Q4 2025 US Treasury QRA Summary

The core of the Q4 2025 US Treasury QRA is the decision to freeze coupon (2Y+) issuance at the current level. This gave immediate relief to a market that had feared long-end supply pressure.

But the massive deficit-financing need persists, and the Treasury formalized a strategy of meeting it via expanded issuance of sub-1-year T-Bills. This lowers interest cost short-term but, as TBAC warned, is a trade-off that deliberately shortens the average maturity of the debt, accepting more frequent "refinancing risk" and "interest-cost volatility" going forward.

1. Borrowing Need and Funding Strategy

(1) Borrowing-need outlook

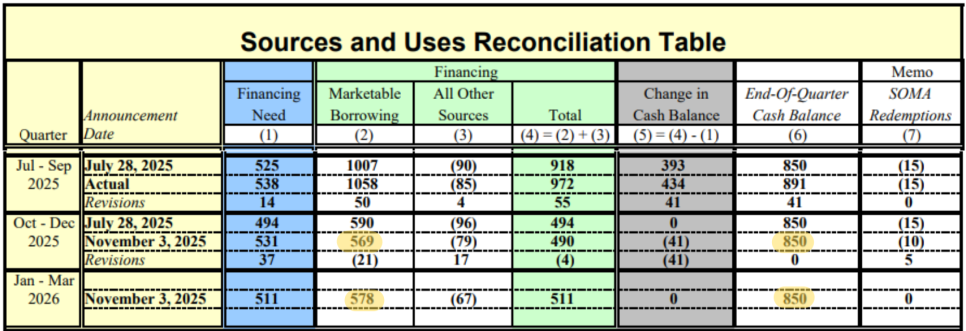

The Treasury projects total borrowing need of $1,147B over the next two quarters (FY26 H1):

- Oct–Dec '25 (FY26 Q1): $569B

- Jan–Mar '26 (FY26 Q2): $578B

- End-of-quarter TGA cash target: maintained at $850B

(2) Funding strategy

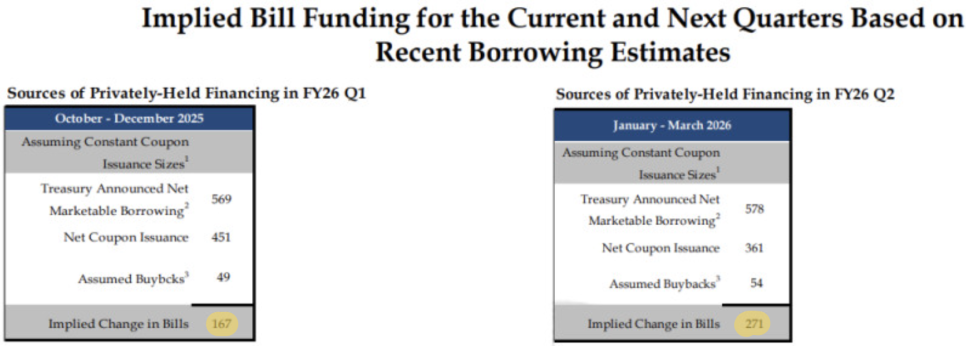

The Treasury confirmed a "Coupons Constant" strategy — freezing coupon issuance "for at least the next several quarters." The FY26 H1 need ($1,147B) is structured to fill the coupon-freeze shortfall with net T-Bill increases.

T-Bill net-supply outlook:

- FY26 Q1: $167B

- FY26 Q2: $271B

- Total ~$438B of net T-Bill supply to the market over FY26 H1 (six months).

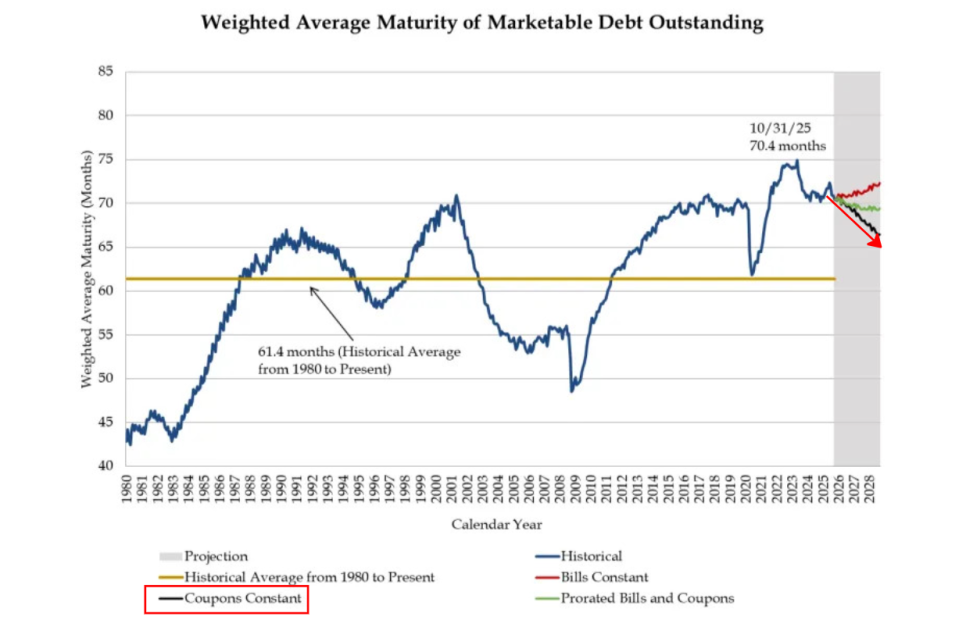

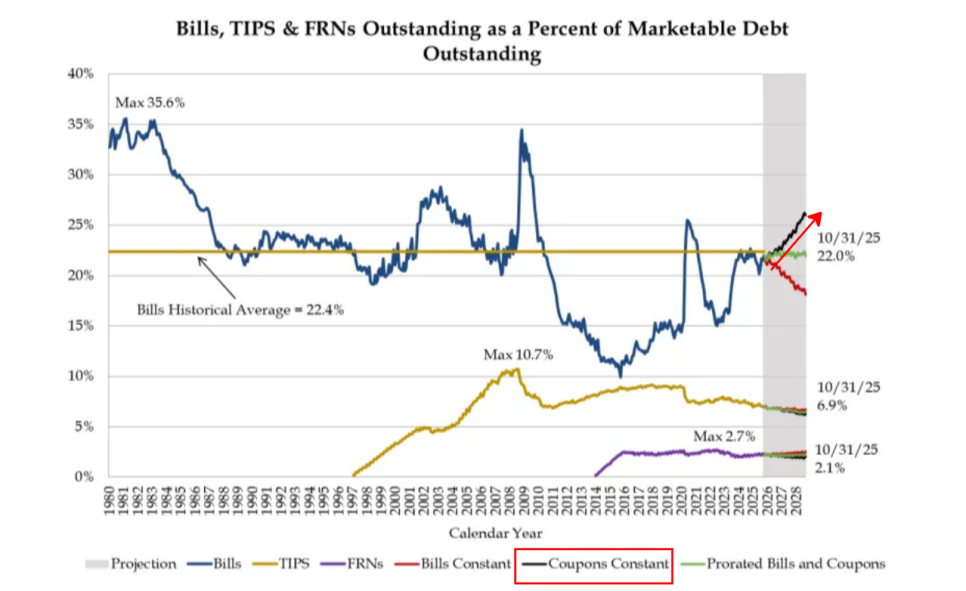

2. Implications of the Deliberate Maturity Shortening

(1) Deliberate shortening

"Coupons Constant" produces the following direct portfolio changes.

a. Falling weighted-average maturity (WAM) — with the coupon share stagnant and the bill share rising, the overall debt's average maturity shortens.

b. Rising short-debt share — both the T-Bill share of total marketable debt and the ratio of debt maturing within one year rise.

(2) TBAC's official warning — refinancing risk and volatility

TBAC, in its November 5 report, explicitly flagged the strategy's risks.

- Key point: "The Treasury's recent T-Bill-share expansion reduced expected cost but increased (interest-cost) volatility."

- Refinancing risk: raising $438B of new funds in bills in H1 alone, the government must now roll maturities over on a weeks-to-months cadence, dependent on market conditions.

- Interest-cost volatility: with future Fed policy shifts (hikes or cuts), government interest cost will swing far more sensitively and widely than before.

(3) Money-market impact

The TBAC report noted the T-Bill supply expansion is already affecting the market. With the RRP balance near a low level and T-Bill supply rising, some short rates (TGCR) printed an unstable 13bp above the Fed's IORB.

- IORB: interest paid on bank reserves at the Fed — the risk-free minimum yield for banks.

- TGCR: the overnight tri-party repo rate on US Treasuries as general collateral.

Through '24, ONRRP served as the demand sink absorbing T-Bill issuance, but its balance is now near zero. MMFs had pulled funds parked in RRP to lend to dealers or buy T-Bills directly. After the Trump administration's OBBBA passed in '25, T-Bill supply continued but no more liquidity could come out of RRP, so dealers had to source cash by offering higher rates — TGCR spiked. Normally a TGCR rise above IORB normalizes via bank arbitrage (pull reserves from the Fed to earn TGCR in repo), but a persistent, unstable overshoot indicates a reserve shortage in the banking system.

3. Sustainability and the Tone Shift

(1) The strategy's unsustainability

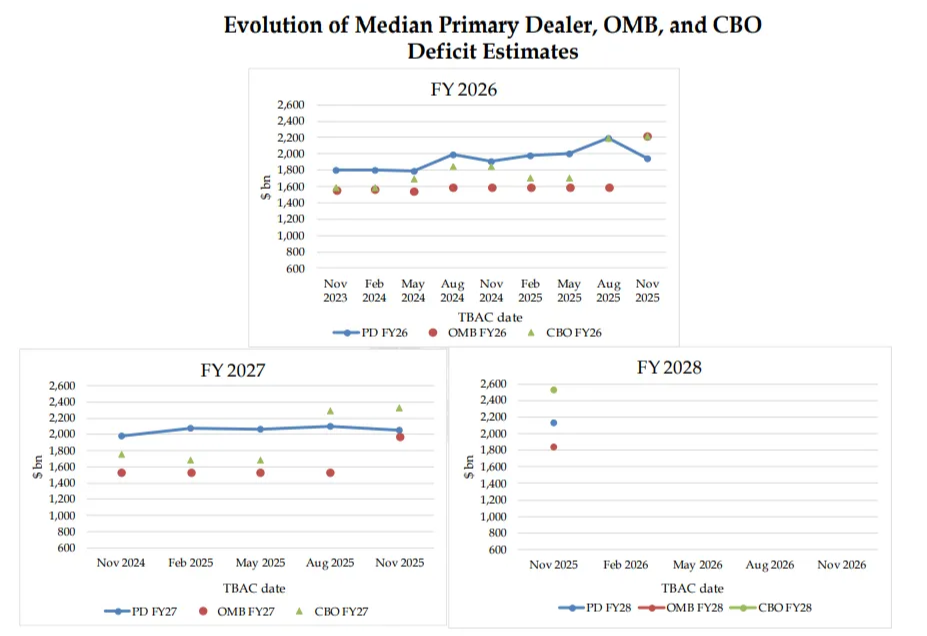

CBO (Congressional Budget Office), OMB (Office of Management and Budget) and others project massive deficits persisting at $2.1T–$2.5T annually into FY27–28.

Meeting $2T+ of annual need via T-Bill issuance alone is effectively impossible and could accumulate the refinancing risk TBAC flagged to an unmanageable level.

(2) The Treasury's tone shift and longer-term plan

The Treasury also recognizes this limit and signaled a subtle tone shift in this QRA statement.

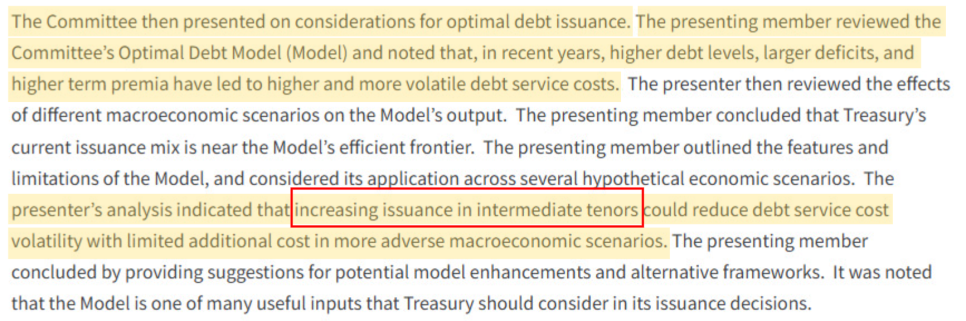

- A "preliminary review" formalized: while freezing coupons short-term, it officially stated it has "begun to preliminarily consider increasing issuance in intermediate tenors" in the future.

- Implication: the Treasury itself concedes the current bill-centric strategy is a stopgap and is preparing to raise coupon issuance again at a market-shock-minimizing point. Still, being at the "preliminary review" stage, the concrete timing of any increase remains uncertain.