US Treasury Yield Path Scenarios and Liquidity Positioning (2024)

US equities closed the week with high volatility. The VIX rose ~30% over a month, and the US 10Y Treasury yield rose ~16% over a month to 4.39%.

Behind the steep long-end rise despite the Fed's cut sit Sticky Inflation concern and US-election uncertainty. This note covers the path of US long-end yields. On a 10Y basis, US long rates sit in the elevated 4%+ zone.

1. Why a Rising Treasury Yield Is Feared

(1) Rising bank unrealized losses

Banks convert balance-sheet assets into Treasuries — low risk, steady cash flow, high liquidity. A yield rise is a price fall; if a sharp rise drops the market price below the purchase price, unrealized losses arise. The higher the yield, the larger the unrealized losses. In 2023, Silicon Valley Bank, Signature Bank, and First Republic Bank failed for this reason.

(2) The S&P 500's relatively lower earnings yield

As of Nov 1, 2024, the S&P 500 PER is 29.2. Earnings yield (the inverse of PER) is used to compare investment attractiveness against other asset yields.

- Higher earnings yield → higher profitability, possibly undervalued.

- Lower → lower profitability or overvalued.

The S&P 500's earnings yield computes to 3.4%. By contrast the US 10Y is 4.39% and the Moody's Seasoned BAA Corporate Bond Yield is 5.63%. Equities' relative attractiveness is lower than Treasuries / corporates — the broad market may be relatively overvalued — and rational investors are likelier to choose bonds over taking equity risk.

To the point: this note covers the Treasury's forward funding plan, the change in long-end market supply from the Fed's potential Operation Twist (OT), and the path of long-end yields.

2. The Treasury's Forward Funding Plan

As stressed in (3) Taking the Liquidity Temperature: Scenarios, Yellen issued bills well beyond the TBAC-recommended level to expand system liquidity and prop equities ahead of the election. To fund 2025, the weight must therefore shift to coupon issuance — the first signal that a lot of long-end supply will hit the market.

3. The Fed's Operation Twist (OT)

The Fed is running QT to shrink the SOMA account that ballooned under pandemic QE. It targets mainly long-dated paper and MBS, redeeming at maturity without reinvestment to drain liquidity. Naturally the long-dated share of SOMA falls and the bill share rises, shortening the maturity profile — consistent with the Committee's portfolio-restructuring goal.

The Fed's near-term aim is a soft landing via QT-driven absorption and safe cuts, but this is not an environment for consecutive cuts. Core PCE still runs above target, and the October employment data added labor-market uncertainty. The tool to support the economy when consecutive cuts are hard is precisely Operation Twist (OT) — easing via securities-mix restructuring, i.e. raising the bill share.

Why raise the SOMA bill share? Four reasons:

- To raise funds to run OT — OT (formally the Maturity Extension Program) induces a long-rate decline without balance-sheet expansion, by changing only the asset mix (lower long rates → lower borrowing costs → more consumption/investment). When needed, the Fed sells held bills and buys long bonds with the proceeds.

- To maintain an Income-Neutral Balance Sheet (INBS) — a higher bill share makes interest cost and income both track the policy rate, stabilizing net interest income.

- Monetary-policy efficiency.

- Minimizing market distortion.

Critically: if recession-with-inflation makes further cuts hard, the Fed must lower long rates to support the economy without raising system liquidity — by changing only the SOMA mix, selling bills for cash and buying long bonds. Since the long-dated share of SOMA is currently very high, space must be created in advance.

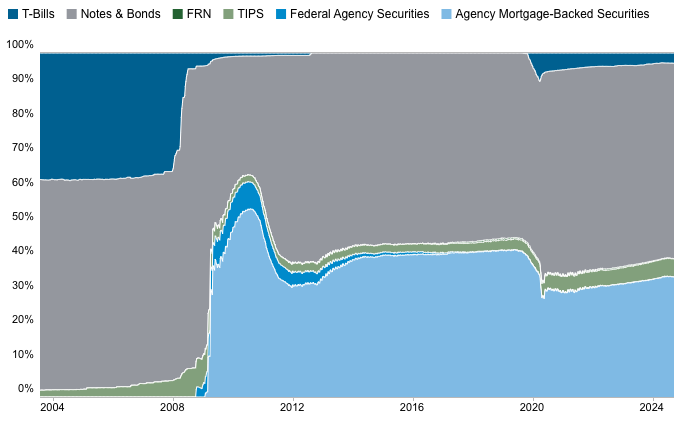

Change in the Fed SOMA portfolio maturity structure

Before the 2009 GFC the Fed held ~1/3 of SOMA in bills; now it is under 5% of Treasury holdings. The signal that bill / long-end supply may hit the market near-term is contributing to upward long-rate pressure (lower long-bond prices).

4. Upward Pressure on Long-End Supply

The Treasury's long-end issuance for fiscal funding and the Fed's bill-share build to prep OT both raise long-end supply (at least over the short-to-medium term). If long-end supply keeps hitting the market and long rates rise, a scenario assuming long-end yields spike to 5–6%:

- Bonds' relative attractiveness vs risk assets rises sharply, so bonds rapidly absorb liquidity from risk assets.

- Dollar liquidity in global safe assets rotates into the US.

The crux is each country's relative sovereign-bond attractiveness. Whether Korea's 10Y at 3.083% is more attractive than a 5–6% US 10Y is doubtful. The most at-risk are Korea or major Emerging Markets. Korea in particular — high foreign-capital dependence, weak domestic demand — faces a larger hit via capital outflow → KRW/USD depreciation → export-economy instability.

5. Conclusion

Uncertainty is high. Whoever wins the election (Trump or Harris), pledges center on higher fiscal spending, so the Treasury's funding problem is unlikely to resolve easily (debt must be issued regardless). A temporary long-end rise during the Fed's OF preparation cannot be ruled out either. When and how each factor feeds the bond market, and how much is already priced, is hard to judge.

Still, at least over the short-to-medium term, keep in mind the possibility of rising long-end yields and the resulting absorption of global liquidity and risk-asset liquidity into the US bond market. Rather than timing the start precisely, prepare a response around the scenarios.