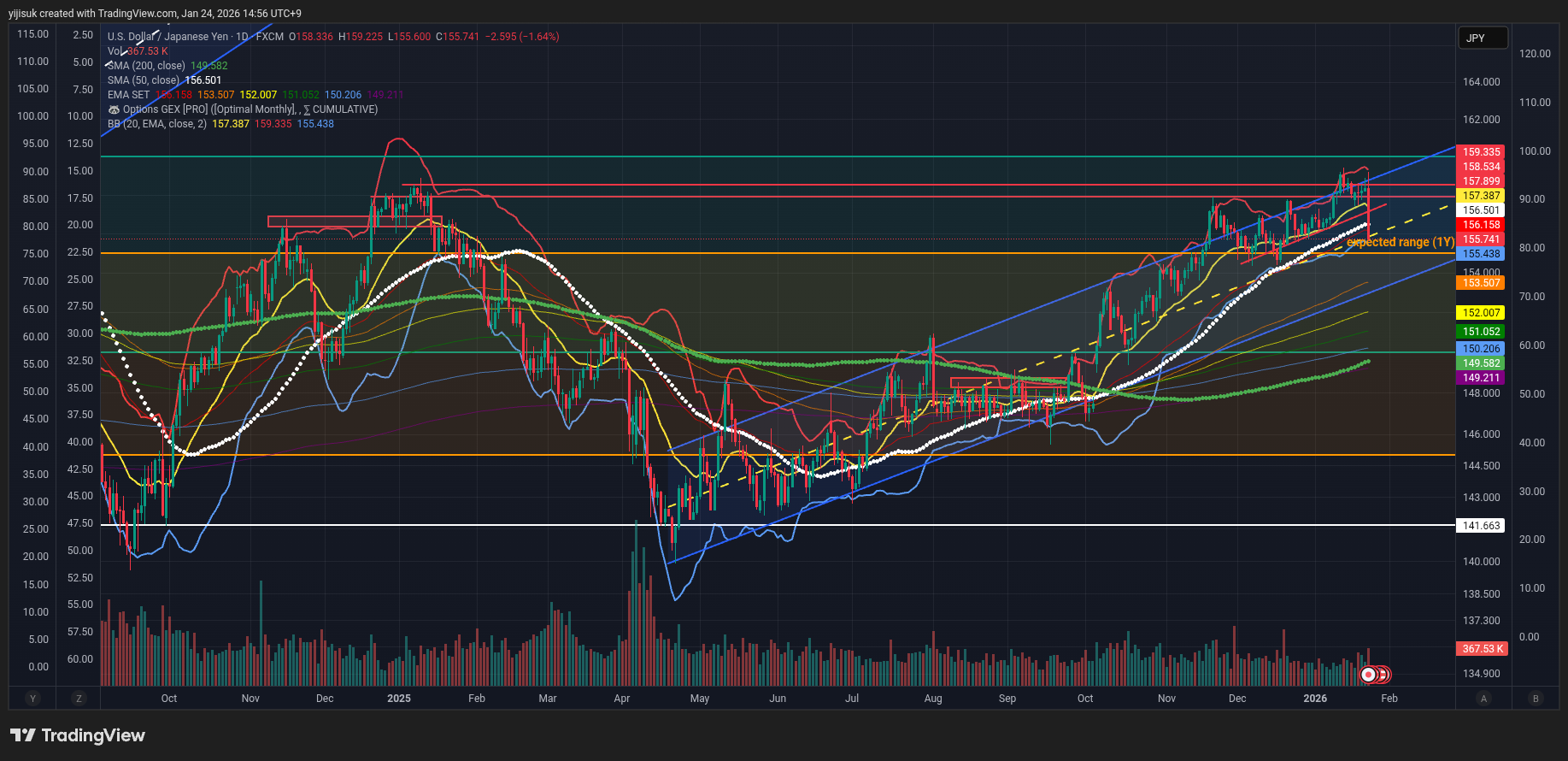

4Q25 Review Pt. 3 | A Short-to-Medium-Term Liquidity Scenario Centered on USDJPY

The point: the policy-rate-spread-centric USDJPY pricing mechanism may be sitting in a short-term distorted regime.

4Q25 Review

- Part 1⎯From Liquidity Fissures to Risk-Off

- Part 2⎯US Q3 GDP Review

- Part 3⎯A Short-to-Medium-Term Liquidity Scenario Centered on USDJPY

Since Sep 18, 2024, the Fed exited the high-rate regime and entered a cutting cycle. Through 2025 the US 10Y largely tracked the policy path with a lag, but from October 2025 it turned to a gentle upward shift, and lately the divergence from the policy rate (long rates breaking to the upside) has become pronounced.

The BOJ, after first exiting the 0% zone since July 2024, has since delivered two 25bp hikes and is mid-normalization. The JGB 10Y likewise shows a widening relative divergence from the policy rate through the hiking phase.

Meanwhile the US 10Y vs JGB 10Y policy-rate gap was on a downtrend throughout 2025.

In sum: Fed cutting, BOJ hiking — a narrowing policy-rate spread. Under the textbook mechanism, yen-carry unwinding pressure intensifies and a USDJPY decline (dollar weak, yen strong) is natural. Yet actual USDJPY runs counter to this, producing a gap versus the "normal path."

Two time-horizon lenses:

- A regime where a falling policy-rate spread cannot be reduced simply to USD weakness / JPY strength (short-term).

- The current weak yen is not grounded in fundamentals (medium-to-long term).

1. Why a Falling Policy-Rate Spread Doesn't Reduce Simply to USDJPY Weakness

In a narrowing US–Japan policy-rate-spread environment, a USDJPY decline via yen-carry unwinding is usually natural. If USDJPY nonetheless fails to reflect it, that signals not a broken correlation but a policy-rate-centric mechanism sitting in a short-term distorted regime.

(1) FX prices at least the following composite variables simultaneously

1) Compositional change in long rates (expected path vs term premium)

The 10Y is the sum of the expected policy path (expected short rates) and the term premium (compensation for duration risk). The US 10Y's break from the policy rate signals that long-rate-specific factors are strengthening — either (a) limited expectations of further cuts after the cut, or (b) a repricing of the long-end duration-risk premium.

2) Term-premium spread decline with FX non-co-movement

If the US–Japan 10Y policy-rate gap narrowed throughout 2025, that is usually a USDJPY downside factor. That USDJPY held up means the expected policy path, flows, and risk premia worked more strongly than the policy-rate spread. The priority by which rate-component changes feed into FX has likely shifted.

3) Japan's fiscal / political premium

When yen-weakness expectations build and fiscal expansion (more spending, tax cuts) is layered on, the market can demand an extra premium on long JGBs, reflecting both (a) rising bond supply and (b) doubts about long-run fiscal soundness. In that case a BOJ hike shows up first as higher long-end yields rather than restored currency credibility, and FX can keep weakening via a widening JPY risk premium.

4) Hedging cost / basis and position structure

JPY is strongly a carry funding currency, so volatility, margin constraints, and hedging costs often matter more than the policy-rate differential as liquidation triggers. So even as the spread narrows, absent a volatility event the unwind is delayed; conversely, when an event hits, a sharp yen appreciation (USDJPY plunge) can unfold nonlinearly.

(2) Implications

1) Japan side — rate rise ≠ currency strength, not reducible simply

If the current JP10Y rise is more a risk-premium character than a healthy result of policy normalization, the yen has room to react weak rather than strong. Then, even with short-term fiscal-stimulus benefits, the medium term can intensify (a) government interest-cost burden, (b) tighter financial conditions, and (c) the BOJ's policy dilemma (yen defense vs bond-market stability).

2) US side — Fed cut ≠ automatically lower long rates

The US, too, despite an easing environment, sits where the risk-premium character is strengthening. The essence of the gap is the cost-ing of the uncertainty / geopolitical premium.

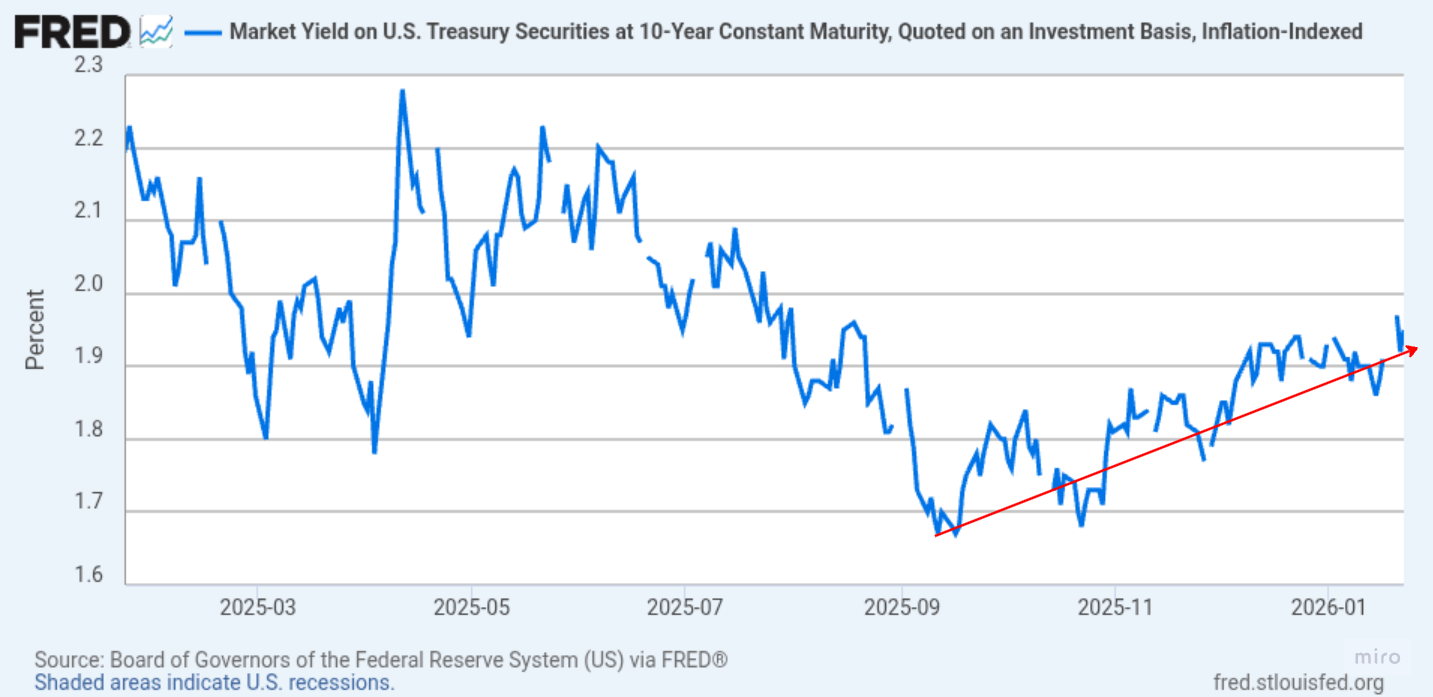

The US 10Y vs policy-rate gap turned to an increasing trend from October 2025.

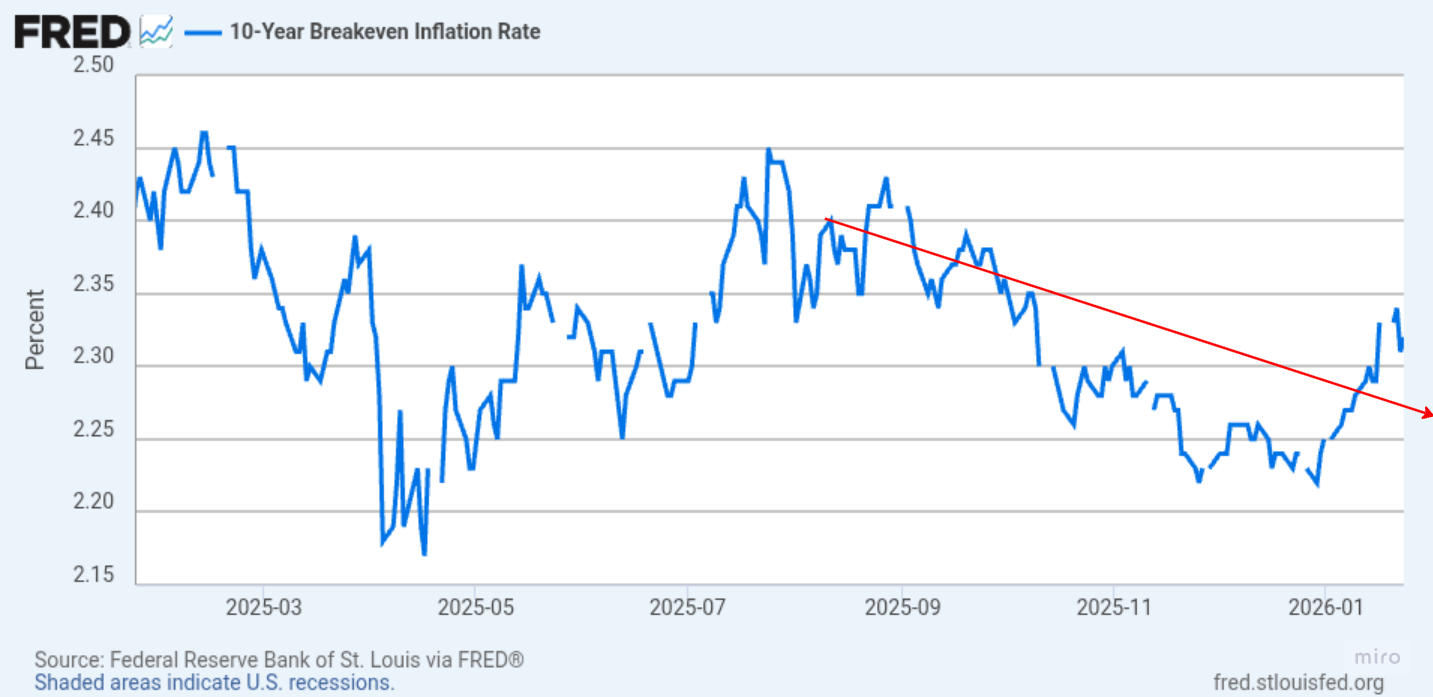

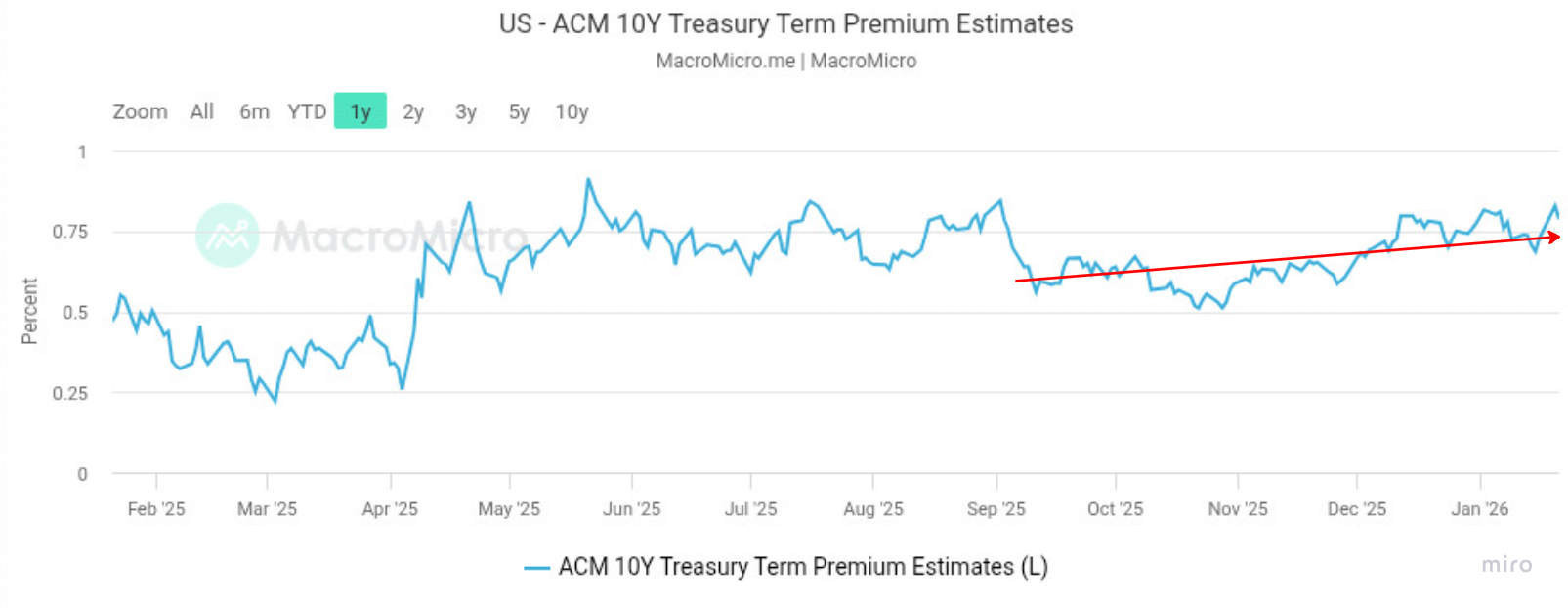

Nominal 10Y ≈ Real 10Y + Breakeven Inflation 10Y + Term Premium

Decomposing the US10Y rise by this identity:

Real 10Y: the inflation-adjusted (real) yield proxied by the 10Y TIPS yield. Turned to an uptrend from September 2025.

Breakeven Inflation 10Y: the market-implied average inflation over the next 10 years. Rebounded in January 2026 but, medium-term, on a downtrend since August 2025.

ACM 10Y Treasury Term Premium Estimates: the model-estimated term premium (compensation for duration risk) for holding long bonds. Also turned to an uptrend from September 2025.

In sum:

Nominal 10Y ⬆️ ≈ Real 10Y ⬆️ + Breakeven Inflation 10Y ⬇️ + Term Premium ⬆️

The nominal long-rate rise came from real + premium, not inflation expectations. So even with Fed cuts, the long-rate decline is limited, and the upside divergence from the policy rate may persist.

This premium does not show up only as higher long rates. It is also reflected in the sharp run-up in base commodity prices — gold, crude, gas, rare earths.

$GOLD

$XLE: breaking out of the 2-year downtrend channel since 2024 and forming an uptrend channel

$XOP

$OIH

3) FX market structure — tail risk matters more than a gentle trend

That USDJPY holds up despite the narrowing spread may mean the trigger is off while positions accumulate. Then the risk is larger on the side of a sharp unwind when volatility spikes / policy-tone shifts / liquidity squeezes combine — rather than a slow, steady term-premium decline. As geopolitical risk rises and liquidity rotates into gold, the dollar can send mixed signals. So USDJPY has more room to move nonlinearly via risk premia (Japan fiscal / political + global geopolitics) and position structure than via the cross-country rate differential.

2. The Current Weak Yen Is Not Grounded in Fundamentals

Medium-term, the correlation is more likely to be restored not in policy-rate form but through long-rate premia (term premium / uncertainty) or a volatility trigger, in a changed form. So the key question now is not "why hasn't it normalized yet" but whether normalization goes via (1) premium-based level justification or (2) trigger-based unwinding.

(1) The relative-yield structure follows the exchange rate

A simple reading says justifying the USDJPY level needs the policy-rate spread to re-widen. But that carries the excessive premise that the US real economy must improve markedly. As seen in the Q3 GDP review in Part 2, "K-shaped consumption divergence," "investment crowded into AI-centric capital-intensive sectors," and "net exports lifted by tariff-driven import declines" are far from a healthy real economy. If the real economy were improving, policy should be tighter, not easier — yet the market expects consecutive cuts plus QE, which contradicts the situation.

- Realistically, it is the long-premium-based relative yield, not the policy-rate spread, that can justify the USDJPY level.

- If US long rates stay high on term premium and uncertainty premium, the relative attractiveness of dollar assets can hold even through a Fed easing phase.

As a result, even with a "narrowing policy-rate spread," USDJPY downside can be limited or a high range sustained.

(2) The exchange rate follows relative fundamentals

The case where the narrowing spread is ultimately reflected in FX medium-term and USDJPY realigns lower. But because yen-carry unwinding occurs nonlinearly on a trigger event, the timing is generally set by a shock that breaks the position structure.

Representative triggers:

- A volatility spike (equity / credit) collapsing carry Sharpe.

- A sharp move in funding / hedging costs.

- A BOJ tone shift or stronger intervention — policy events.

- A growth shock or credit event.

One of the potential catalysts most worth watching is the combination of the AI narrative and leverage. If the market fails to confirm clearly (numerically) an ROI path that justifies AI capex into 2026, it can connect beyond a simple valuation repricing to a position-liquidation shock.