Q3 2025 Settlement

1. Net Trade P/L, Trade History & Evaluation

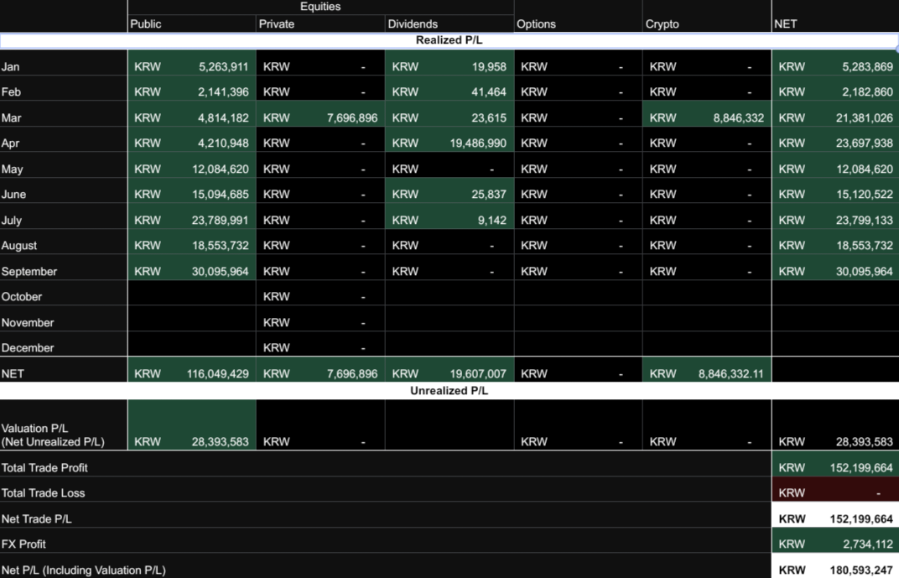

The Q3 Net Trade P/L accounting first.

[P/L Log through Q3 '25]

As of Oct 1, 2025:

- Total realized P&L YTD '25: KRW 152,199,664

- Q3-only realized P&L: KRW 72,448,829

- Including unrealized KRW 28,393,583, Net P/L to date: KRW 180,593,247

[Public Equities Trade Log]

(1) July

Given the local-minimum TGA balance early in the month, I judged TGA refilling would proceed from that month after OBBBA passage and the debt-ceiling deal. So I kept July trade frequency minimal, targeting cash, trimming names whose short-term attractiveness was spent — $HOOD (judged at its short-term target) and $META (right after the earnings surprise).

(2) August

Ahead of September seasonality I raised cash further by trimming (a) names with heavily concentrated weight and (b) some high-volatility names (aimed at lowering portfolio volatility, not profit-taking). $NVDA was 30%+ of the US-equity portfolio, so I cut 1/3 of the holding in a range. $TSLA / $BMNR were held on momentum, not valuation — cut decisively. In early–mid August, after OpenAI's GPT-5 launch, some data-center / neocloud / SaaS names corrected sharply on AI-capex noise; judging short-term attractiveness still intact, I accumulated some — neocloud: $ORCL·$CRWV·$NBIS, SaaS: $TWLO·$PINS.

(3) September

Entering a high-volatility regime, I raised trade frequency to capture short-term-volatility profit while setting cash-weight expansion as the main goal. September saw unexpected tail events formalize, favoring held neoclouds — partly luck.

- $NBIS: signed a $17.4B AI-infrastructure supply deal with Microsoft. Given Nebius's 2Q25 revenue of ~$0.1B, a substantial positive. I liquidated the entire holding right after the announcement on volatility expansion / short-term-attractiveness decline; in hindsight holding would have been fine — a regret. But since the bet was a relatively trivial $6,570, selling was a reasonable decision on a hold-vs-efficiency basis.

[$NBIS]

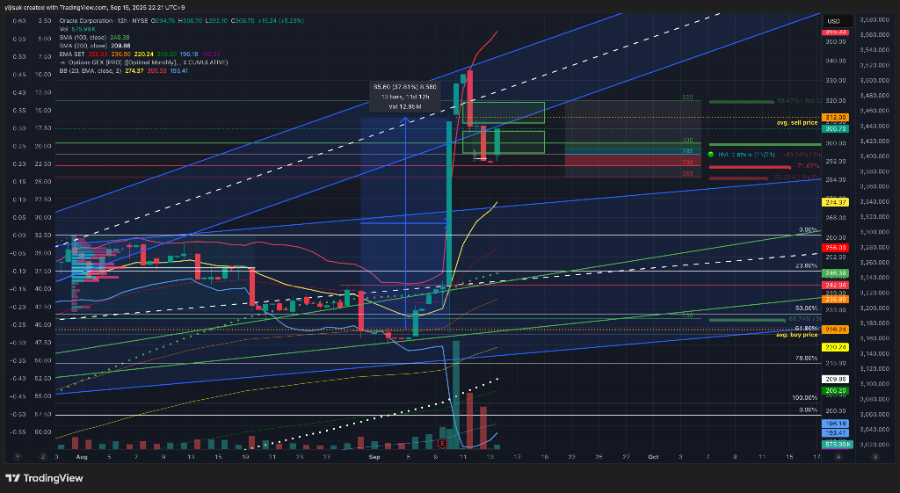

- $ORCL: after 3Q25 results, RPO of $455B, +359% YoY. RPO = future-revenue fuel, so ~30% average annual revenue growth over 5 years became feasible. Oracle DB has overwhelming on-premise dominance, integrated into OCI gen-2 infrastructure specialized for large AI workloads — forming Oracle's unique data-infrastructure leverage. Financial / medical data once on-premise-only is stored at substantial scale on Oracle servers worldwide, a great position for the data-based-AI build trend. Originally a medium-to-long-term hold; after the RPO-driven volatility I took first profit, then changed to doubling the holding after price stabilizes. Oracle should be viewed with a long horizon.

[$ORCL]

While raising trade frequency, the position range unintentionally widened and I made small mistakes. I entered Gold on a short horizon — judging September's high-volatility tape, often rooted in macro uncertainty, would pressure gold upward — and traded gold-related names adding leverage to momentum at the range-break. I selected names that, until a few months prior, were highly correlated with gold but had recently decoupled, betting on a "near-term correlation reversion." The direction missed, and per the "if it doesn't work, cut fast" principle from the start, I closed the trade decisively with a stop.

[$ORLA]

2. The Strange Balance of Employment and Inflation

(1) Employment

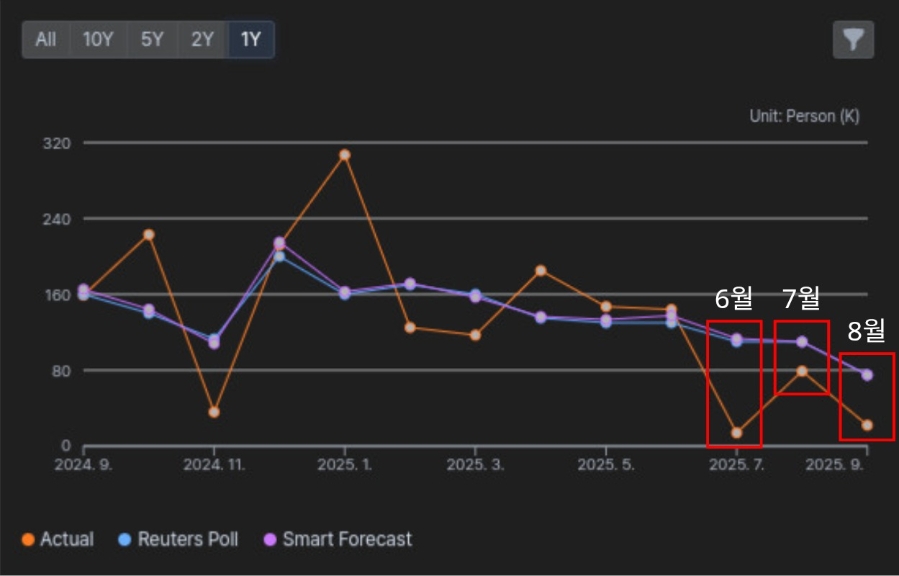

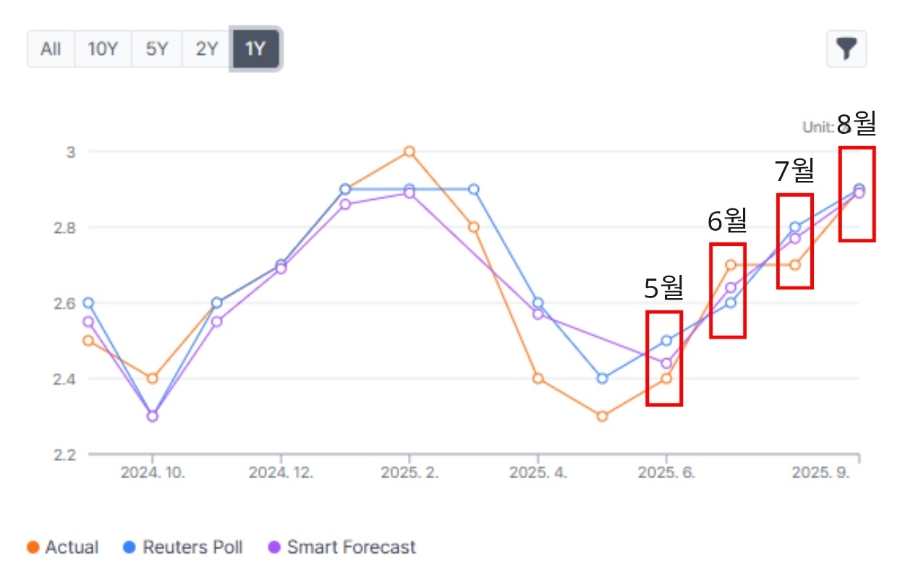

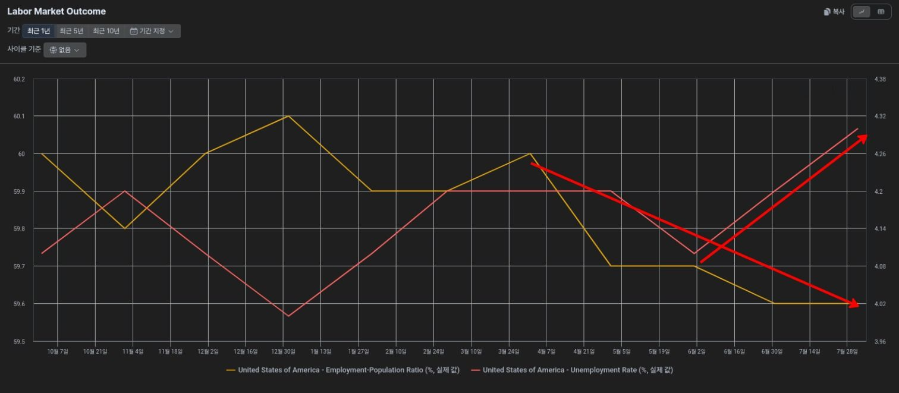

[BLS Nonfarm Payrolls actual vs estimate, 1Y trend]

BLS Nonfarm Payrolls, near estimates through Q2, had its narrative flip from the July report released in August. Key:

- Unemployment 4.2%, up slightly but in line with estimates.

- NFP +73K vs estimate +110K (miss).

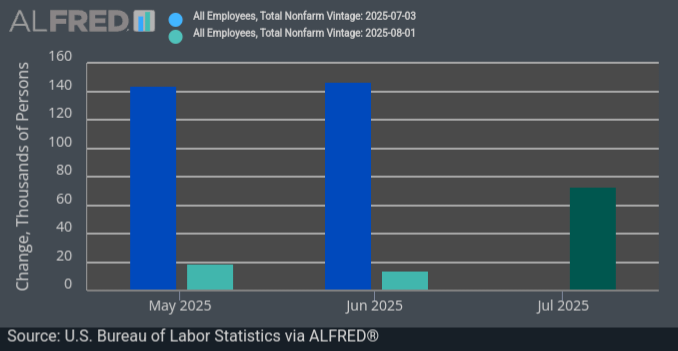

[May/June NFP print vs revision]

May/June NFP revised down by a combined 258K (May +144K→+19K, June +147K→+14K). July's gains were concentrated in cycle-insensitive sectors (healthcare +55K, social assistance +18K); cycle-sensitive private sectors (manufacturing, construction, transport, retail/wholesale, ICT, finance) were nearly flat or slightly down. Reading at the time: unemployment 4.2% nominally maintains full employment (<5%), but gains are concentrated, participation keeps falling while unemployment faces upward pressure. From the July report, the balance holds within a narrow range, signaling the Fed should weight labor-market downside risk more — a trigger that momentarily raised September-cut odds.

(2) Inflation

[May–Aug YoY PCE %]

[May–Aug YoY CPI %]

The May CPI/PCE released in June suggested a Q2 YoY downtrend reversal, but subsequent data began a clear uptrend; the market suspected corporate tariff pass-through to consumers showing up numerically. Inflation was under upward pressure, and until the Jackson Hole meeting (Aug 21–23) there was much speculation about which data the Fed would anchor on.

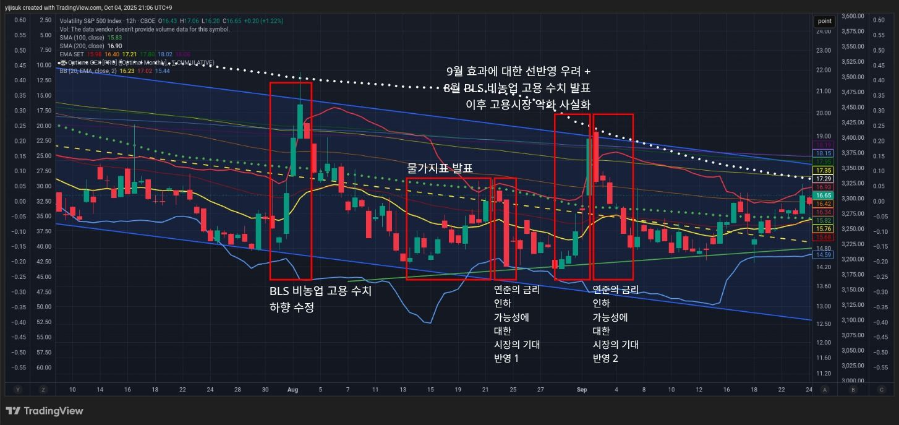

[August macro-view market volatility (VIX)]

(3) Jackson Hole — implications of Powell's speech

1) Jackson Hole

Unlike last year's clear "the time has come to adjust policy," this was a conditional "policy adjustment may be warranted." Asset markets cheered it as a cut signal, but the actual message is closer to continuing data-dependent, careful response amid the crossing of tariff-driven inflation pressure and labor-market downside. The crux is "data-dependent."

A. Policy-environment inflection — post-Trump-inauguration 2025: broad tariff hikes reshaping trade order; tighter immigration sharply slowing labor-supply growth. Long-run effects of tax/fiscal/regulatory change unsettled, with large uncertainty.

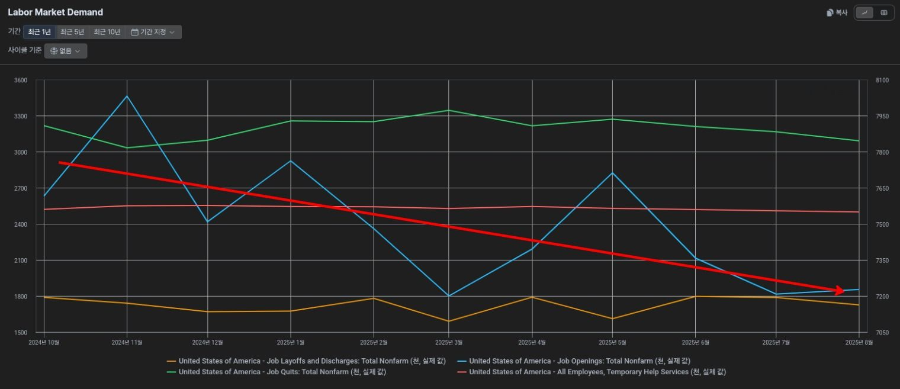

B. Labor market — a "strange balance" and growing downside. Per the July report, the recent 3-month job gains plunged to ~35K/mo, sharply revised down from a month prior. Yet unemployment held at 4.2%, near a historical low. Quits, layoffs, vacancy-to-unemployment, nominal wages little changed or mildly softening.

Demand side: Job Openings keep falling, Layoffs in a stable range, Quits slightly down, cycle/sentiment-sensitive Temporary Help Services little changed.

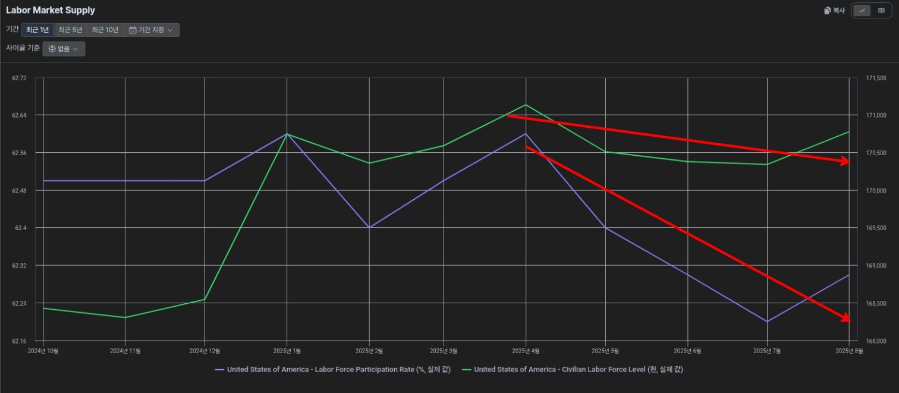

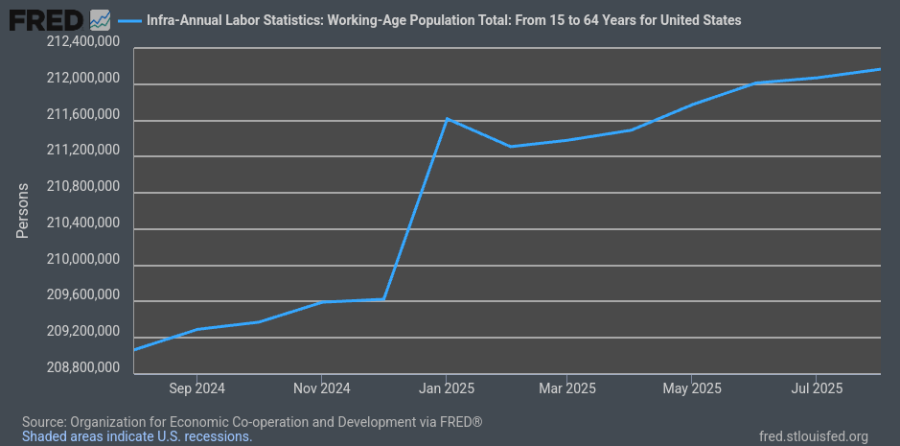

Supply side: Labor Force Participation Rate and Civilian Labor Force Level both falling (Participation Rate = Labor Force / Working-Age Population × 100 — the labor-supply pool is shrinking).

Conclusion metrics: Employment-Population Ratio falling vs Unemployment Rate rising. In EP Ratio = Employment / Population × 100, either (1) numerator Employment falls while denominator Population is flat/mild-up, or (2) Working-Age Population falls faster than Employment.

But since US Working-Age Population is growing somewhat, (2) is not tenable. Here the "strange balance" = demand and supply slowing together. Employment slowdown usually comes from weak demand, but now plunging immigration weakens labor supply simultaneously — the falling Participation Rate + falling EP Ratio prove labor-supply contraction + employment contraction. With labor-force growth far lower, the 'break-even' employment to hold unemployment dropped. Downside risk is rising, and if realized, "layoff surges and unemployment increases could unfold quickly" was stated explicitly (fortunately no layoff surge yet; needs more watching).

C. Inflation — tariff-hike price effects clear in some goods. Cumulative over coming months expected, but the policy-relevant key is whether it becomes persistent inflation. The Fed's base assumption: a "one-time increase in the price level." "One-time" does not mean instantly gone — it can feed through supply / distribution chains sequentially with a lag.

2) Monetary-policy framework revision

The Fed effectively wound down the core elements of the 2020 Flexible Average Inflation Targeting (FAIT).

A. ELB-premised wording cleaned up — the ELB (Effective Lower Bound) constraint is when the nominal policy rate nears a level hard to lower further, limiting traditional easing room. Long post-2008 ultra-low rates treated ELB risk as institutionally central, but in today's high-rate environment that assumption builds too narrow a frame. With cut room available, much discourse still anchors on "what if rates hit the ELB," neglecting new constraints — high-rate sustainability, rate-path uncertainty, bond-market burden, financing cost. The new statement says the strategy is designed to "promote maximum employment and price stability across a broad range of economic environments" — generally more flexible.

B. FAIT make-up strategy removed — the 2020 (AIT) statement allowed "above-target for a time if past inflation persistently ran below." Powell conceded "an intentional, moderate overshoot was neither needed nor realistic" — post-pandemic price surges left average-makeup unconvincing. The revision returns to Flexible Inflation Targeting, focusing on current comprehensive conditions rather than past inflation.

C. Employment-language adjustment — the 2020 "shortfalls" wording, premised on a hard-to-observe natural-rate estimate, intended not to rush tightening on transient overheating, but was read as "won't act pre-emptively." The revised wording is more balanced: "employment may temporarily exceed estimates and that alone is not immediately a risk; but pre-emptive action is possible if price-stability risk is clear."

3. The Imbalanced 'K-Shaped Economy'

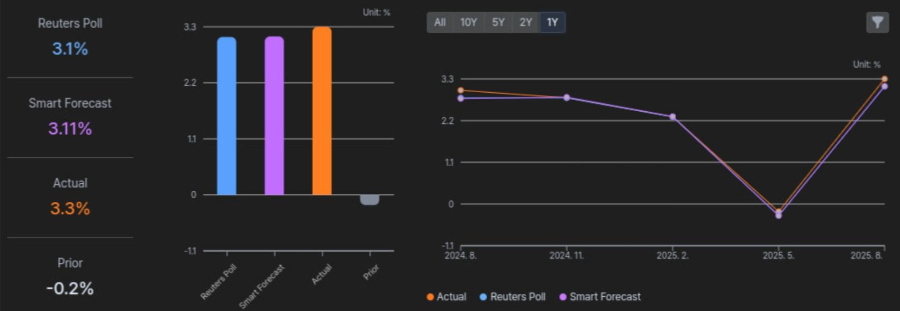

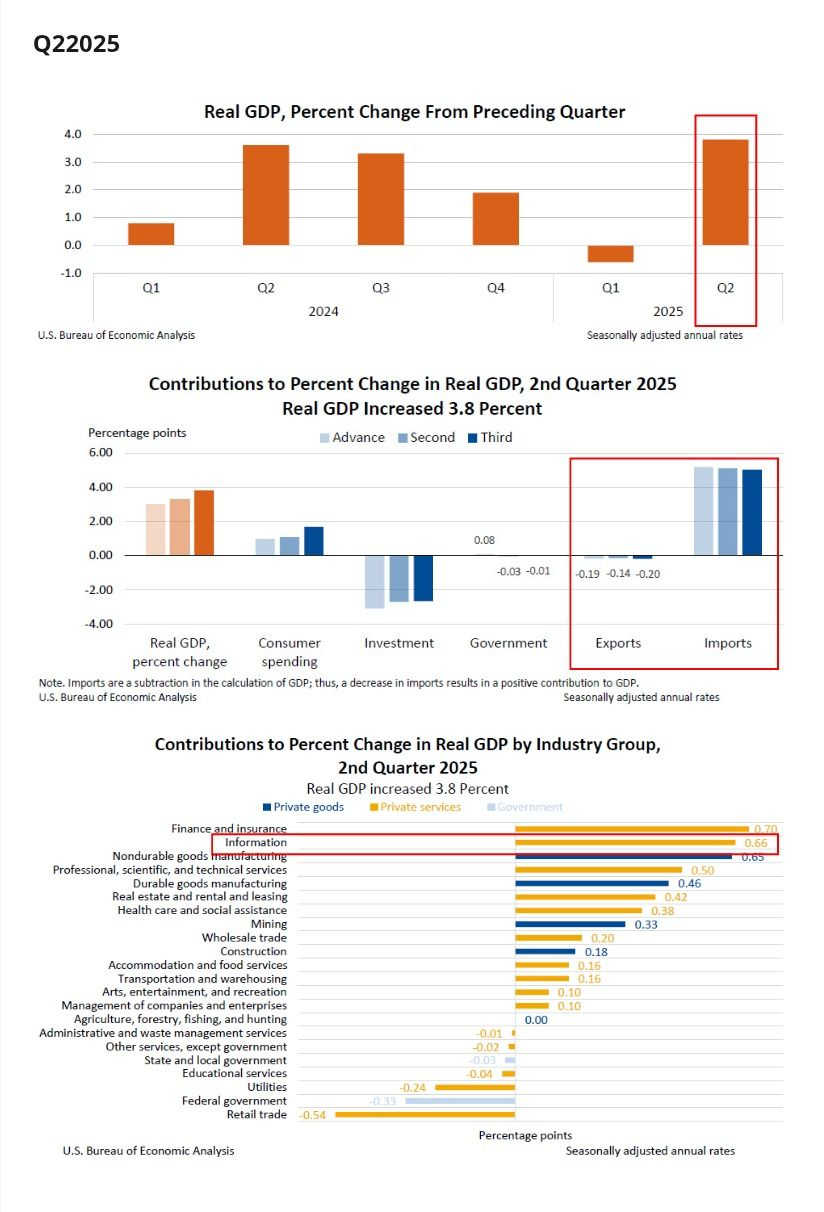

(1) US Q2 2025 GDP

[US annual GDP growth, 1Y]

Annual GDP growth, in a 4-quarter downtrend, rebounded to +3.3% YoY in Q2.

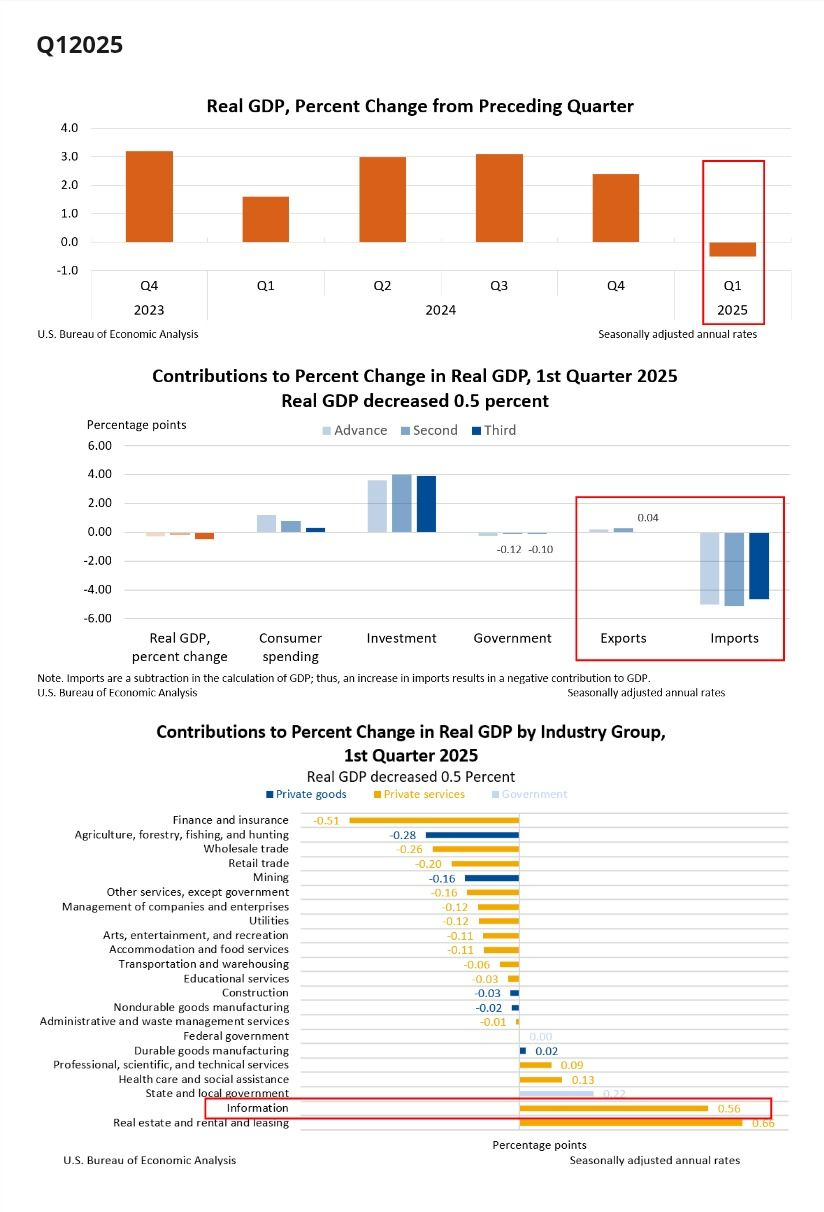

[Q1 2025 GDP growth factors]

[Q2 2025 GDP growth factors]

The Q1→Q2 upgrade was driven largely by the trade balance. Q1 imports were pulled forward ahead of tariffs, then fell sharply in Q2 — since GDP = C + G + I + (X − M), net exports improved markedly (possibly a transient effect of the import decline).

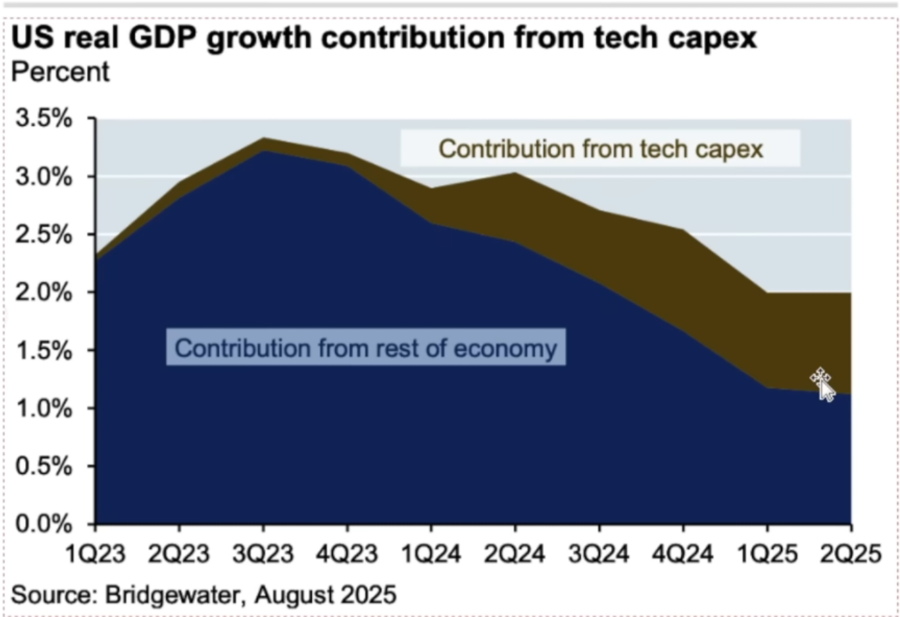

[Tech capex contribution vs the rest of economy, in US real GDP growth]

Another focus: in both quarters the Information sector is the key GDP-growth contributor.

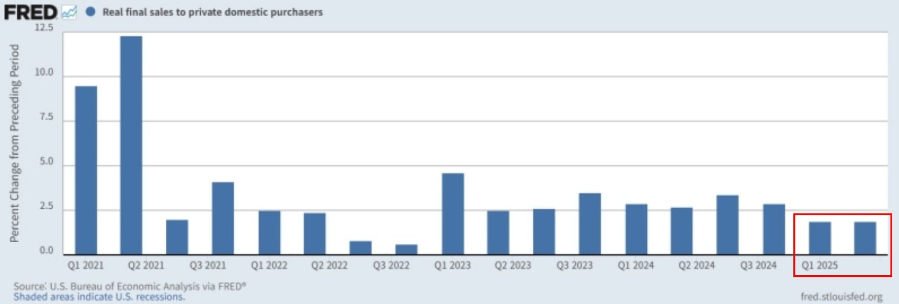

(2) US Domestic Demand and Non-AI Investment

[PDFP (private domestic final purchases) YoY growth]

The Q2 rebound is not a uniform recovery in domestic demand / investment. PDFP (Private Domestic Final Purchases), a good base read of US demand, stayed at the same 1.9% annualized as Q1 — a wide gap to the 3.3% headline.

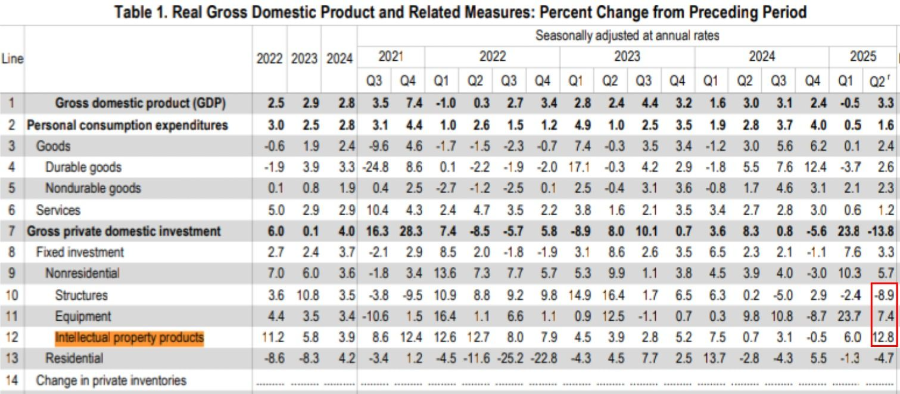

[US GDP growth factors]

In investment, the AI-related vs traditional gap is stark — IP products +12.8%, nonresidential equipment +7.4% lifted the top, while nonresidential structures −8.9% had the traditional real axis going backward. In a high-rate environment, capex is highly rate-sensitive (higher financing / opportunity cost → weak nonresidential structures). AI-related capex (data centers, GPUs, power infra) shows exceptionally strong momentum, masking other-sector weakness. Intangible / digital capital became the growth driver while traditional real sectors are pressed lower by rate sensitivity — this rebound was not balanced across sectors.

1) AI investment and the K-shaped structural gap

Ex-AI fixed investment is weak, structures / residential investment sluggish. A 'K-shaped' structure forms — up: AI/big-tech-centric large caps and high earners; down: traditional industry, SMEs, low earners with shrinking investment / consumption. In short: headline shows a firm recovery, but the structural base is still imbalanced. AI investment and transient factors lifted growth, but given the demand–non-AI-investment divergence and the rate environment, the growth path carries mild downward pressure.

4. The Sacrifice of Reserves, Through a Liquidity Lens

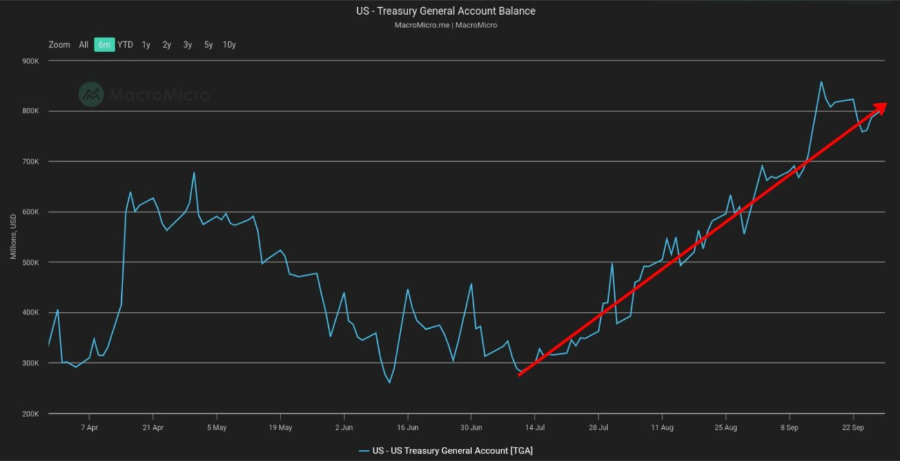

(1) TGA

[6-month TGA balance change]

With the TGA balance bottoming and rising from early July, I expected a somewhat early correction — but that was a one-sided TGA-only read. The TGA rose steadily through Q3, peaking at the $850B target on Sep 15. Yet it had little effect on the S&P 500 / NASDAQ 100.

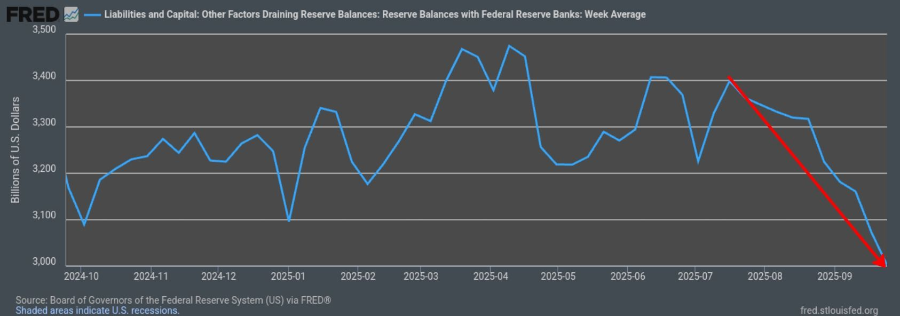

(2) Reserve Balances

[1-year Reserve Balances change]

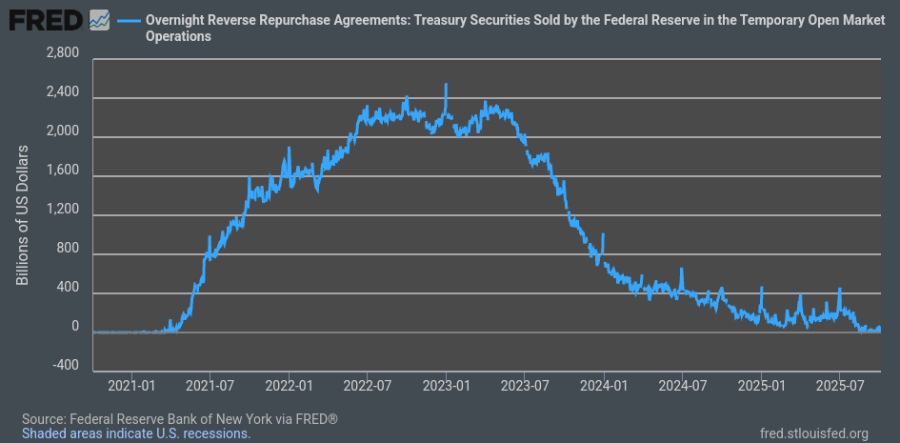

[ONRRP balance near zero]

Why? With ONRRP near zero, I expected the next TGA restore to pull liquidity directly from equity / bond markets — but reserves seem to have served as the supply source behind the TGA absorption. Ultimately the effective overlap of (a) strong earnings growth at key players, (b) rate-cut expectations from intensifying labor-market downside, (c) a low DXY, and (d) low oil made the TGA absorption's direct market impact relatively smaller than in the past.

5. Money-Market Liquidity Problems

(1) The level of rates

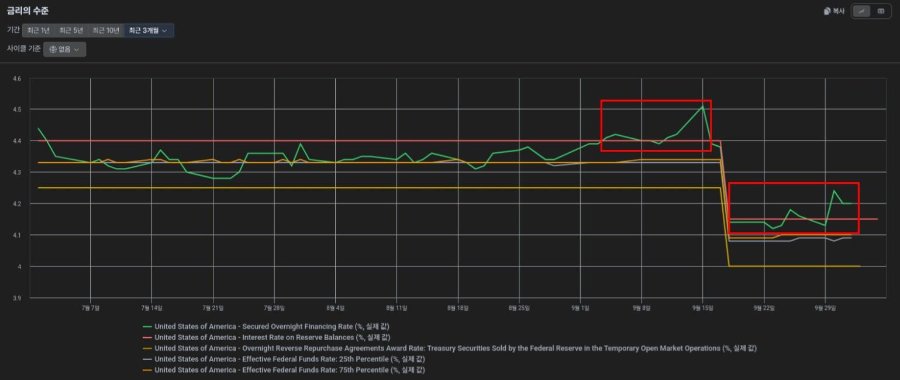

[Last 3 months of money-market rates. Green = SOFR, red = IORB]

Liquidity problems were not entirely absent. From late August to early September, the risk-free SOFR exceeded the banks' minimum return IORB several times. Normal-environment ordering: IORB 〉 EFFR 〉 SOFR 〉 ONRRP.

- IORB: only banks earn it via Fed deposits.

- Non-banks (GSEs like Fannie Mae / Freddie Mac / FHLB) can't earn IORB → earn the lower EFFR. EFFR is the most direct gauge of overall banking-system liquidity.

- EFFR (unsecured) 〉 SOFR (secured) — unsecured carries relatively higher default risk. SOFR is the broad secured-repo average rate, the representative gauge of short-dollar funding cost and system secured liquidity.

- MMFs / GSEs / some non-banks earn ONRRP via the Fed's reverse-repo — low barrier and ~0 default risk, so the very floor.

Normally SOFR forms below IORB (banks can lock IORB risk-free). SOFR 〉 IORB signals repo-market liquidity shortage — participants offering above the banks' attainable minimum reflects deepening cash-liquidity scarcity. SOFR stayed above IORB in early September, normalized briefly after the FOMC cut, then from Sep 24 again exceeded IORB and remains above.

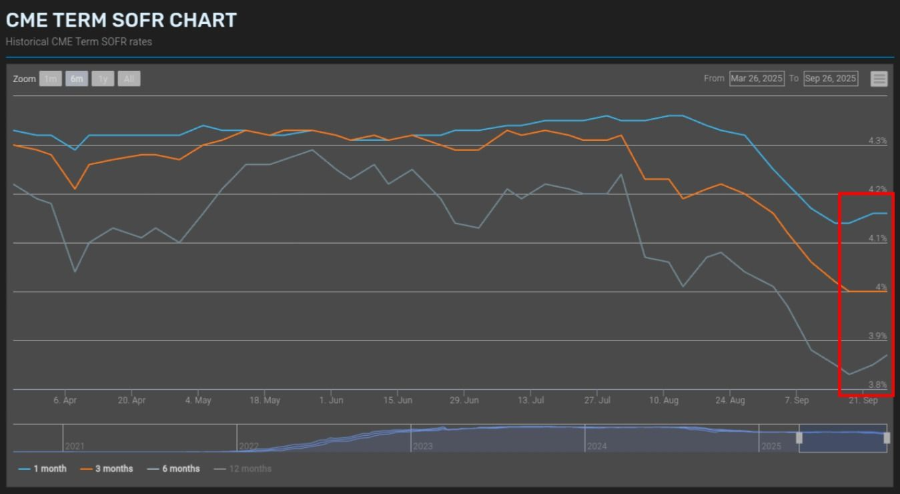

(2) CME Term SOFR

[1M / 3M / 6M SOFR futures]

SOFR futures bet on SOFR at expiry, so they converge to market expectations. In a sound environment the curve is downward, 6M 〉 3M 〉 1M (cut expectations embedded); the opposite is upward 1M 〈 3M 〈 6M (further-hike expectations). SOFR futures began turning up from Sep 18, but not yet a steep reversal — needs continued monitoring over time.

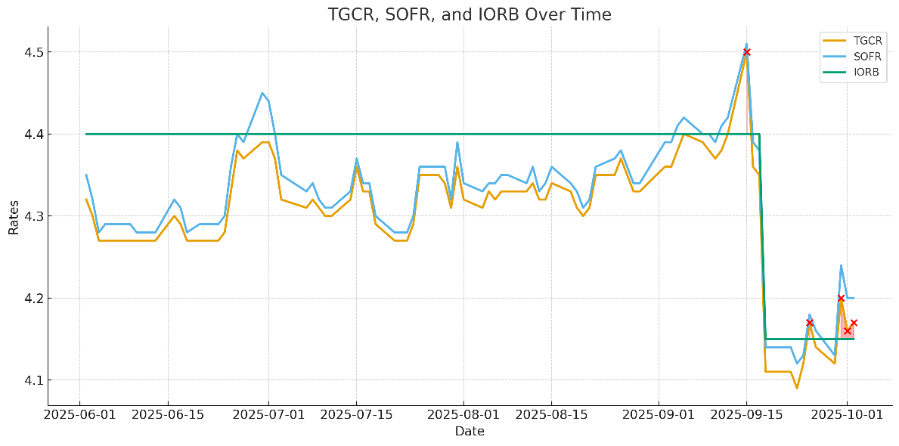

(3) TGCR (Tri-party General Collateral Rate)

[Last 3 months TGCR / SOFR / IORB]

Reflects tri-party repo between non-bank investors (MMFs/GSEs) and large dealers, sensitively showing a specific cohort's cash/collateral supply-demand. On Sep 25 Dallas Fed President Lorie Logan argued for modernizing the policy target EFFR to a repo rate. Post-2008 Ample Reserves + IORB fundamentally changed the FFM's character — it became an arbitrage market between IORB-ineligible institutions and eligible banks, a narrow market where just 11 FHLBs are the main lenders, so EFFR is a structurally invalidated gauge no longer representing system-wide funding cost. The proposed new benchmark is TGCR — FFM daily volume ~$100B vs repo over $4.5T. TGCR is the overnight rate on US-Treasury collateral in tri-party repo (mainly MMF cash investors–large dealers), covering $1T+ daily — describing repo liquidity faster and more sensitively. Usually below IORB; a prolonged TGCR 〉 IORB reflects dollar-funding pressure or surging Treasury-collateral demand (a tightening signal). The red x marks on the chart are where TGCR exceeded IORB — from late September after the cut, TGCR continuously exceeds IORB.

(4) Outlook

Overall: SOFR above IORB; EFFR volatility still small; SOFR futures starting to turn up; TGCR above IORB. SOFR and TGCR both above IORB = rising dollar-funding pressure in the secured money market and tightening cash/collateral supply-demand between non-bank investors and dealers. But limited EFFR volatility shows the banking system's internal unsecured liquidity is still stable. That is — banks relatively comfortable, but tightening signals materializing in non-bank / secured funding — the crux of the current short-term liquidity environment.

6. The US Government Shutdown

On Oct 1, 2025 (US Eastern), the federal budget deadline arrived but Congress failed to pass a new budget, halting federal-agency operations. The key: a government shutdown is entirely separate from the debt ceiling and does not mean a sovereign default. The debt ceiling was recently raised $5T, expected valid through H2 2027 — so the debt-ceiling issue is separate from the shutdown. A prolonged shutdown can affect the economy, but the impact is likely largely minor — during a shutdown the DoD, HHS, DHS, State, SSA etc. keep spending, ~85% of total government spending. My personal view: there may be a hidden Trump intent to induce an "unavoidable additional rate cut" by blocking key data like September NFP. The currently usable data is the Oct 1 ADP report — private payrolls −32K (low reliability, yet even it conveys strong labor-market downside).

7. The Persisting Internal Conflict — 'Uneasy Calm'

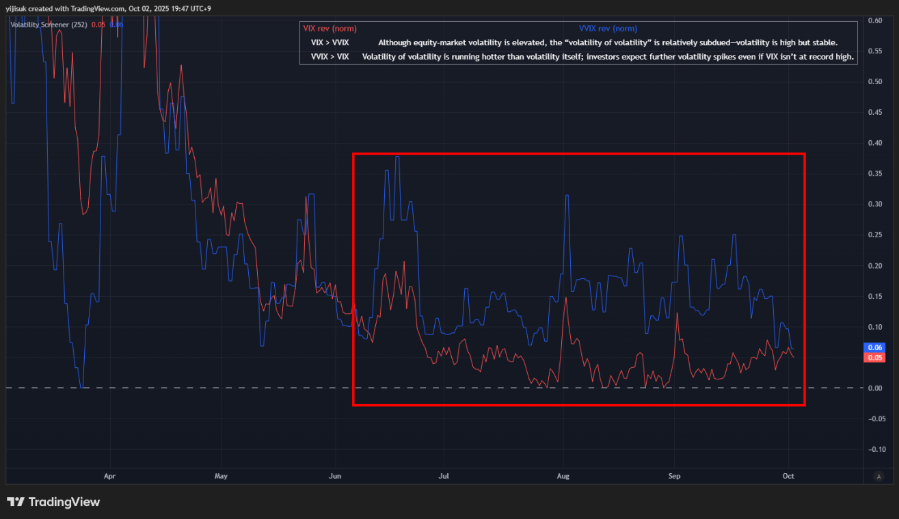

(1) VIX vs VVIX

[Inverted VIX (red) vs Inverted VVIX (blue)]

Through most Q3 sessions VIX sat in 2025's lowest zone, but VVIX kept above VIX. Even with volatility not at highs, participants are positioned for an eventual volatility spike — an 'uneasy calm' ran through Q3.

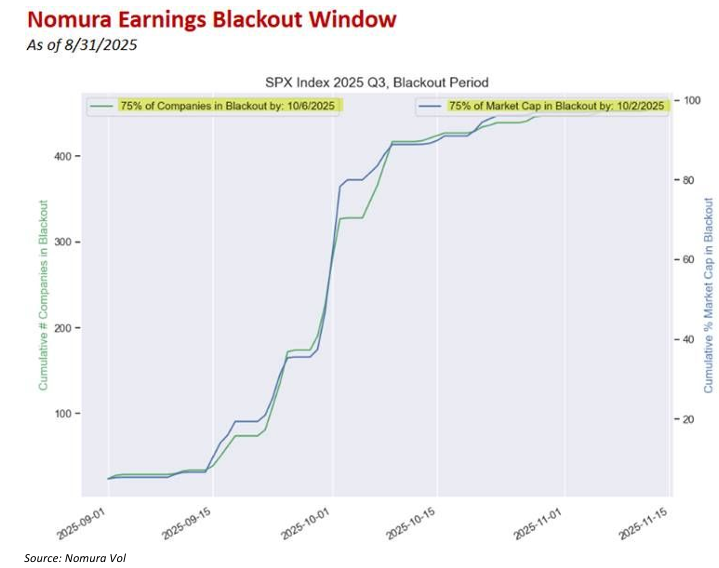

(2) Blackout through end-October

Into Sep–Oct, the Q3 earnings season approaches and buybacks are barred over insider-info concerns. By Oct 2, 75% by market cap; by Oct 6, 75% of S&P 500 by company count enter the blackout. With buybacks — a core support and volatility suppressant — gone, the market is likely more vulnerable to the liquidation risks noted earlier. By end-October ~90–95% of the S&P 500 should report; most see restrictions lifted 2–3 days post-report, so most resume from the week of Oct 20, with broad full resumption opening by end-October.

(3) Market leaders' positioning

[NAAIM Exposure Index]

The NAAIM Exposure Index measures the weekly average US-equity exposure reported by professional active managers in the NAAIM (0% to leveraged 200% long/short). Through Q3, especially the September rise, the index actually ranged sideways — institutions, hedging for possible risk, didn't put much into this rally. The Q3 advance was, broadly, retail-led. It is now sideways with a weak downtrend; if institutions begin raising weight in earnest, considerable upside remains. Perhaps it becomes Tom Lee's 'The Most Hated Rally' — I'll wait and see.

8. Reflections

(1) Widening the lens

I waited for a July–August correction watching only the rising TGA balance — a narrow lens. Conviction that "ONRRP is empty so liquidity will obviously be sourced from equities / bonds" + past-pattern fixation made me exclude the reserves possibility entirely. The deviation didn't make a big difference to trade performance, but served as a reminder to widen the lens.

(2) The three axes — liquidity, sentiment, momentum

The indicators most representatively monitored ultimately reduce to "liquidity." "Row while the tide is in" involves two stakeholders — (a) the one letting the water in, (b) the one rowing on time. Most participants are the latter. Liquidity flow is, broadly, a game of sentiment and momentum. Market sentiment is like an organism — (a) the most fundamental alive/dead metric is real-economy data, (b) persistence is monitored via short-term-funding-market rate levels, (c) the final outcome is read via end-node metrics like TGA and Reserve Balances. For momentum: in on-position mode, moderate beats overheated; in off-position mode, rather than FOMO-chasing overheated momentum unplanned, waiting for momentum to cool short-term in a sound-liquidity environment has higher risk-adjusted reward. I previously did quantitative momentum temperature-checking mainly from price, volume, and option-chain-derived data; for qualitative momentum, the highest-level tool is, I think, Google Trends.

(3) Free market → planned market

The US market is shifting from a free-market to a planned-market system — "planned" meaning direct government intervention under Trump. The so-called Trump signal-room cues should not be dismissed entirely as noise.

(4) Incentive → Intention-based liquidity

The Fed supplies liquidity, in principle independent of government, but its independence began to be infringed with the Trump era. For now Jerome Powell as a pillar props that independence, but after his term I think the liquidity source may shift from the free-market's incentive to the planned-market's intention. The ultimately money-making questions: (a) which industries lead this flow, (b) which directly benefit in the planned market — the contours of the answer are, I think, somewhat set.