

- US default risk from a delayed debt-ceiling deal (an effectively extinguished risk)

- Post-deal liquidity absorption into the TGA via issuance → system-liquidity-decline risk

Risk 1:

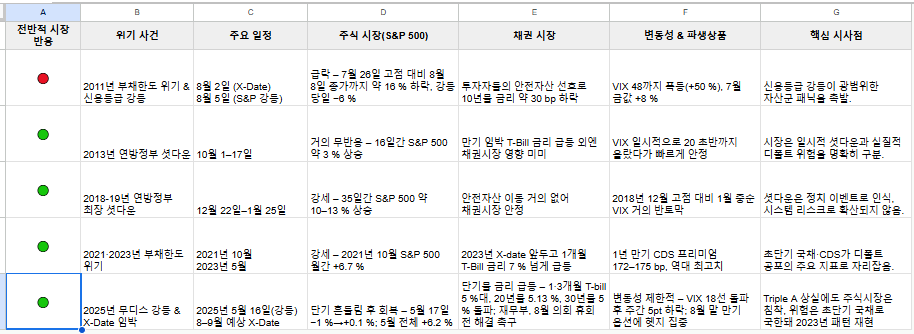

US default-risk trend

US default risk is not new — participants keep adapting.

Risk 2 (assuming an eventual deal):

- After the '25 DISP entry, the Treasury released liquidity by drawing down the TGA and deferring pension Treasury reinvestment / interest payments.

- Reserves rose as a result, and funds flowed heavily into MMFs and the repo market.

[Chart 10] Reserve Balances with Federal Reserve Banks

[Chart 11] Effective reverse-repo balance excluding foreign-official deposits

Note: ON RRP is the Fed's device to temporarily absorb market cash via bonds. Foreign institutions (FIMA) use ON RRP via a separate window and move independently of US domestic flows; excluding them measures the domestic short-term supply-demand balance accurately. Residual as of Jun 30, '25: $237.31B.

- Ultra-short rates trended down (charts 12·13·14).

[Chart 12] 1-month bill yield

[Chart 13] 3-month bill yield

[Chart 14] 6-month bill yield

- DISP provides temporary money-market easing, creating a short-term-investment-friendly environment. But the TGA-release liquidity expansion is temporary.

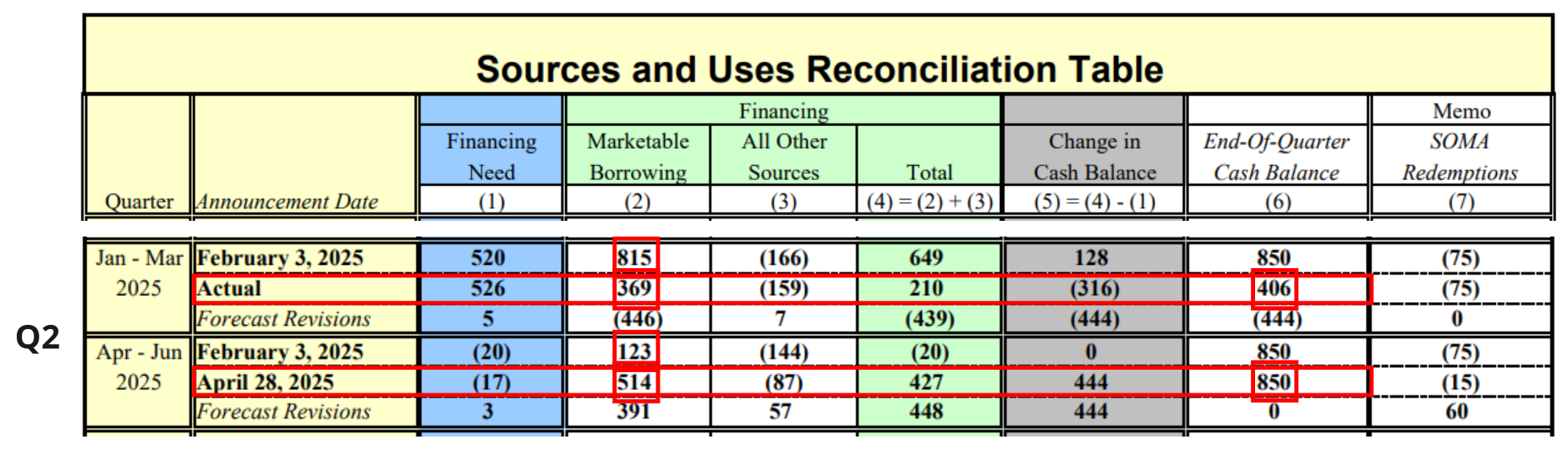

TGA Funding scenario

- Post-deal expected Treasury TGA borrowing $514B (per the late-April '25 QRA).

- Concern: the (effective) ONRRP that was 2024's TGA funding source is an uncertain size to absorb a $514B draw.

- To arrange liquidity sources, the GENIUS Act (stablecoin) and the Fed's SLR easing were likely (well-timed) enacted before the negotiation point.

Note — GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act): the first US federal framework regulating stablecoins. Issuers must hold (1) 1:1 high-liquidity reserves of cash / short-dated US Treasuries, (2) monthly reserve disclosure, (3) annual external audit, (4) a statutory redemption right protecting customers even in bankruptcy. Pegging each digital dollar to immediately redeemable collateral (reserves parked in short-dated Treasuries) builds a reliable real-time settlement framework, encouraging banks / payment networks / firms to adopt it — improving speed and cost, and ultimately serving as a liquidity source across crypto and traditional finance.

Note — the Fed's SLR easing: SLR (Supplementary Leverage Ratio) is the US bank-leverage rule (capital-to-total-assets ratio). The stricter (higher) it is, the more capital banks must hold. On Jun 25 the Fed announced an easing (60-day comment → final ~4–6 months → effective 6–8 months). The core goal is improving US-Treasury-market liquidity. The prior all-banks minimum 3% SLR + G-SIBs' extra 2–3pp eSLR (holding companies 5%, subsidiaries 6%) was said to constrain low-yield / liquidity-source trades like repo participation and Treasury buying. This easing applies eSLR at half the international standard — holding companies ~5%→3.9%, subsidiaries 6%→3.9% — letting excess capital flow into the Treasury market.

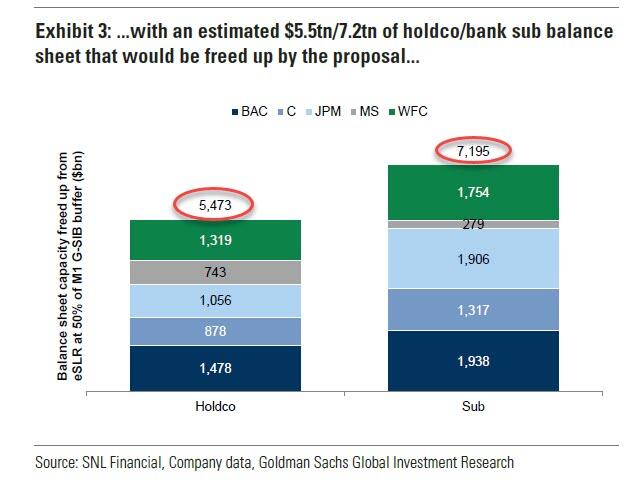

$5.5T capacity from SLR easing

Per a Goldman Sachs report: holding companies gain ~2.1pp average extra capital headroom (~$5.5T more asset capacity); subsidiaries ~2.8pp (~$7.2T capacity).

5. Forward Scenarios Centered on OBBB Passage

- The information that the post-deal TGA-refill liquidity source is uncertain is, of course, also known to the Trump side (which, as noted, is offering various responses).

- The factors hobbling Trump's tariff policy: recent geopolitical complexity, the policy's economic dilemma, potential bond-market tantrum.

- If the probability tilts toward the volatility-risk side, there is also a chance of re-pausing reciprocal tariffs on some pretext.

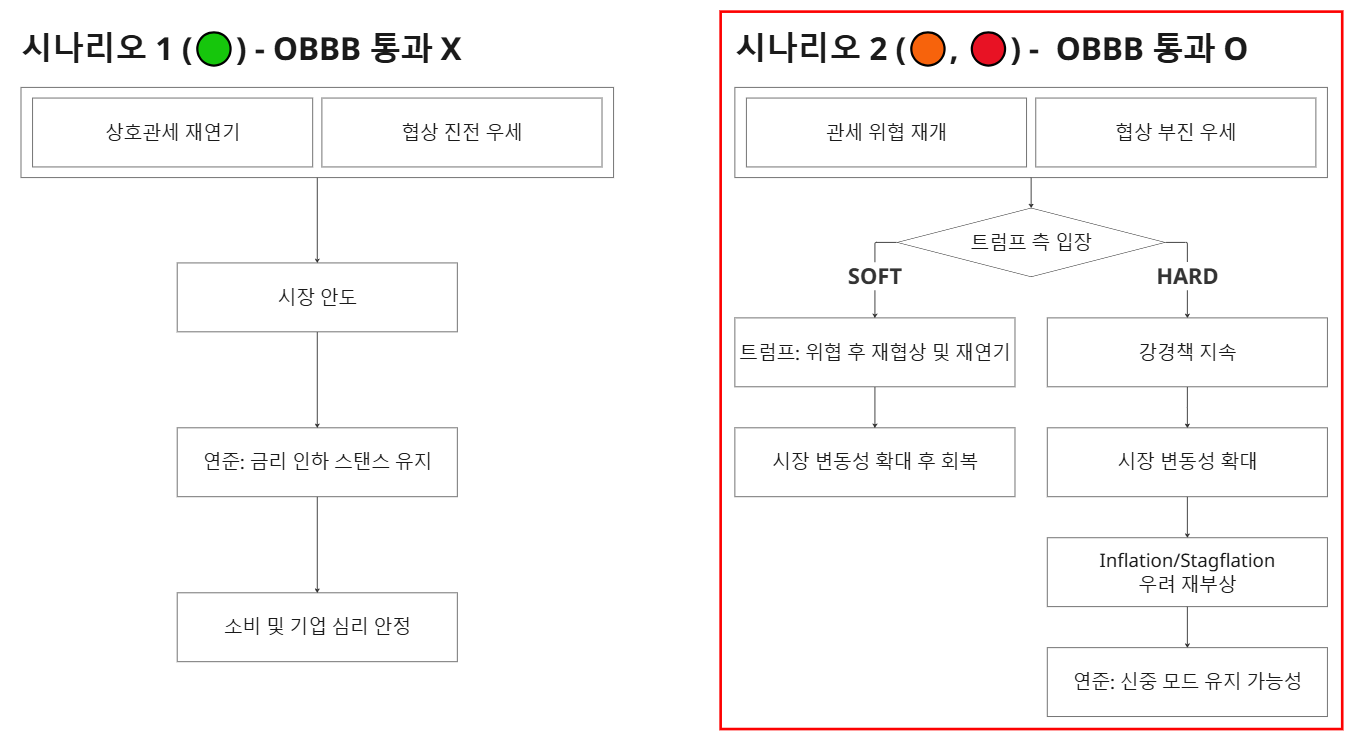

If OBBB does not pass — if Congress fails to pass OBBB by the Jul 9 expiry, Trump likely does not want expanded market volatility before the fiscal bill. If OBBB passes — with the fiscal direction confirmed, Trump may (short-term) push somewhat strongly, since he has the means to move liquidity per his master plan.

OBBB scenario branches

comment: after Jul 4 OBBB congressional passage was confirmed, I weighted Scenario 2 more.

After this was disclosed, as of 23:21 on Jul 4 when writing, the market (futures / crypto) shows a somewhat shared reaction.

In sum, I broadly consider Scenario 2's direction but think it too early for a concrete call. Considering the various possibilities, I'll approach with a moderate positioning across the branched cases. Current thought: potential re-spread of macro sentiment / geopolitical risk, and temporary TGA-absorption risk → considering (1) ONRRP residual, (2) OBBB passing both chambers before the TGA drains to zero, (3) the administration's stablecoin-based new-liquidity framework, the magnitude of correction I worried about in earlier notes seems excessive.

6. Conclusion

Lessons / thoughts from the Q2 retrospective:

- The prelude to a new liquidity regime — "digital liquidity" will soon become one of the main channels. Through Q1 I underestimated the administration's stablecoin-based liquidity environment. The system began to take shape, and via the bill-demand-oriented purpose + $CRCL's IPO + TradFi's USDC implementation, the stablecoin-ecosystem-led digital MMF became huge-if-true.

- I had tracked government financing referencing only legacy liquidity regimes like ONRRP, so I expected substantial liquidity absorption during the July TGA-funding period. But trusting and following Trump's approach, considering the various liquidity sources in preparation, the correction may be less severe than expected — still, short-term, July is a time to brace for some volatility.

- Ultimately the market converges to the aggregate value the constituent companies create, but short-term it is a game of expectations. Liquidity's acceleration on top finally produces volatility.

- The DXY has been forming a sustained downtrend channel since '25. Per Steve Miran's A User's Guide to Restructuring the Global Trading System, whether Trump formed the weak-dollar trend per the original purpose is questionable, but the earnings benefit of a weak dollar can't be ignored — a point to watch in the Q2 season from Jul 15. Still, long term, is there anything that surpasses dollar demand? Even if new liquidity demand is created, it will ultimately peg to USD.