Datacenter Power Supply Pt 1 | The Power Bottleneck and the Shift to BTM Fuel Cells

- Part 1 of 2 — "Datacenter Power Supply." This part covers the datacenter power-supply bottleneck and the shift to behind-the-meter (BTM) generation, and why fuel cells are drawing so much attention here.

- Part 2 covers Bloom Energy's advantages, its 800 VDC fit, the detailed financials and valuation, and the risks.

Executive Summary

The binding constraint on AI compute has migrated down the stack — from GPUs, to the grid, to manufactured generation capacity and permission. Capital is abundant; fast, firm, controllable megawatts are scarce. CoreWeave's CFO compressed the whole thesis into one line: "power today is more valuable than power in 2030" (Nitin Kumar, CFO, CoreWeave — Jefferies Software, Internet & AI Conference, 2026).

That inversion — "capital is abundant, permission is scarce" — drags the industry behind the meter (BTM) and, within BTM, up a technology ladder: gas turbines → reciprocating engines → solid-oxide fuel cells (SOFC). Each rung trades efficiency and $/MWh for speed-to-power and permission.

Bloom Energy sits at the top of that ladder for one structural and one cyclical reason:

- Structural (the 800 VDC shift): The datacenter power architecture is moving to native 800 VDC, mandated at the Rubin-Ultra Kyber rack (600 kW+, shipping 2H '27). Bloom's SOFC is the only commercially shipping source that outputs 800 VDC natively, skipping the lossy AC→DC conversion that every turbine/grid + rectifier stack needs — and dodging the transformer/switchgear/rectifier supply bottleneck that is itself now a multi-quarter queue.

- Cyclical (the turbine bottleneck): The gas-turbine oligopoly (GE Vernova, Siemens Energy, Mitsubishi) is sold out into 2029, with only ~10 GW of 2029–2030 slots left at GE Vernova; the OEMs refuse to over-build factories after the 1990s–2000s and 2018 boom-bust cycles. Turbine pricing is up ~20% to ~$3,000/kW. Customers "searching elsewhere" hit reciprocating engines (also backlogged into 2028) and land on fuel cells as the fastest path to first power — Bloom ~90 days, 55 days proven at Oracle.

The numbers have inflected hard:

- revenue $1.47B (2024) → $2.02B (2025) → consensus ~$3.68B (2026E, +82%) → ~$6.44B (2027E, +75%);

- Q1 '26 was the first clean GAAP-profitable quarter (+$70.7M net income, +$0.23 EPS);

- product backlog $6B (+140% YoY) atop ~$14B service backlog;

- an Oracle master agreement for up to 2.8 GW (1.2 GW contracted ≈ $4B).

The bear case is equally concrete — and already in the price:

- forward P/E ~134× on FY '26E, compressing to ~58× on FY '27E as earnings ramp;

- a PEG of ~1.0 (+1Y) that depends entirely on a >600% / +134% two-year EPS trajectory being delivered.

Add real risks:

- SOFC competition (Ceres Power licensees Weichai/Doosan/Delta; FuelCell Energy (NASDAQ: FCEL); GE Vernova's (NYSE: GEV) metal-based cell by 2027),

- Scandium / rare-earth + 50% metals tariffs,

- an unproven 2-year stack-life extension,

- and the open question of whether facility-edge conversion vendors (Vertiv, Eaton, Schneider, ABB) capture most of the 800 VDC value regardless of generation source.

Bottom line: the technical and commercial chain holds. The investment question is: (1) how much flawless, multi-year execution is already discounted — and (2) whether Bloom's moat survives the SOFC competition arriving in 2027–2029.

0. The Framing — A Regime Shift in What "Good Power" Means

A change in the attractiveness function for power solutions sits underneath everything:

- Old regime: solutions needing low capital, high permission win → grid power. Cheap per-MW, gated by multi-year interconnection queues, utility planning, permitting, community pushback.

- New regime: solutions needing high capital, low permission win → BTM gas, then fuel cells. More expensive per-MW, more operating complexity, but the developer owns the timeline.

Two forces flipped it:

- AI compute demand went parabolic, and datacenters became a political and environmental flashpoint, so permission (interconnection, air permits, community acceptance) became the binding constraint, not money.

- Capital for power remains abundant despite application-ROI scrutiny. Hyperscalers self-fund power buildout from massive cash flows, and a powered site retains option value even if a given AI product disappoints — so power-infrastructure capital keeps flowing even as application-layer AI ROI gets questioned.

Ratings agencies have institutionalized the shift: secured power is now treated as a fundamental differentiator of datacenter project risk.

1. The Available Power-Supply Solutions (the Supply Stack)

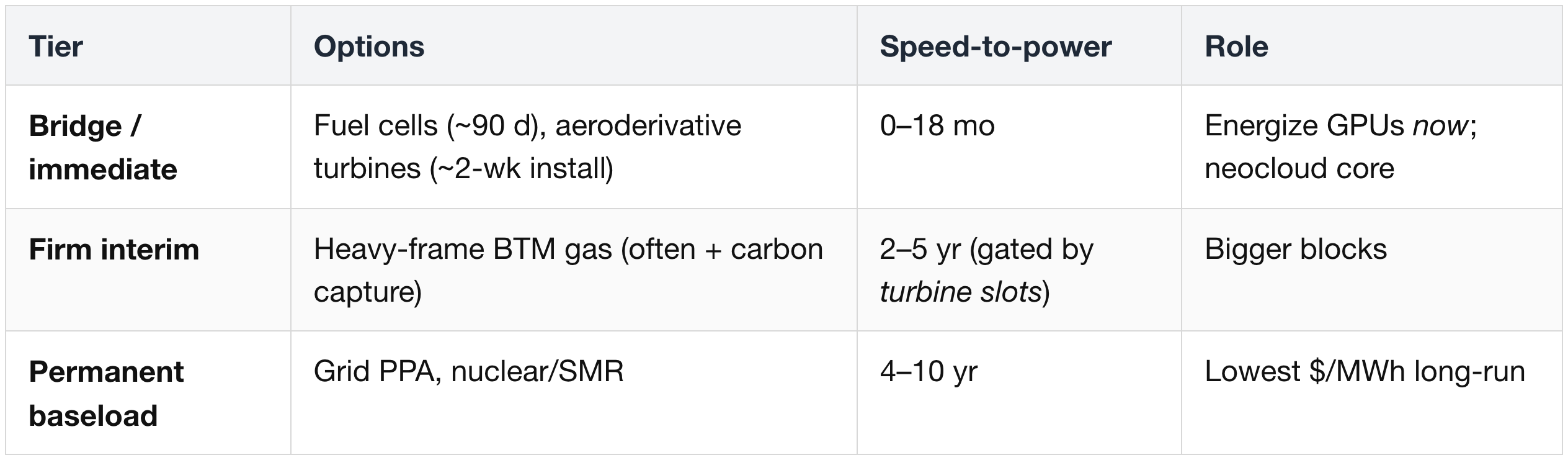

Datacenter power in 2026 is a three-tier stack sorted by speed-to-power — because speed is the competitive variable.

1.1 Grid power — the default that broke

- Mechanism: utility PPA (Power Purchase Agreement) + transmission interconnection. Lowest $/MWh; ESG-clean if renewable-backed.

- Why it broke — interconnection queues by ISO: PJM ~7 yr · ERCOT ~5 yr · MISO ~4 yr · CAISO ~3 yr. US datacenter power demand is projected to double from 31 GW (2025) → 66 GW (2027), lifting datacenters from 4.1% → 8.5% of US peak summer demand.

- The grid is now actively pushing back: PJM's Connect & Manage (effective June 1, 2027) requires new large loads to bring their own capacity or face curtailment (~50–100 hrs/yr) — effectively forcing datacenters into BTM procurement.

- Net: roughly one-third of planned new datacenter capacity is being designed to run independently of the grid.

1.2 Behind-the-meter (BTM) generation — three sub-options

On-site generation spans a spectrum:

- from low-CapEx, but high-OpEx, fast-to-deploy engines for bridge power

- to high-CapEx, but low-OpEx plants for permanent baseload.

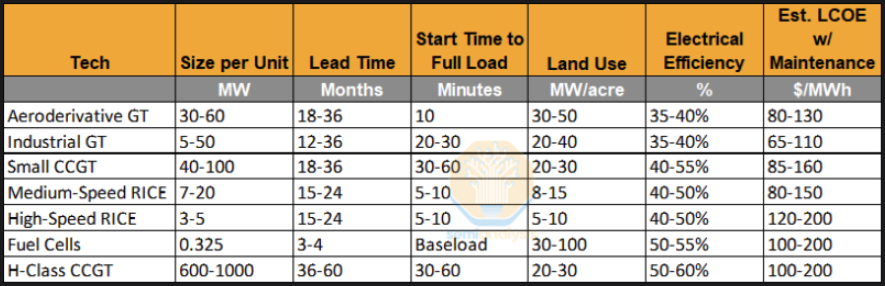

The options compare head-to-head like this:

- Lead time is the decisive variable.

- Fuel cells install in 3–4 months — against 12–36 months for gas turbines, 15–24 for reciprocating engines, and 36–60 for an H-class CCGT.

- In a market gated by time-to-power, that gap alone reorders the ladder.

- The CapEx/OpEx trade sets the use case.

- Engines and aero-turbines win on upfront $/kW and speed → optimal for short, uncertain tenures (functioning as bridge power source during power cuts on peaks; lifespan of < 5-7 years).

- Fuel cells and H-class CCGT carry higher CapEx but higher efficiency (50–60% vs 35–45%) and lower lifetime $/MWh → steady 10–20-year baseload.

- The heuristic: "lowest upfront cost & fastest deployment" vs "lowest lifetime LCOE."

- Fuel cells are also the most power-dense, with the lowest local pollutants.

- 30–100 MW/acre, pure baseload, no combustion — so NOx/SOx run >90% below turbines, though they still emit CO₂ (≈735–849 lbs/MWh, only ~25% less than a CCGT).

- That means a lighter air-permitting path — still permitted in most states, but as a streamlined "minor source" (CARB-exempt in California; ~45-day general (minor-source) permit in Ohio) rather than the 1+ year battles turbines face.

(a) Gas turbines — the incumbent BTM answer, two flavors:

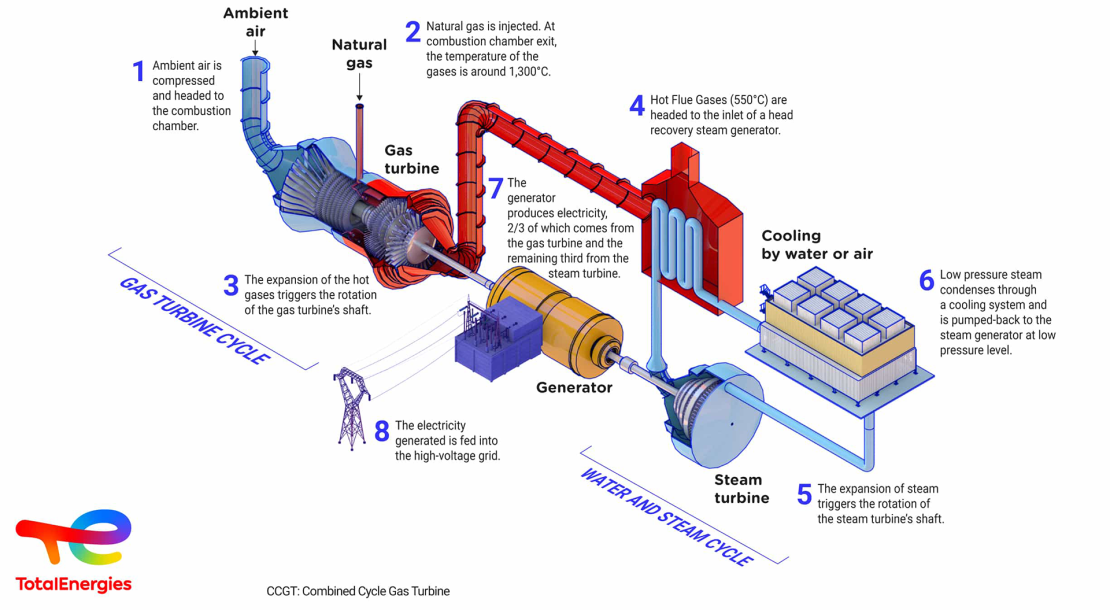

- Combined-cycle (CCGT): gas turbine + a steam cycle recovering exhaust heat. Maximum energy from the gas, highest efficiency relative to gas turbines, but most complex and longest to build. Best fit: permanent baseload.

- Aeroderivative: "a jet engine strapped to the ground" — faster-start, modular (GE Vernova (NYSE: GEV), Mitsubishi Power (MHI, TYO: 7011), Siemens Energy (ETR: ENR)). The LM2500XPRESS installs in ~2 weeks. Simple-cycle efficiency ~30–45%.

- The constraint = pollution + permission + supply. All gas turbines emit NOx and SOx; every deployment faces slow air-permitting and lawsuit exposure (e.g., the xAI Colossus / Southaven Clean Air Act suit over ~33 unpermitted turbines). And the OEMs are sold out.

(b) Reciprocating engines — the first landing of "searching elsewhere": cheaper, dirtier, less marvelous. Lower $/kW than aeroderivatives ($700–1,200/kW) but high maintenance, smaller units, ~40% efficiency. Makers: Caterpillar (NYSE: CAT), Cummins (NYSE: CMI), Wärtsilä, INNIO. Now also backlogged (Caterpillar booked into 2028).

(c) Fuel cells (SOFC) — the top of the ladder; Bloom Energy. Higher CapEx but native DC output, fastest deployment, and no combustion — near-zero NOx/SOx and a lighter permitting path, though they still emit CO₂ (~25% less than a CCGT, not zero). The terminal "search elsewhere" destination.

1.3 The permanent-baseload leg (long-dated): nuclear / SMR

Not BTM and not fast, but the hyperscaler balance-sheet leg:

- Microsoft–Constellation (Three Mile Island restart, ~835 MW),

- Amazon–Talen (1.92 GW) + X-energy SMRs,

- Google–Kairos (500 MW),

- Meta–TerraPower/Oklo,

- Oracle's 3-SMR campus. Online 2027–2035+.

Long-run $/MWh as low as $30–40 but pre-FID with 2030+ timelines.

The stack, summarized:

2. How Online Datacenters Are Actually Powered Today (Hyperscalers & Neoclouds)

There is no single approach — the picture splits by balance sheet and urgency.

- What follows emphasizes how live capacity is powered now, with contracted/committed power (and the named supplier) alongside.

- Real power portfolios blend grid, gas, fuel cells, nuclear, and storage. Publicly available information have been aggregated; not individual, detailed components.

2.1 Hyperscalers — barbell: fast on-site gas for live load + long-dated firm (nuclear/grid) for the future

The hyperscaler playbook is to grab whatever energizes a campus now — grid where it's available, on-site gas where it isn't — and backfill clean baseload later with nuclear PPA (Power Purchase Agreement)s.

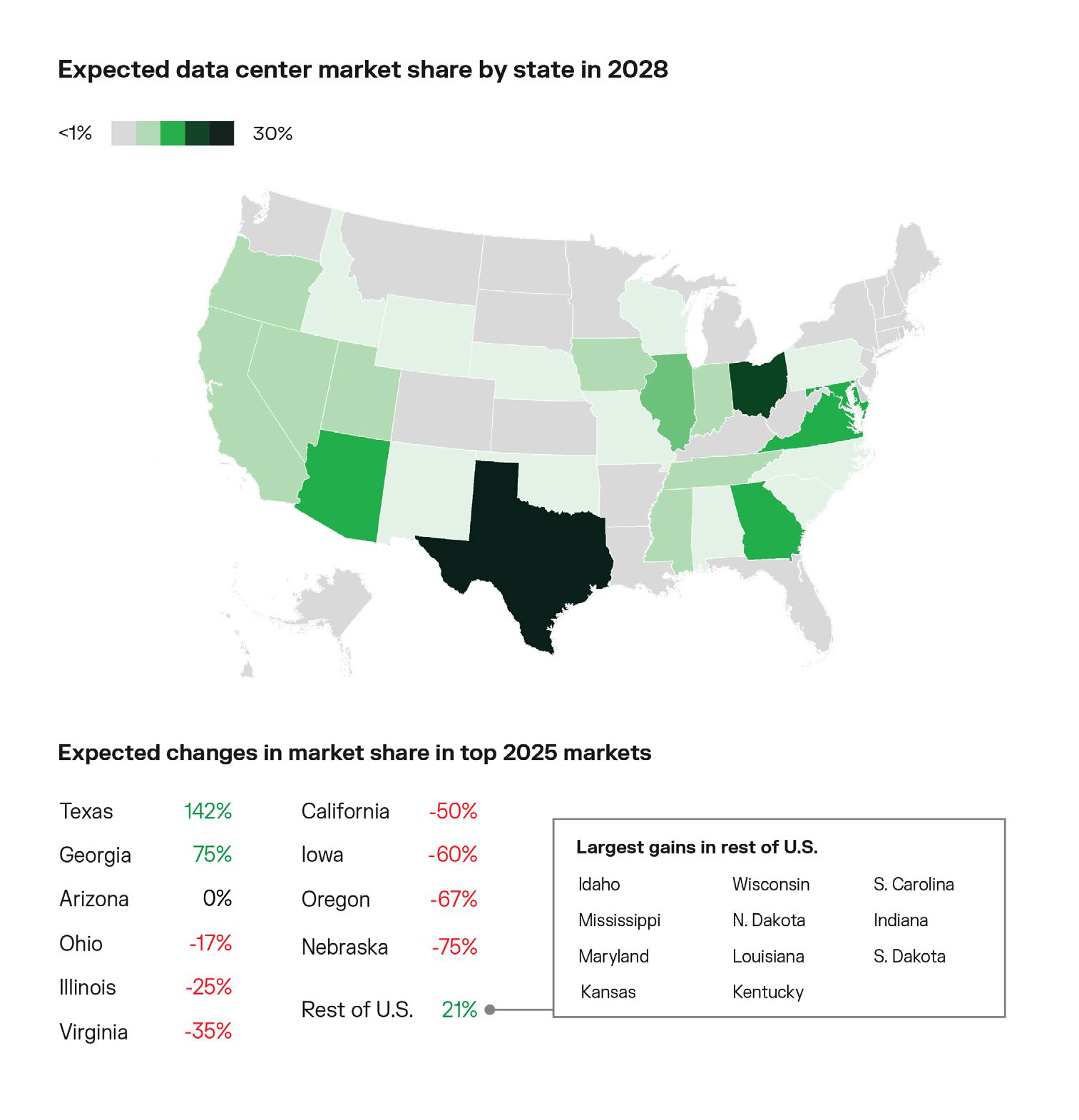

And the map is moving to where power is cheap and fast to permit: expected datacenter market share is surging in Texas (+142%) and Georgia (+75%) while shrinking in California (−50%), Oregon (−67%) and Nebraska (−75%) — the same low-cost, fast-permit states Bloom's backlog has flipped toward (Bloom Energy internal survey — though take this with a grain of salt, as the developer survey was conducted by Bloom Energy itself).

Microsoft (NASDAQ: MSFT)

- Microsoft's growth is now capped by power availability, not customer demand — it adds roughly 1 GW of capacity per quarter, but only as fast as it can energize the sites.

- Its default has been grid power, but it is now pivoting toward building on-site natural gas where the grid can't deliver in time.

- For long-term clean baseload, it has contracted the Three Mile Island nuclear restart — 835 MW from Constellation (>$100/MWh), coming online in 2027–28.

Meta (NASDAQ: META)

- Meta is the most aggressive hyperscaler at building its own on-site gas plants to power live load.

- On top of that, it layers long-dated nuclear contracts for clean baseload: Vistra (~2.1 GW), Oklo (1.2 GW), and TerraPower (690 MW now, scaling to 2.1 GW by 2035).

Amazon (NASDAQ: AMZN)

- Amazon ran the largest build-out of 2025, adding about 3.9 GW — more than any other operator.

- Its live capacity is almost entirely grid-fed today;

- its nuclear deals are firm power contracted for the future, not yet powering AI load:

- Susquehanna (1.92 GW co-located at Talen's existing, operating plant — Amazon's draw is ramping, ~$83/MWh),

- Somervell County (Vistra's Comanche Peak plant, with Amazon's data center slated to start construction ~2027),

- X-energy small modular reactors (~5 GW, reactors still in development for ~2030s).

Alphabet / Google (NASDAQ: GOOGL)

- It is now making its first move into behind-the-meter gas, at the off-grid Goodnight campus.

- For firm clean power it has contracted Kairos small modular reactors (500 MW, 2030+) and Ormat geothermal (~150 MW in Nevada, 2028–30).

Plus smaller Texas campuses (Red Oak ~93, Midlothian ~82 MW) and early-build sites (Fort Wayne, Cedar Rapids, Kansas City East) not yet energized.

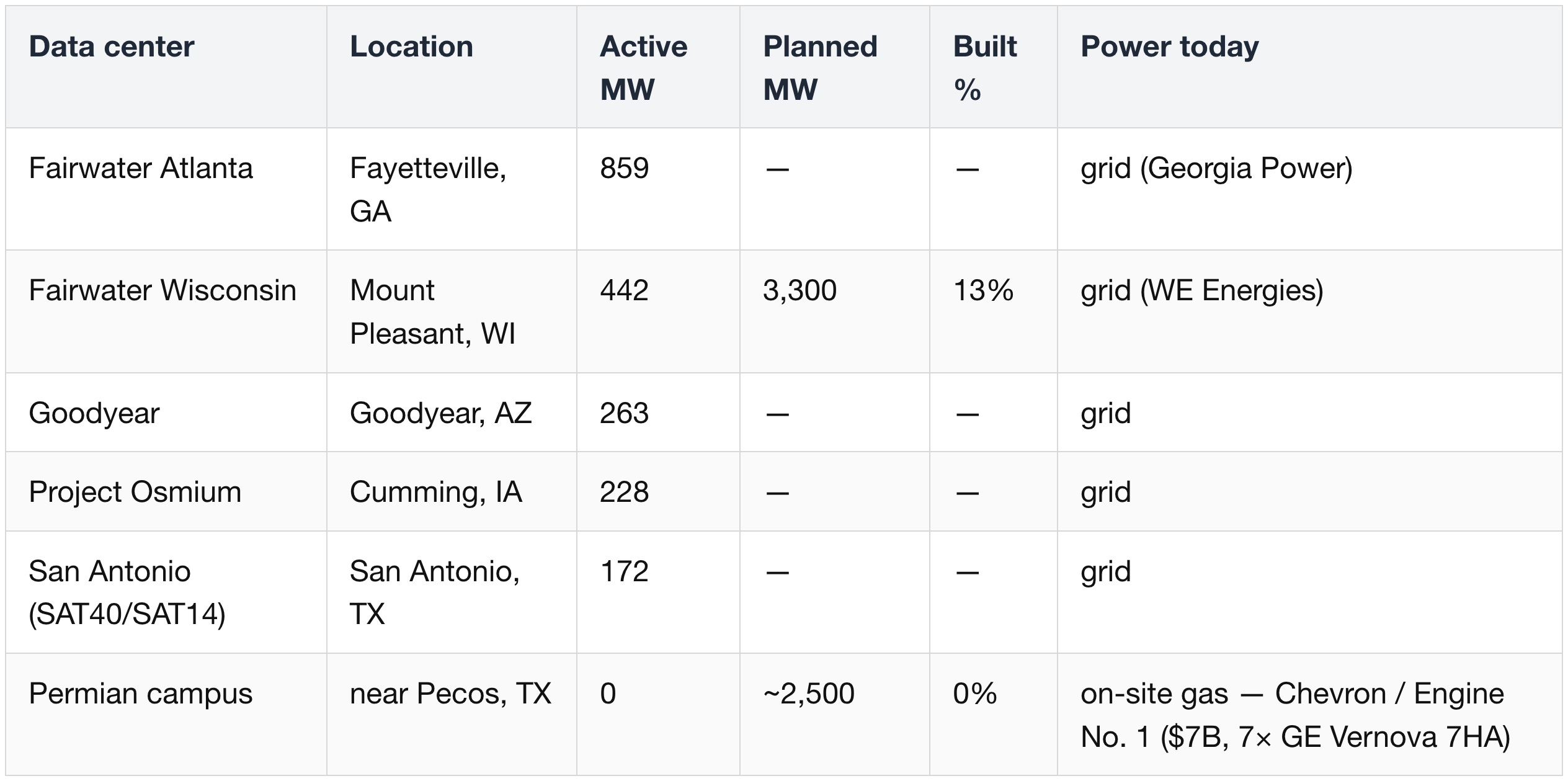

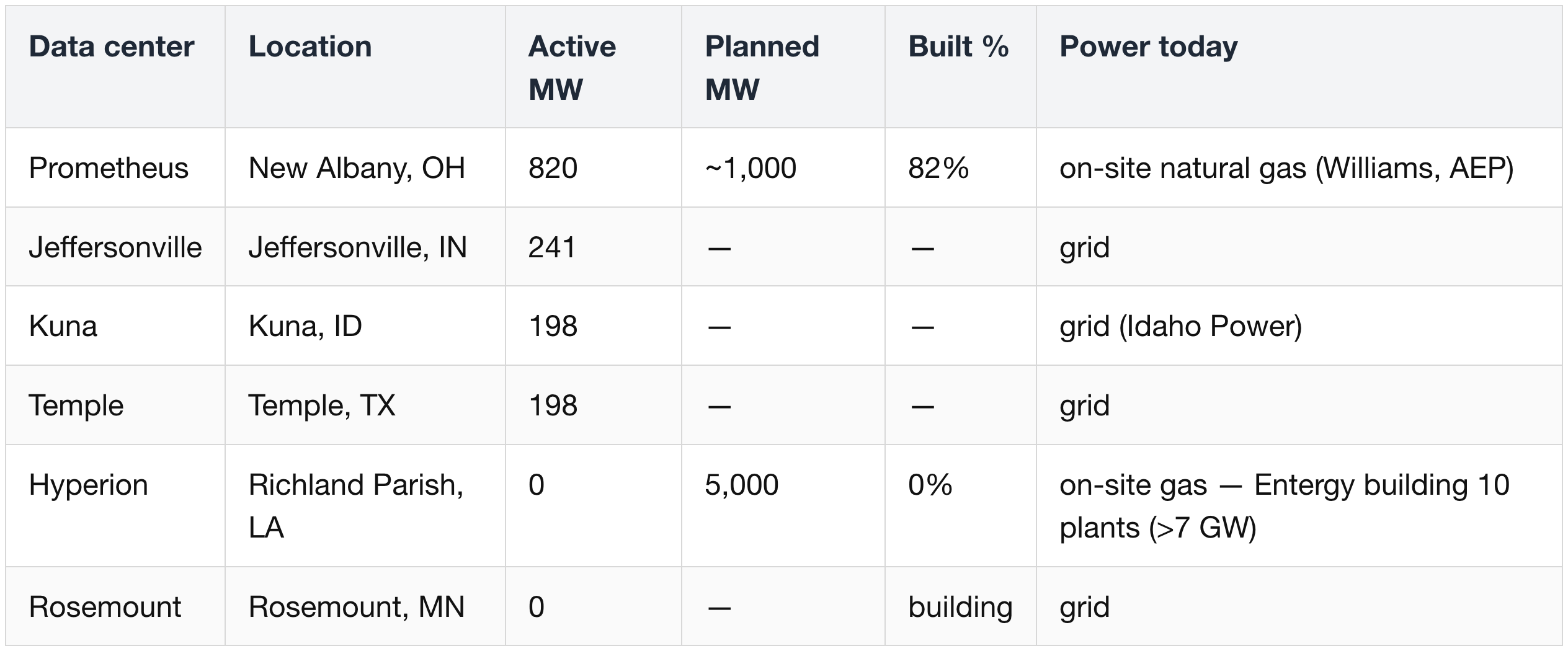

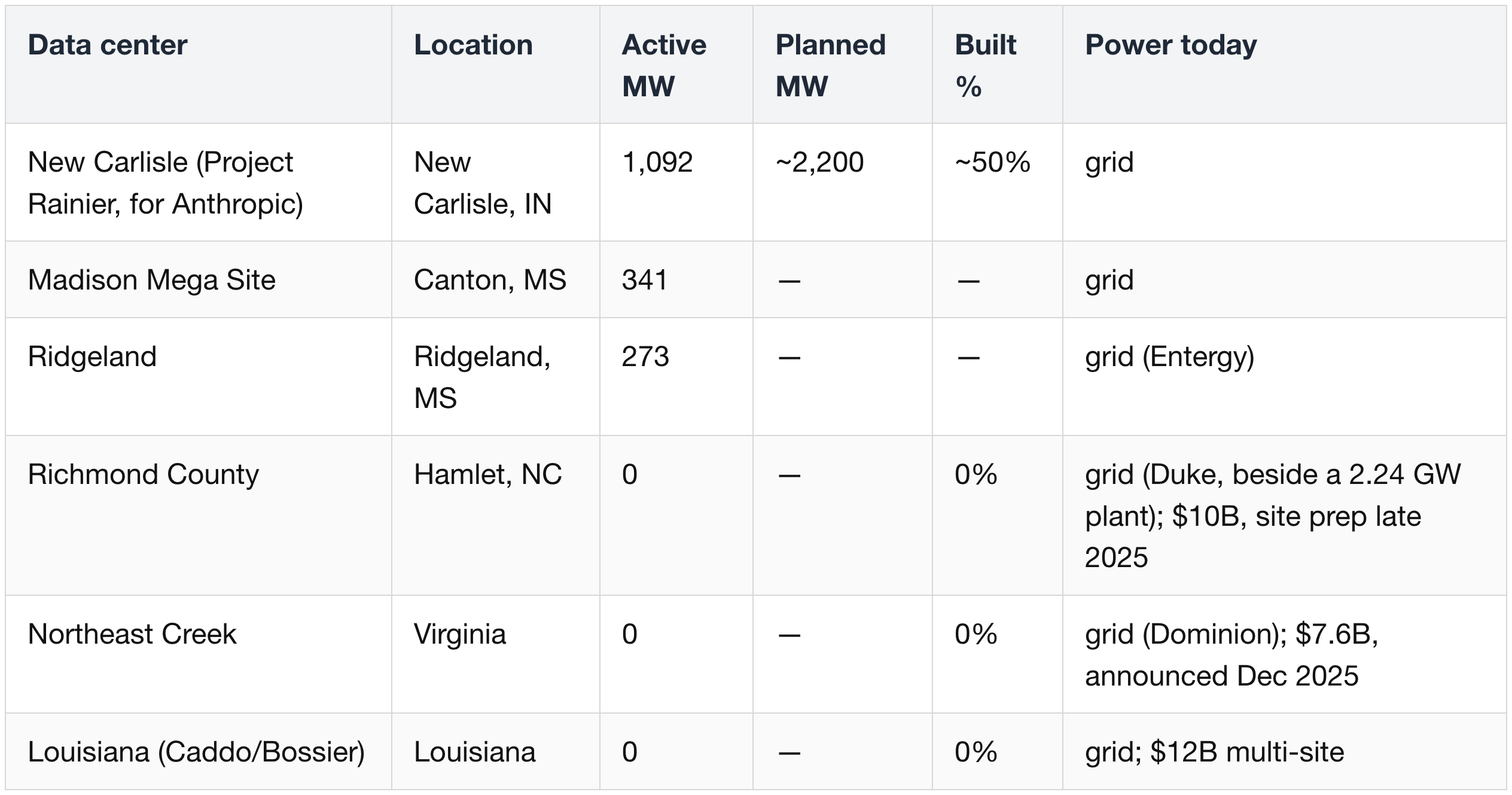

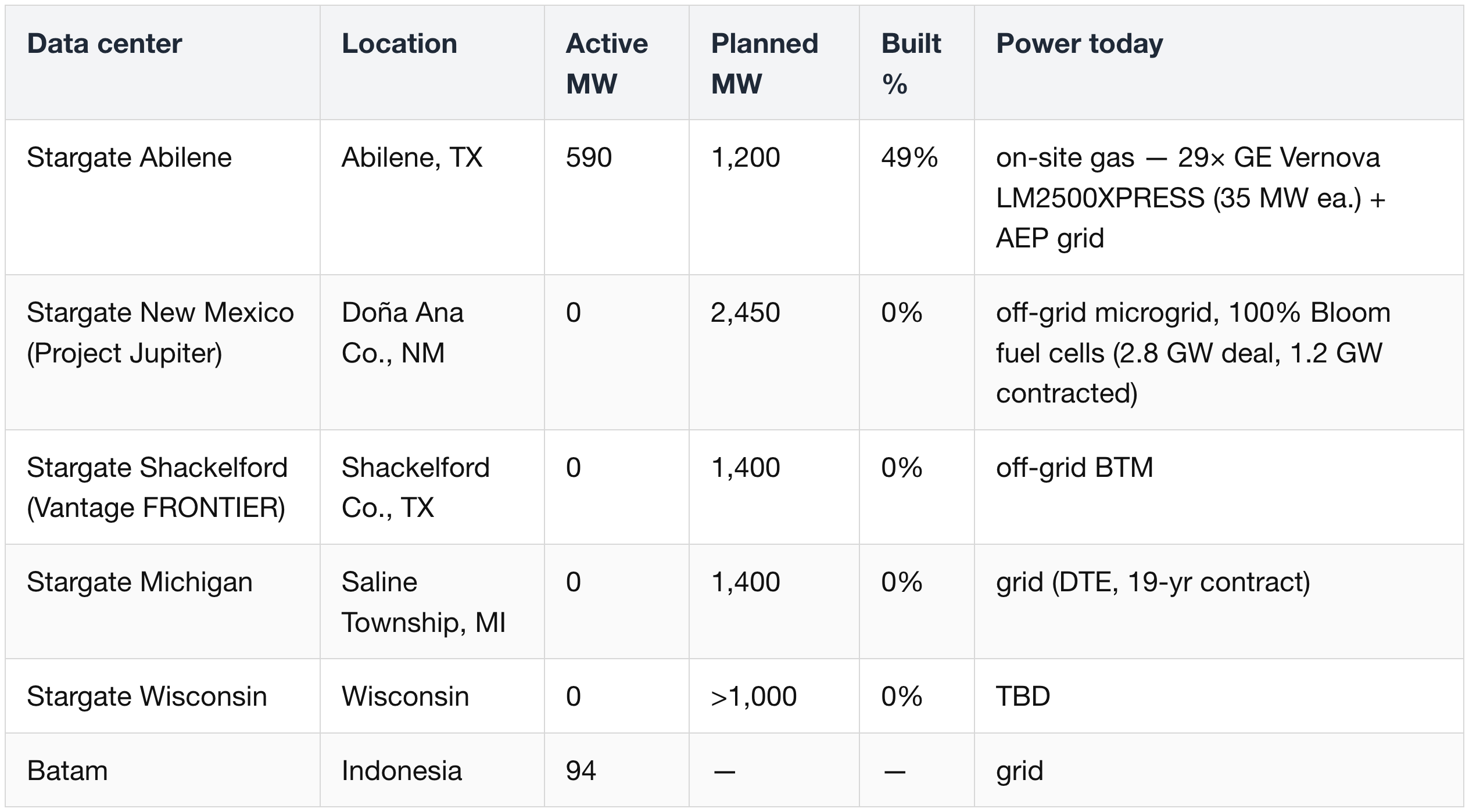

Oracle (NYSE: ORCL)

- Oracle is the anchor tenant of the Stargate program and has secured more than 10 GW of power coming online over the next three years.

- Its sites use a mix of off-grid gas, fuel cells, and grid — and are physically built by Crusoe and operated for OpenAI.

The pattern across the tables:

- Primary power is still mostly grid. Almost every active megawatt above is grid-fed; on-site generation is the exception, not yet the domain rule.

- On-site gas turbines are the main BTM lever, and increasingly run as primary power for the new off-grid / islanded campuses (Crusoe's Stargate Abilene, Meta's Hyperion, Microsoft's Permian site) — not just as backup.

- Fuel cells are the newest and still limited. Oracle's Project Jupiter is the standout, planning Bloom SOFC as a campus's primary 100% source.

- Nuclear / SMR PPAs backfill the permanent clean baseload later — mostly contracted for the future, not powering live load today.

- Among the big hyperscalers, only Oracle actually runs Bloom fuel cells (Project Jupiter) — the lone commercial hyperscaler deployment.

- Microsoft ran a 250 kW Dublin pilot only;

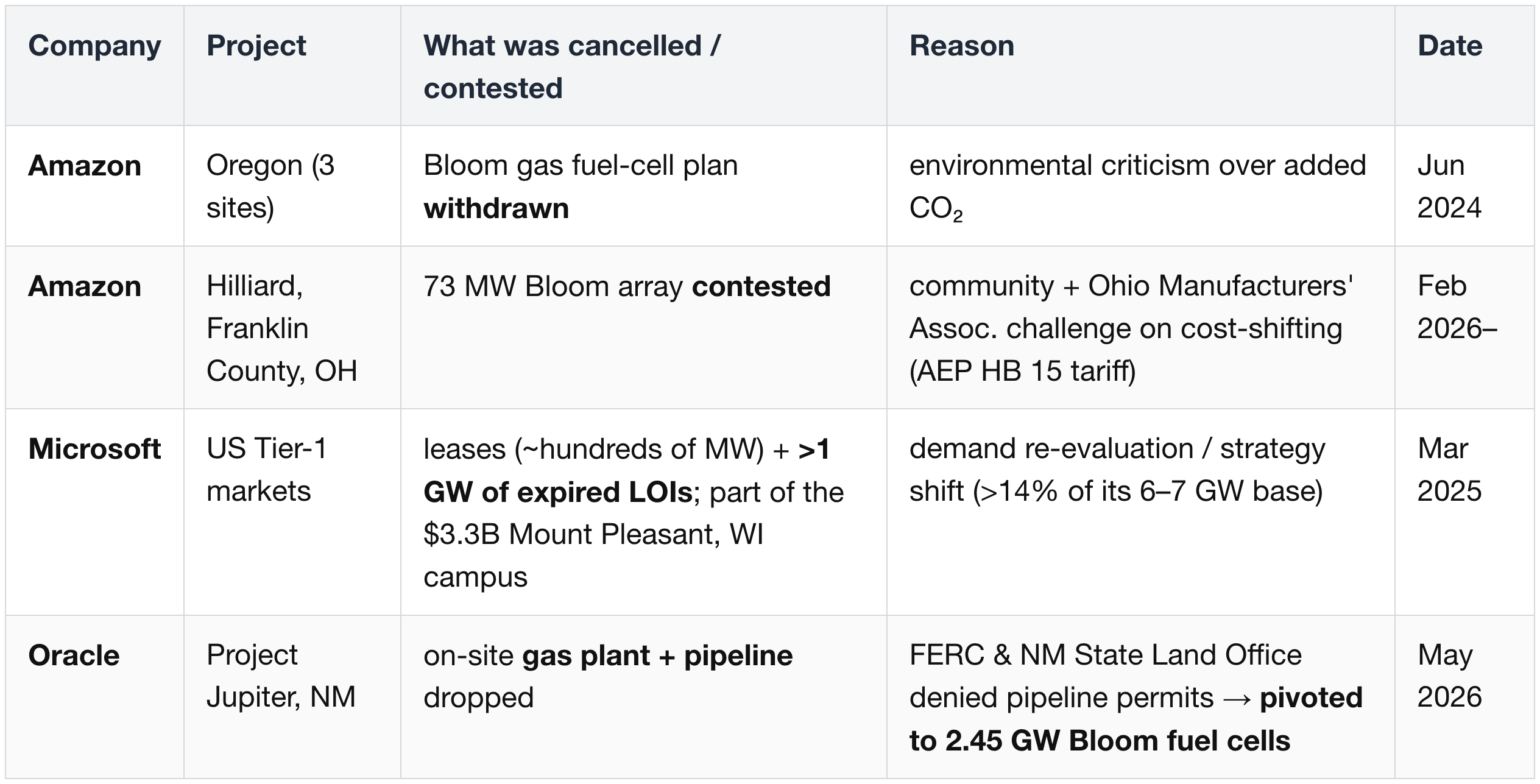

- Amazon withdrew its 2024 Oregon Bloom plan and has a contested 73 MW Bloom project at Hilliard (Franklin County), Ohio;

- Google and Meta have none yet.

Cancelled & contested BTM / fuel-cell projects (2024–26):

Microsoft's tell on how binding power has become: "something as simple as a power cord could be the difference about whether you could monetize something" (Microsoft — Evercore Global TMT Conference, 2026).

2.2 Neoclouds — lean hardest into BTM (gas + fuel cells) because rented-GPU revenue is existential

Without utility relationships or balance-sheet patience, neoclouds energize sites the fastest way available — leased shells, on-site gas, and fuel cells.

CoreWeave (NASDAQ: CRWV)

- CoreWeave runs about 1 GW active across 49 sites (Q1 '26), almost all leased / colocation, spread over ~40 development partners with no single one over ~17–20% — built that way for speed.

- It is scaling to 1.7 GW active by end-2026 against 3.5 GW contracted (mostly online by end-2027) and an 8 GW target by 2030.

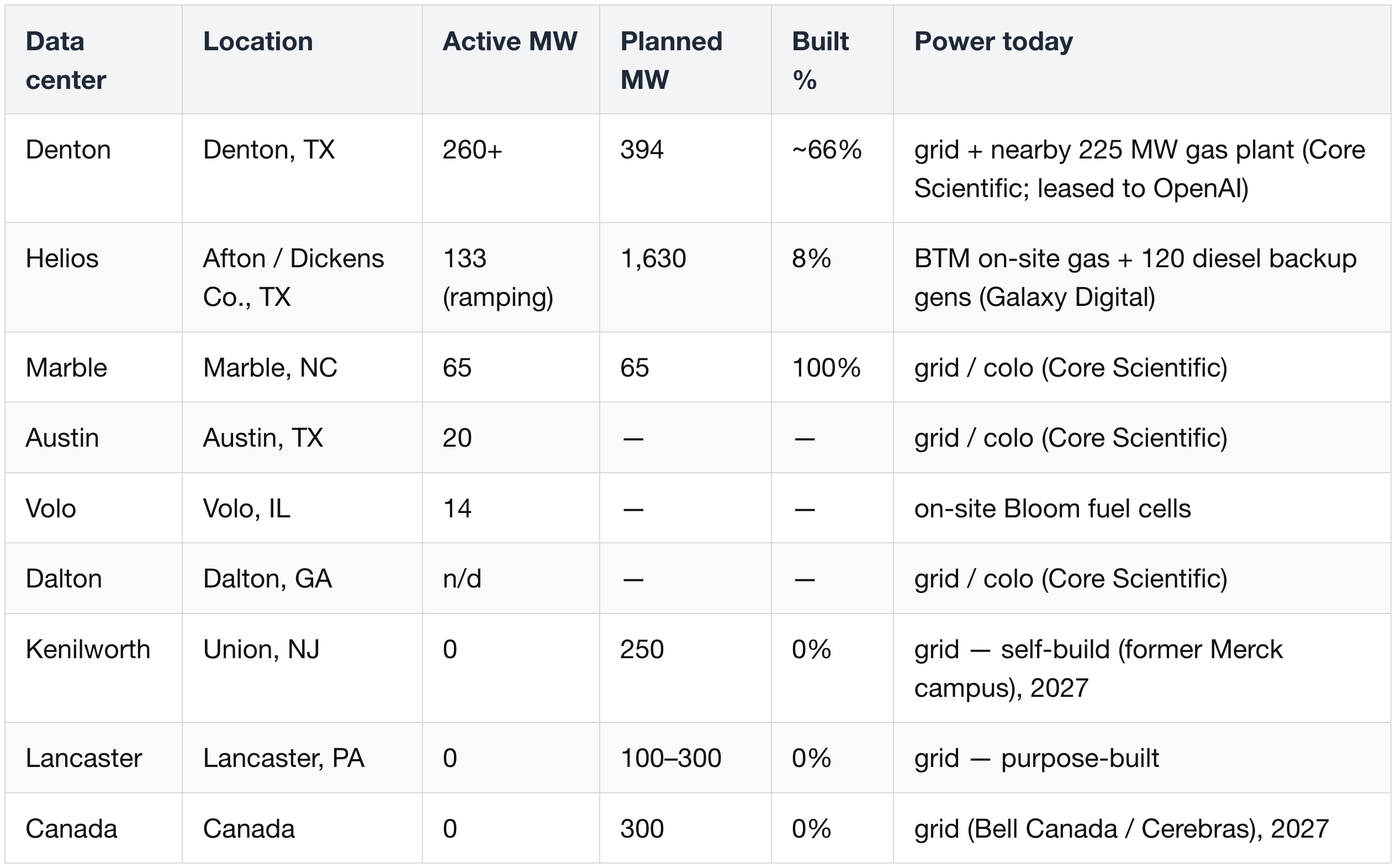

- Its largest host is Core Scientific (590 MW across five sites); it is now starting to self-build (Kenilworth, NJ) for control and margin, and uses Bloom's fuel cells (Volo) to energize sites in ~90 days and skip the grid queue.

~1 GW total active across 49 sites; CoreWeave discloses only a handful at site level, so the smaller colo sites aren't shown.

Nebius (NASDAQ: NBIS)

- Nebius owns more than 75% of its campuses outright, which improves its cost of ownership and its access to asset-backed financing.

- Its live capacity is small but real — ~170 MW active at end-2025 (flagship Mäntsälä in Finland plus colocation in Paris, Iceland, Kansas City, and Israel) — on track to 800 MW–1 GW connected by end-2026, against >3.5 GW contracted (toward 4 GW, and a 5 GW target by 2030). The gap reflects an 18–24-month build-and-energize cycle.

- It signed a 10-year, $2.6B deal with Bloom for 328 MW of behind-the-meter fuel cells at its US sites, to skip utility interconnection queues.

Nebius reports ~170 MW total active at end-2025 but breaks out only Mäntsälä (75 MW) at the site level, so the live colo sites show n/d.

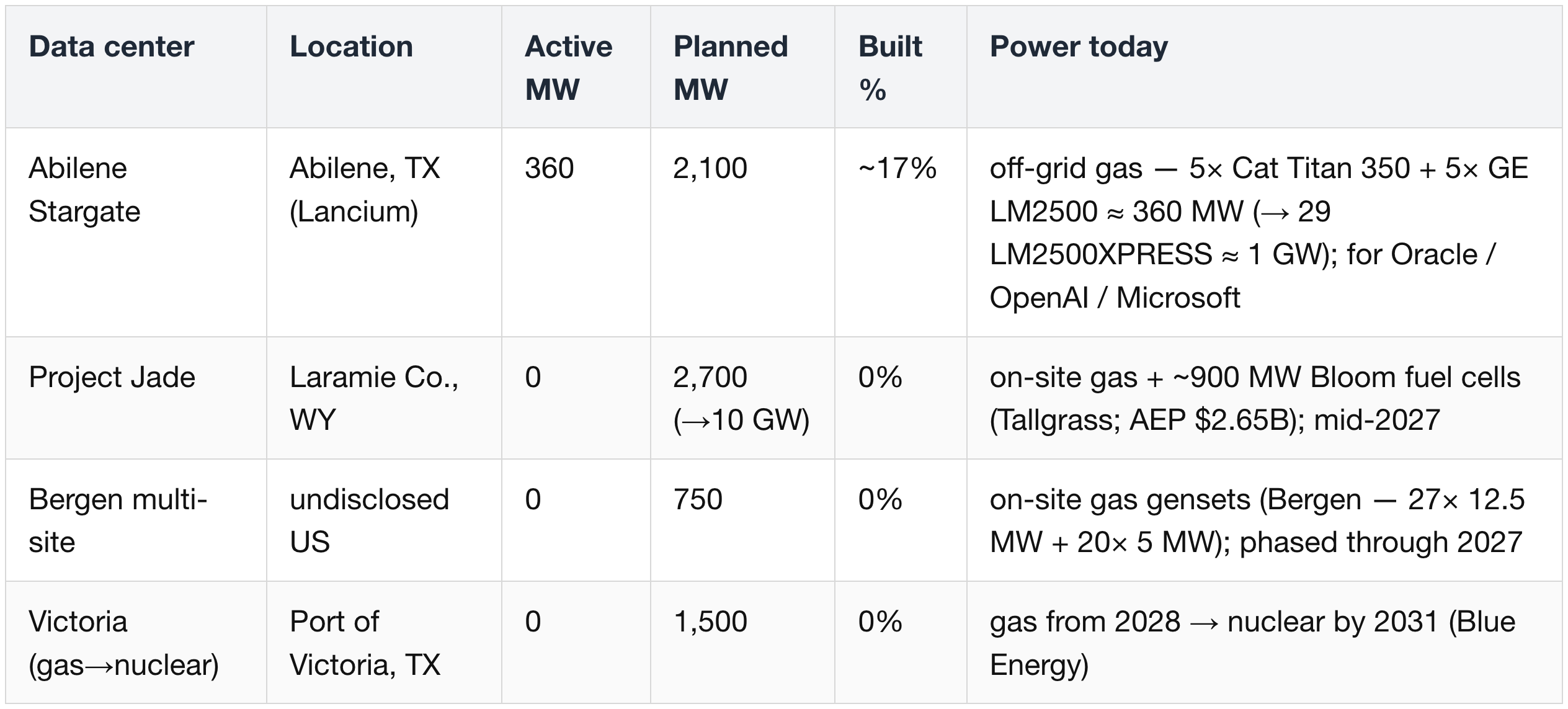

Crusoe (private)

- Crusoe is not a cloud operator but an off-grid, gas-first campus developer — it builds the power and the shells that others (Oracle, OpenAI, Microsoft, Google) run their GPUs in.

- It has ~360 MW operating today (Abilene Phase 1) targeting 1 GW operational by 2027. It sold its flared-gas / Bitcoin division to NYDIG (Mar 2025) and the Goodnight campus to Google.

- Because it develops for others, its compute capacity also shows up in the dataset under Oracle or Google rather than under its own name.

Abilene's 360 MW is the on-site gas generation Crusoe installed (Phase 1); the same campus appears as ~590 MW from the compute side in the Oracle table. Goodnight (sold to Google) and the former flared-gas division (sold to NYDIG, Mar 2025) are no longer Crusoe's.

The binding constraint for neoclouds is "powered shell," not electrons — "there aren't enough electricians, plumbers" (Nitin Kumar, CFO, CoreWeave — Jefferies conference, 2026). They do not expect supply–demand balance "before the end of the decade."

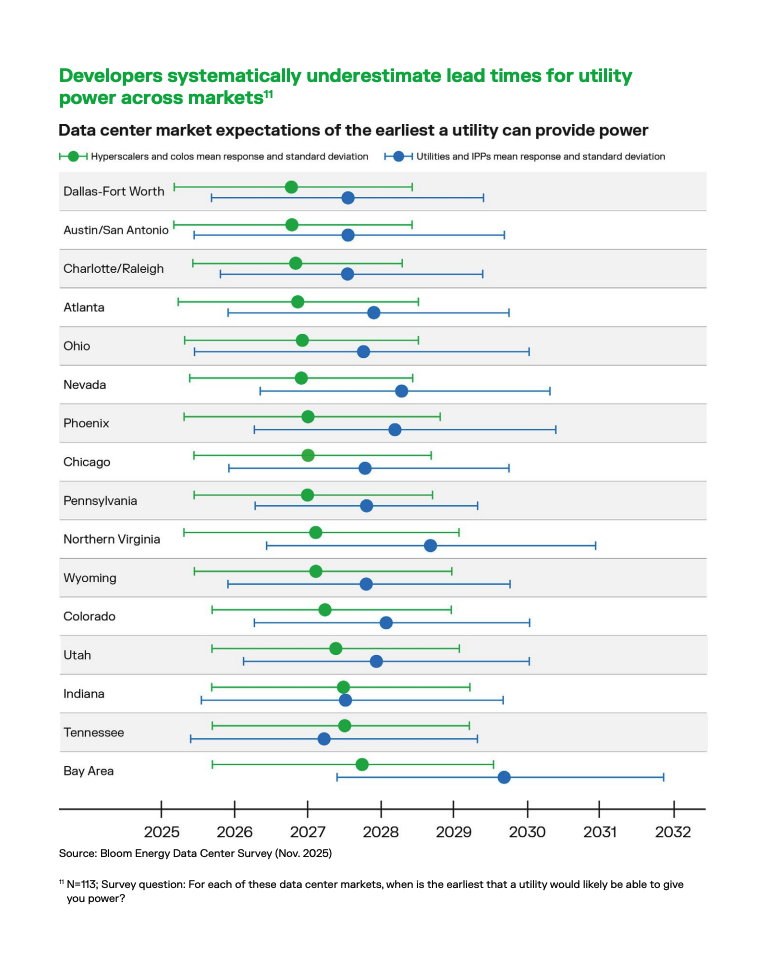

2.3 The consensus variable: time-to-power

Developers consistently expect utility power years before utilities say they can deliver it — the gap that pushes them to self-generate (Bloom Energy internal survey):

- "Time to power has gone from a procurement consideration to an existential necessity," with delays equal to "hundreds of millions in foregone AI revenue" (Bloom Energy management — Q1 '26 earnings call, Apr 2026).

- The binding cost is GPU idle time / delayed revenue, not the electricity price — which is why operators willingly pay a per-MWh premium to self-generate.

- BTM gas is being institutionalized as a financeable asset class: Atlas Energy signed a 1.4 GW Caterpillar framework and grew its pipeline from 4 → 8–10 GW; a natural-gas "renaissance" is underway after a decade of limited development.

3. Why BTM — and Why the Transition from Gas Turbines to Fuel Cells

3.1 Why BTM at all → speed

Grid interconnect runs 3–7 years; BTM gas ~18 months; fuel cells ~90 days. When a year's delay loses a hyperscale contract or misses an AI model generation, owning the timeline is worth a capital premium.

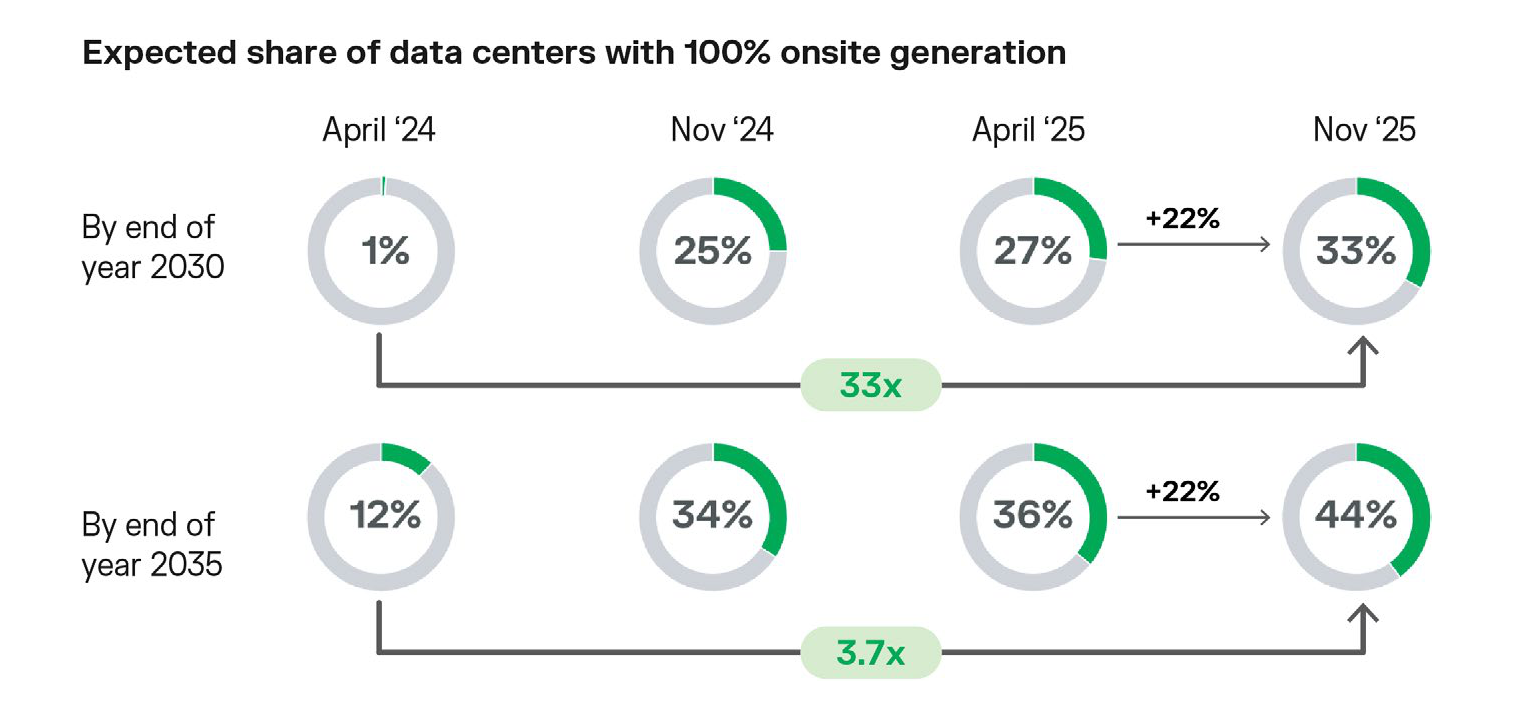

Developers are voting with their plans: the share of datacenters expecting 100% on-site generation (for end-2030) has gone from ~1% to ~33% in 18 months — a 33× jump — and ~12% → ~44% for end-2035 (Bloom Energy internal survey).

3.2 Why gas turbines stall → the supply bottleneck

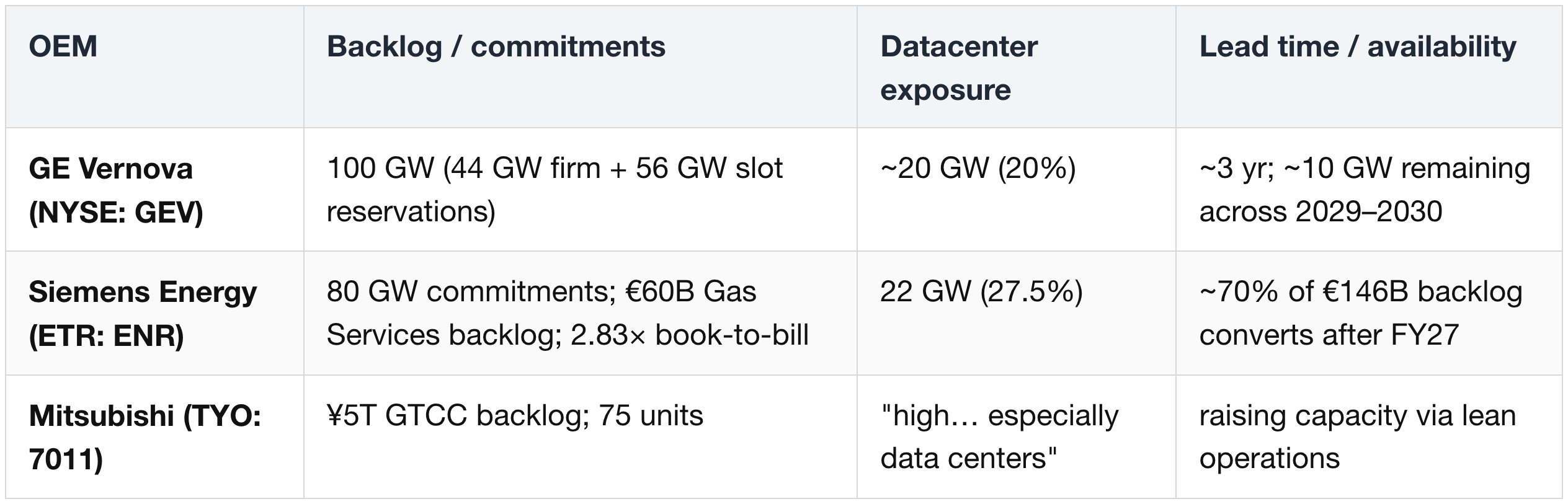

The deregulation-era overbuild (1990s–2000s) collapsed into stranded capacity in 2001, then again in 2018. Burned twice, the OEMs refuse to expand factories despite record demand — they harvest pricing power on a sold-out book instead:

- Pricing:

- GE Vernova's H1-2026 orders priced +10–20% $/kW vs Q4 '25;

- CCGT trending to ~$3,000/kW (+20% from $2,500).

- Siemens Gas Services margin expanded 14.6% → 16.6%.

- Capacity discipline (the key evidence):

- rather than new factories, OEMs squeeze productivity — GE Vernova added 280 machines + 1,800 workers (2025–26)

- and signaled no new factory decision "in the next 18 months" (Scott Strazik, CEO, GE Vernova — Q1 '26 earnings call).

- "Sold out through 2030" is the company's own projection for end-2026, not yet literal — currently sold out into 2028–29 with ~10 GW of 2029–30 slots left.

3.3 Why the ladder ends at fuel cells

When heavy-frame turbines sell out, buyers drop to the next rung — reciprocating engines — but that rung has filled up too, which is what finally pushes them onto fuel cells:

Reciprocating engines are no longer the fast escape hatch they were.

- Caterpillar's backlog has reached $62.7B with power-generation sales +48% YoY (Q1 '26);

- it is lifting large-engine capacity from 2× to 3× 2024 levels (an extra ~15 GW/yr) — but that investment only lands in 2027–29,

- so demand has already outrun supply here too. (Six of its deals are ≥1 GW each, including ProPower's 2.1 GW.)

Cummins tells the same story.

- It is adding 9 GW of high-horsepower capacity (toward ~55 GW by 2030)

- and sees datacenter revenue roughly tripling from $3.5B (2025) toward ~$9B (2030),

- with 6–8 quarters of orders already booked — i.e., the "cheaper, dirtier sibling" is itself backordered into 2027–28.

So the search for fast power doesn't stop at recips.

- Fuel cells become the last fast option standing: ~90-day deployment (55 days at Oracle), no turbine-slot queue, and a far lighter air-permitting path — near-zero NOx/SOx clears the gate that stalls turbines, even though the cells still emit CO₂.

- The CapEx premium is simply the price of time and permission — the two genuinely scarce goods.

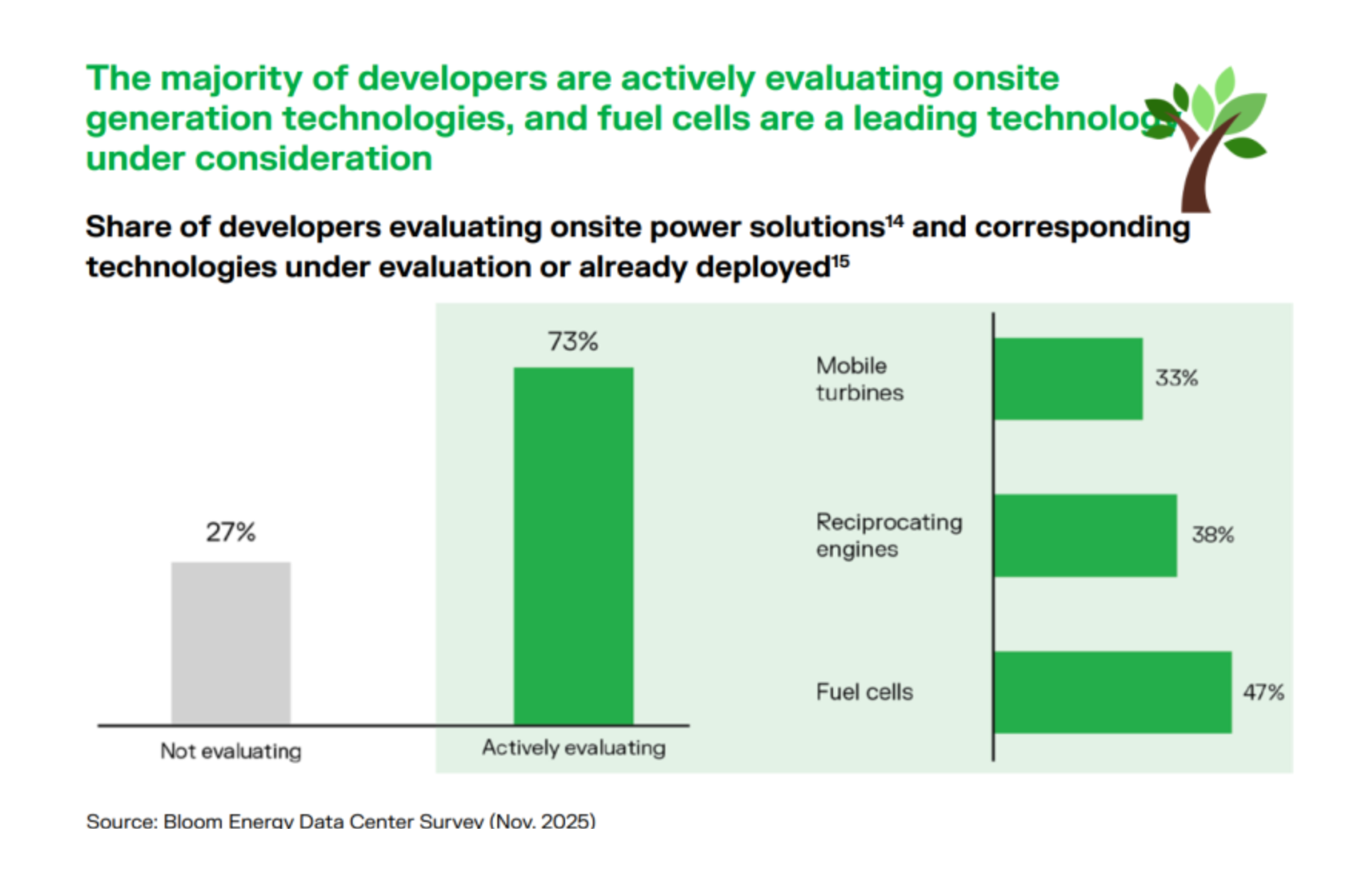

Developer surveys bear this out: Bloom's Nov 2025 datacenter survey found 73% of developers actively evaluating on-site generation, with fuel cells the single most-preferred option (47%) — ahead of reciprocating engines (38%) and mobile turbines (33%) (Bloom Energy internal survey).